Russia-China Economic Relations

Moscow’s Road to Economic Dependence

SWP Research Paper 2024/RP 06, 24.05.2024, 39 Seitendoi:10.18449/2024RP06

ForschungsgebieteDr Janis Kluge is Deputy Head of the Eastern Europe and Eurasia Research Division at SWP.

-

Russia’s full-scale invasion of Ukraine has fundamentally changed the terms of Russia-China economic relations. Economic cooperation with China has become vital for the Russian economy.

-

Trade turnover between Russia and China has increased significantly since February 2022. However, Chinese companies remain hesitant about investing in Russia.

-

Energy cooperation remains the backbone of Sino-Russian cooperation, but the expansion of Russian exports is hindered by infrastructure limitations.

-

Russian arms exports have declined in recent years. Meanwhile, China exports large quantities of dual-use goods to Russia, which are urgently needed by the Russian military industry.

-

Sino-Russian cooperation in the digital economy has been hit hard by Western sanctions. China’s digital giants cancelled several projects in Russia due to fears of secondary U.S. sanctions.

-

Russia’s trade with China is mainly conducted in Chinese yuan. However, Russia continues to rely on the U.S. dollar for trade with the rest of the world.

Table of contents

2 Russia-China Economic Relations in the “Putin Era”

2.1 China’s gravitational pull grows

2.2 China becomes Russia’s lifeline

3.2 Chinese investors not interested

4.1 Energy remains the backbone

4.2 Russian advantage in arms technology is shrinking

4.3 Sino-Russian IT cooperation in trouble

4.4 Chinese yuan – for lack of a better option

5 Russian Elites and Public Opinion

5.1 Beijing bets on Putin’s entourage

5.2 Potemkin cooperation in the regions

5.3 Sinophobia is not an obstacle

Issues and Conclusions

Russia’s post-soviet transition from a planned to a market economy was accompanied by deep integration with Western economies. Due to its geographic proximity to Europe, existing infrastructure, and the fact that most Russians live in the European part of the country, economic links to the EU flourished. The West was an ideal economic partner for Russia, offering both advanced technologies, capital, and ample demand for Russian natural resources.

Only after China’s rapid growth in the 2000s did the People’s Republic become a viable economic alternative. At first, China mainly provided Russia with inexpensive consumer goods. However, as Chinese industries became more technologically advanced, it evolved into a complementary partner for many sectors of the Russian economy. The start of economic cooperation between China and Russia was initially slow due to Moscow’s deep-seated scepticism towards Beijing. However, the construction of a major oil pipeline in the late 2000s led to a rapid increase in trade turnover between the two countries. China’s insatiable demand for natural resources from Russia, as well as its increasingly sophisticated export offerings, resulted in a flourishing trade relationship in the 2010s.

Simultaneously, Russia underwent a significant shift in its foreign policy, as its relations with the West became more strained in the late 2000s. Following Russia’s annexation of Crimea and its covert war in Donbas, conflicts dominated its relationship with the West. While these conflicts were not the sole reason for the increasingly warm political ties between China and Russia, they did accelerate the deepening of the partnership. In early February 2022, shortly before Russian President Vladimir Putin ordered the full-scale invasion of Ukraine, a joint Russian-Chinese statement described the bilateral relationship as a ‘limitless friendship.’

Initially, the new political reality post-2014 did not result in a complete shift of Russia’s economic dependencies to the East – despite a first round of Western sanctions. While Putin and Xi publicly praised the successes of Sino-Russian cooperation at every one of their regular meetings, Russian companies continued to rely on Western technologies and focused on European markets. China’s economic significance for Russia was growing gradually; however, Russia was still much more dependent on Western economies in almost every aspect of its economic life.

All of that changed with Russia’s full-scale invasion of Ukraine, which marked a turning point in both Russia relations with the West and Russia’s relations with China. Although the West’s sanctions on Russia do not extend to all forms of economic cooperation, a fundamental “decoupling” of Russia’s economy from the West has begun. Against this background, cooperation with China has become vital for large parts of the Russian economy as well as the political regime in Moscow. The new significance of China goes much further than just an increase in trade, which is itself impressive.

China is the only major industrial nation that still trades with Russia largely without restrictions. The volume of exports to Russia is significant, as many of the sophisticated goods that Russia obtains from China, such as machinery, electronics, or vehicles, cannot be imported from anywhere else. Additionally, in certain aspects China’s yuan and financial infrastructure have replaced the Western financial system for Moscow. Beijing’s conduct towards Russia has also become a model for non-Western nations seeking to remain neutral in the conflict between the West and Russia.

The future trajectory of Russia-China relations will not only determine Russia’s economic prospects under sanctions but also have significant implications for the war in Ukraine and the future security order in Europe. Moscow has been able to mitigate some of the effects of Western sanctions with the help of China. Although the People’s Republic has not delivered heavy weaponry to Russia, its exports of dual-use goods, machinery, materials, and components facilitate the expansion of the Russian military industry. These exports to Russia do not only pose an immediate threat to Ukraine, but also boost Russia’s long-term military potential. In reaction to the ongoing delivery of sanctioned goods to the Russian military industry, the EU sanctioned Chinese companies over the war in Ukraine for the first time in June 2023. This shows that an overly close economic cooperation between Russia and China could also lead to increasing tensions between China and the West.

However, Russia cannot count on any favours from China. Beijing has remained cautious and often ambivalent in its stance towards Moscow post 2022. This is partly due to concerns about sanctions pressure from the U.S., but also the desire to maintain at least some constructive relations with the EU. Since the start of the full-scale invasion, no new large-scale Chinese-Russian cooperation projects have been announced. While Chinese businesses are taking advantage of openings in the Russian market left behind by Western companies, the Chinese leadership is trying to avoid the impression that it is overtly supporting Russia’s aggression.

Russia-China Economic Relations in the “Putin Era”

Although diplomatic relations between Russia and China have been continuously improving since the end of the Soviet Union, economic cooperation was initially neglected. Moscow and Beijing made far-reaching plans to foster economic cooperation in energy and other natural resources in the 1990s, but most of these ideas were shelved until the late 2000s. Both Russia and China were mainly focused on the West, to benefit from Western capital, technology, and markets.

The risks of overly depending on the West first became a serious issue for Russian policymakers after the Global Financial Crisis in 2008/2009. Capital flight and the declining demand for natural resources led to a deep recession in Russia. Moscow mainly blamed mistakes in American economic policies for the crisis, which led them to the conclusion that relying on the West too much could be economically risky. China, in contrast, seemed to be much less affected by the global recession, and its continuing economic boom impressed Moscow’s political elites.

However, Moscow did not immediately try to shift its dependence to the East. Instead, then-President Dmitry Medvedev attempted a political “reset” of U.S.-Russian relations during his 2008-2012 term. The signature project of his presidency was to be “Modernizatsiya,” a modernization campaign inspired at least in part by liberal economic ideas. Medvedev planned to build an innovation center in the Russian suburb of Skolkovo, which he wanted to become “Russia’s Silicon Valley” and for which Western companies were the most important partners. It was only with Putin’s return to the Kremlin in 2012 that the Russian leadership began to pursue the economic and political pivot towards China more seriously.

When Putin was campaigning to be elected president of Russia for a third term in 2012, he published an article on Russia’s economic future in which he proposed to catch “Chinese winds” in the sails of the Russian economy.1 These ambitions were not just about economic growth or progress. Putin’s economic policy was increasingly influenced by his anti-Western stance. Against the backdrop of the bombing of Libya by NATO in 2011 and Western sympathy for a protest movement in Moscow following the Duma elections that same year, his rhetoric toward the West became increasingly bitter and hostile.

China’s gravitational pull grows

When a coalition of Western countries imposed sanctions on Russia in reaction to Russia’s annexation of Crimea and its covert war in Donbas in 2014, the desire in the Kremlin to reorient Russia’s economy grew.2 Under the slogan “turn to the East” the sanction-caused problems of the Russian economy were reframed as an economic opportunity – at least in the official state propaganda. Both in domestic politics as well as on the international stage, Putin pointed at growing trade with China to characterize Western sanctions as pointless and ineffective.

There was a real increase in Russia-China trade in the 2010s, but it was driven less by sanctions or the flourishing friendship between Putin and Xi. The main cause of the boom was China’s economic expansion.3 While negotiations on several Sino-Russian megaprojects in energy and the arms trade were finalized in 2014, these talks had already been progressing for several years. Western sanctions created an impetus to show progress in Russia-China economic relations for the Kremlin, but these plans were not new.4

Russia’s full-scale invasion of Ukraine fundamentally changed the terms of Russia-China economic cooperation.

Russia’s economic policy post 2014 was often contradictory and driven by lobbying interests, which at times made it harder to deepen ties with China. Russia’s policy response to Western sanctions after 2014 was mainly focused on strengthening its own economic sovereignty. Moscow did not plan to replace Western economic dependency with a new dependency on China. Import substitution was the highest policy priority, because it satisfied both national security elites and influential lobby groups.5 Moscow still viewed its rising Eastern neighbour with some scepticism.

This became apparent in trade policy, an area where Russia and China did not make significant progress in the 2010s. Moscow resisted Beijing’s plans to deepen economic cooperation in the framework of the Shanghai Cooperation Organization. Beijing then began pursuing its own Silk Road project,6 while Russia set up the Moscow-dominated Eurasian Economic Union (EAEU) in 2015. Both Russia and China were only interested in economic integration when it did not limit their own sovereignty or control.

Moscow was worried that Chinese goods would undermine the competitiveness of Russian industries and was mainly looking for foreign direct investment (FDI) from China. Meanwhile, China was mainly interested in expanding its exports to Russia. These diverging interests meant that the scope for deeper economic integration was limited. While Putin and Xi announced the linking (Sopryazheniye) of their respective megaprojects EAEU and New Silk Road in 2015, this did not lead concretely to any further steps. In 2018, Putin signed a free-trade deal between China and the EAEU, but the agreement is “non-preferential”, meaning there is no actual reduction in trade barriers.7 As one of a few concrete changes, Russia and China did set up several new bilateral minister-level government commissions. In 2014, the Intergovernmental Russian-Chinese Commission on Investment Cooperation (CIC) was created.8 At the same time, another Commission for the Development of Russia’s Far East, Lake Baikal and Northeastern China was brought to life.9

The successes of Russia-China cooperation mainly happened in the field of Russia’s export of natural resources and its related economic sectors. As China’s hunger for commodities continued growing, Russian exports of coal, liquefied natural gas (LNG), metals, ores, but also agriculture products soared between 2014 and 2022. Mining and agriculture were also the sectors that saw most of the relatively few big Chinese investment projects in Russia. At the same time, the People’s Republic remained much less important for Russia than the West in almost all sectors of the economy. Russia’s economic reality was notably different from the prevailing mood in Russia’s foreign policy, which saw a deepening partnership with China and an increasingly hostile relationship with the West.

China becomes Russia’s lifeline

Russia’s full-scale invasion of Ukraine fundamentally changed the terms of Russia-China economic cooperation. Russia’s economic reality caught up to its political reality overnight. Harsh Western sanctions caused economic havoc in Russia, as supply chains with Western partners that were built over several decades collapsed. Russian businesses were urgently looking for a new source for components, materials and replacement parts, to keep their operations up and running. Most of them found new business partners in China – the only major industrial country that had not imposed sanctions against Russia.

China’s leadership criticized Western sanctions on Russia, but it was not immediately clear if Chinese companies would be willing to supply sanctioned goods to Russia. Some large Chinese companies such as Huawei began to strictly limit their exports to Russia, while Chinese banks tried to distance themselves from Russia out of fear of secondary sanctions.10 In trade relations, this initially cautious stance only lasted a few weeks, before Chinese exports to Russia surged again. In other areas of economic cooperation between Russia and China, sanctions have remained a severe obstacle.

Trade and Investment

Trade turnover between Russia and China reached a new record of $241 billion in 2023.11 Although the growth of China-Russia trade follows a multi-year trend, Western sanctions against Russia led to a significant boost post 2022. In contrast, Chinese investment in Russia appears to be declining, not growing. The flow of Chinese capital to Russia has always been small, but since the start of the full-scale invasion, not a single large investment project has been launched. The risks of a long-term commitment to the Russian market outweigh the possible economic opportunities.

Dynamic growth in trade

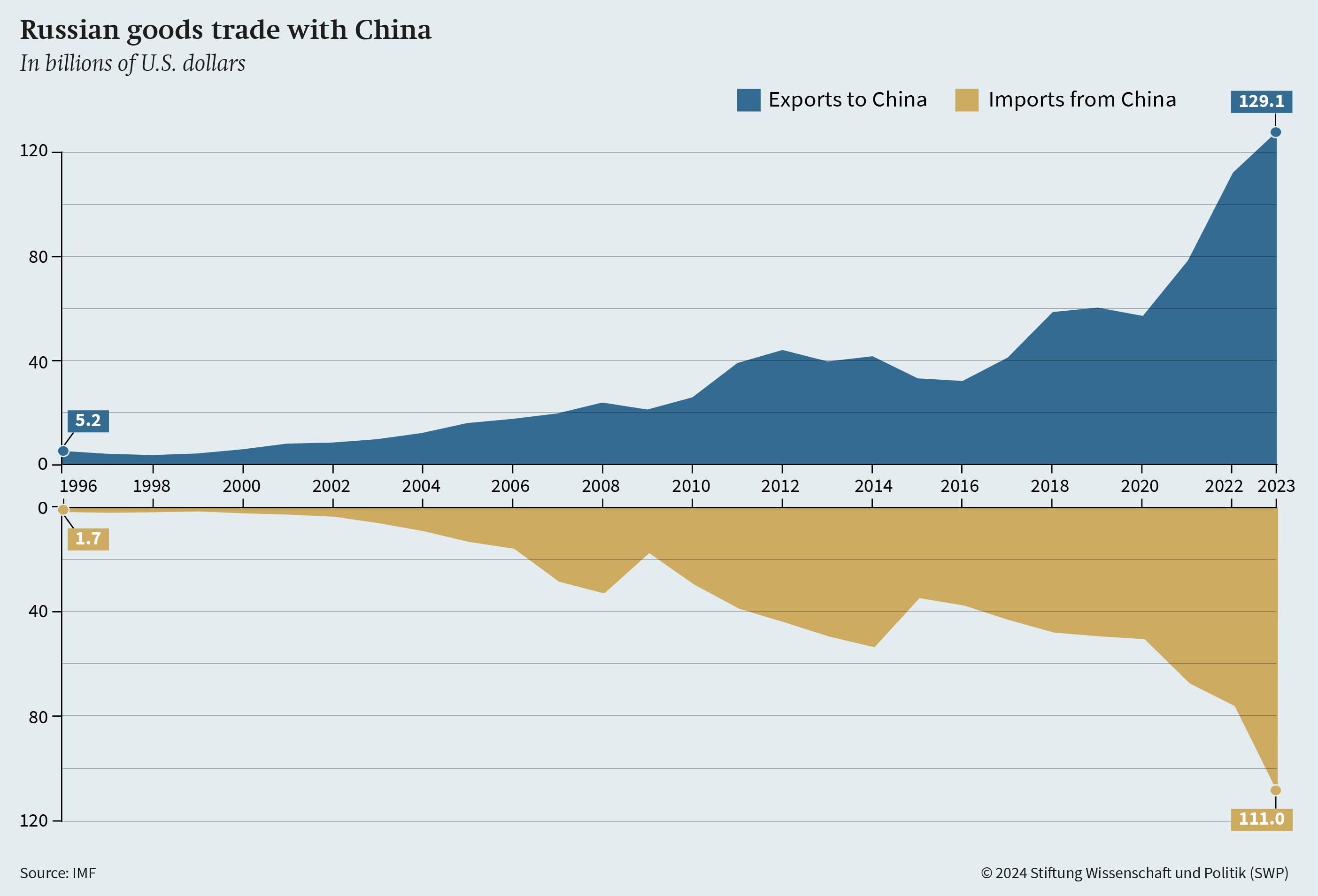

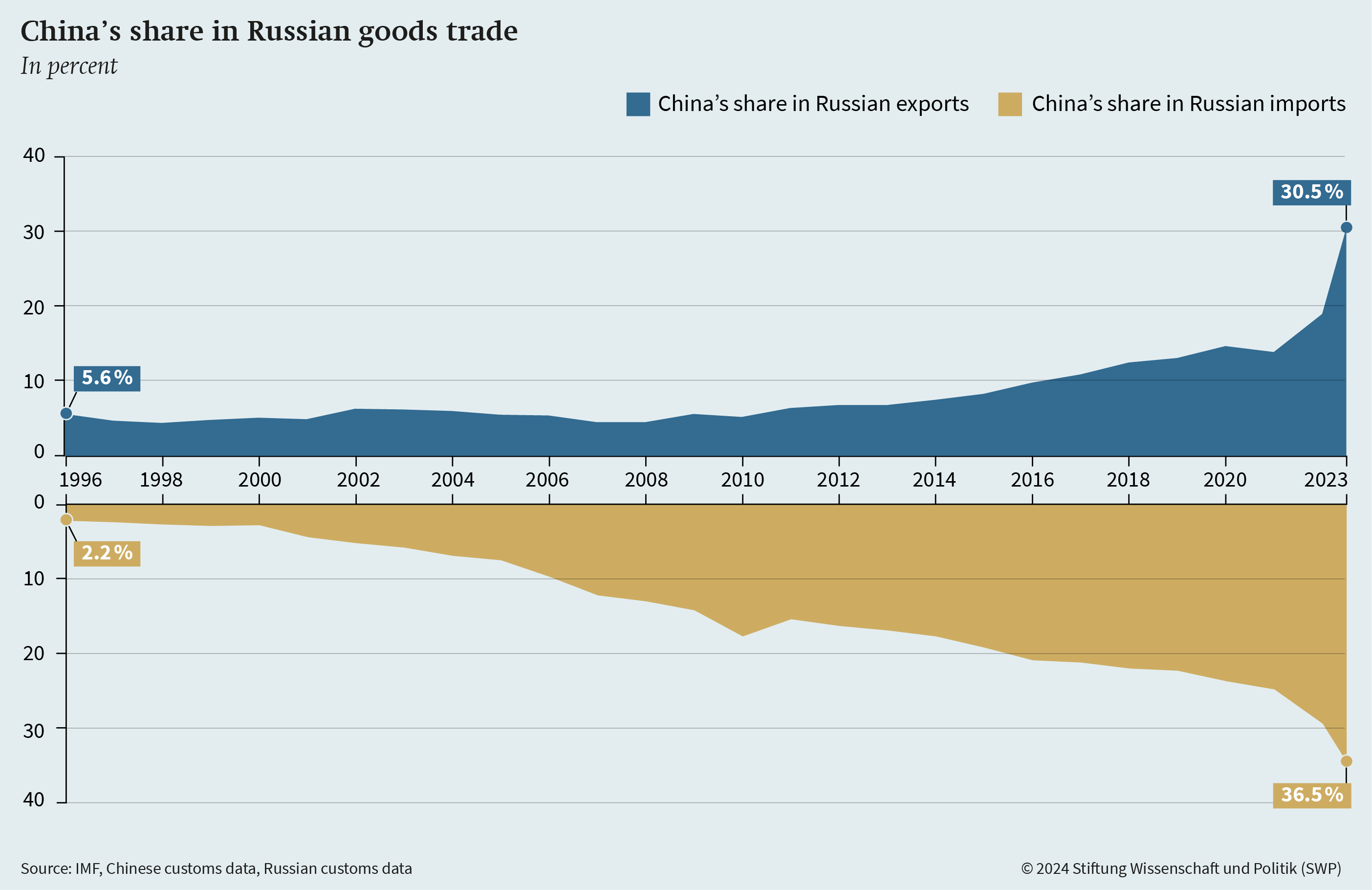

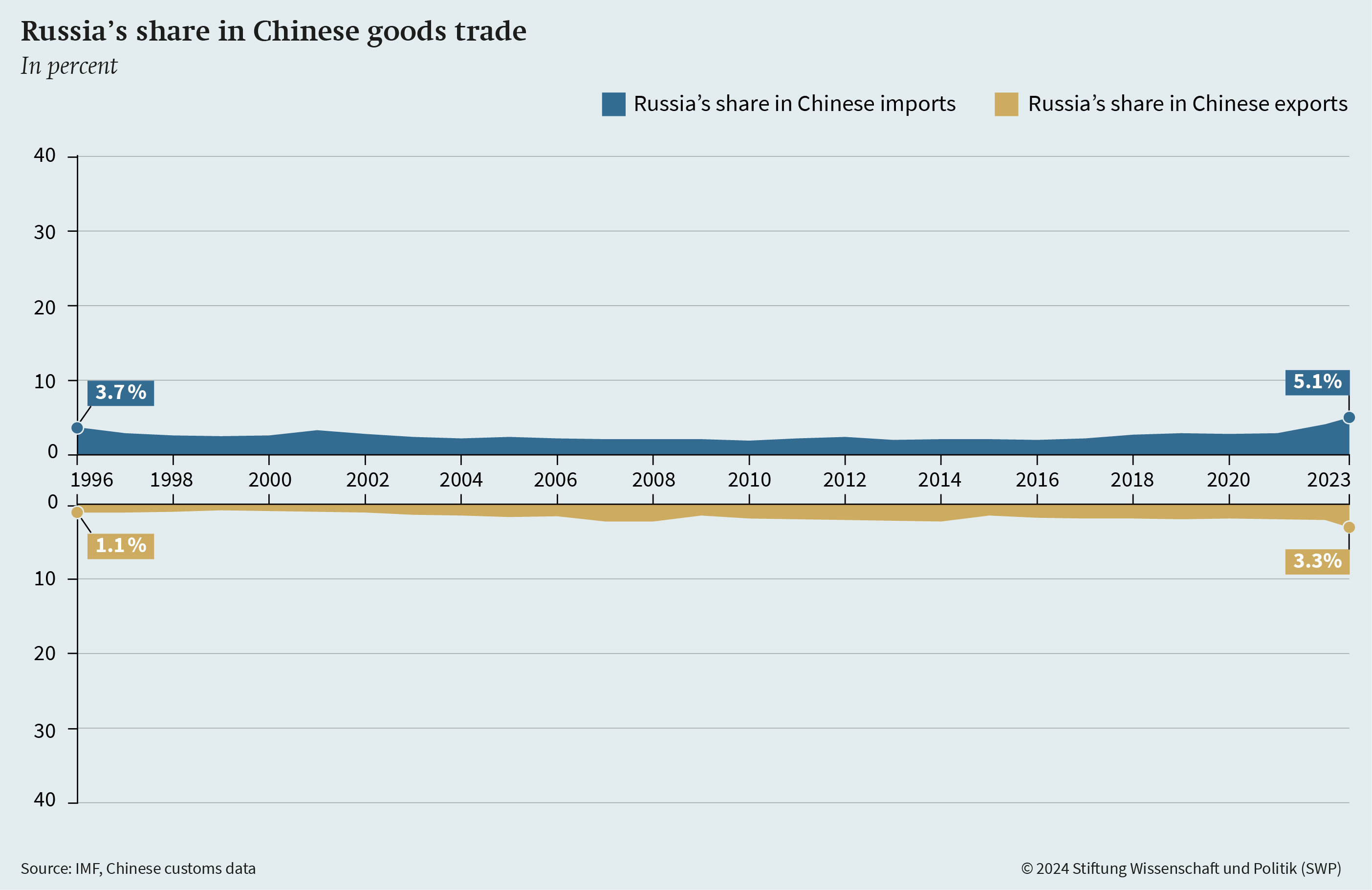

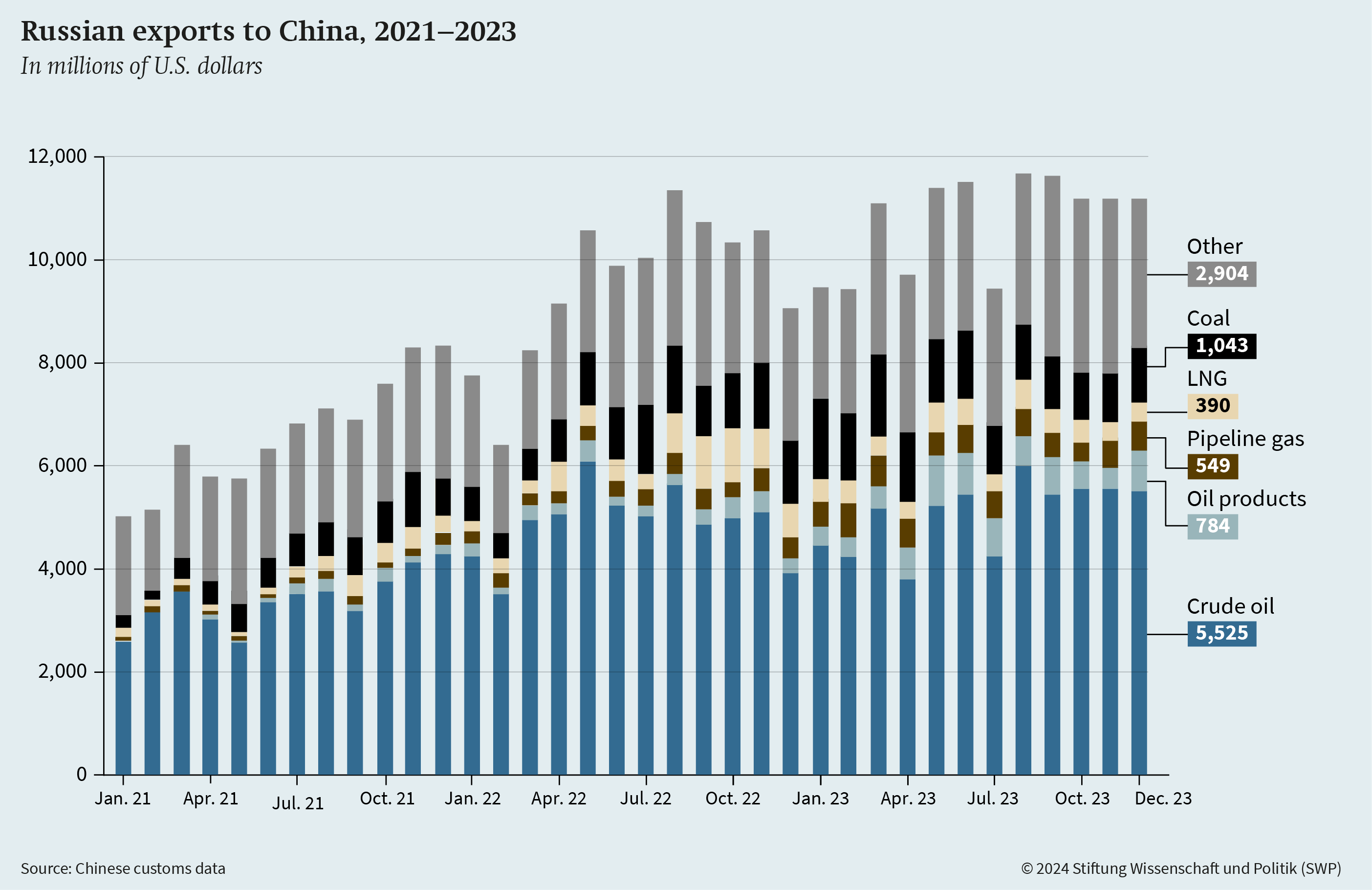

China has been one of Russia’s most important trading partners since the mid-2000s (see Figure 1). In 2010, the value of Russia-China trade surpassed that of Russia-Germany trade for the first time; but overall, until 2022, trade with the EU remained much more significant than trade with China. Then Moscow’s full-scale invasion of Ukraine catapulted Russia-China trade to a new level. In 2023, 36.5 percent of Russia’s goods imports came from China. This share was 3 percent at the beginning of the “Putin era” in 2000. China also plays a key role in Russian exports, accounting for 30.5 percent of Russian goods shipments in 2023. From China’s perspective, Russia remains a relatively insignificant economic partner, although Russia’s share of China’s trade turnover rose from 2.5 percent to more than 4 percent after 2022.

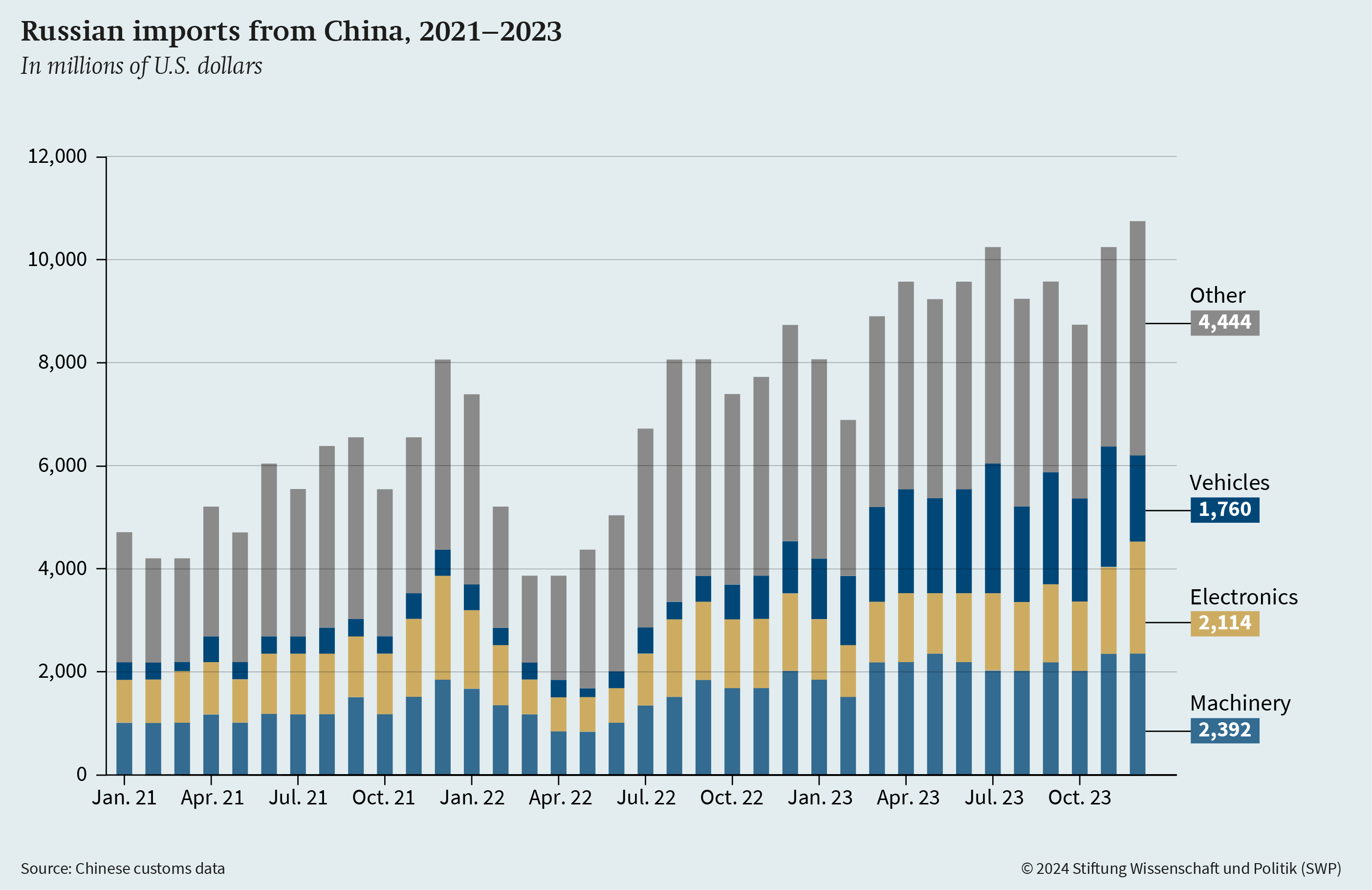

With the growth of bilateral trade, Sino-Russian economic relations have become increasingly asymmetric. This is evidenced not only by the volume of trade, but also by the types of goods exchanged. Until the mid-2000s, Russia imported mainly cheap, labour-intensive consumer goods from China (such as footwear, clothing, leather goods). Since then, imports from China have become increasingly high-value and technology-intensive. The share of capital goods has increased dramatically. More than half of total imports from China in 2023 were in the categories of equipment and machinery12 (23 percent), vehicles13 (21 percent), and electronics14 (15 percent).

The composition of Russian exports to China has also changed fundamentally. Until the mid-2000s, Russia exported hardly any hydrocarbons to the People’s Republic. Most of Russia’s shipments were industrial goods such as chemicals, machinery, and steel products. In contrast, Russia hardly exports any technology-intensive goods to China today (except arms, which are not included in publicly available trade statistics). Russia’s main exports to China in 2023 were fossil fuels15 (73 percent), metals and ores16 (11 percent) as well as wood17 (4 percent).

Other than fossil fuels and metals, Russia has also had some success exporting agricultural products to China. Vegetable oils and oilseeds18 (especially soybeans) accounted for 3 percent of Russian exports to China in 2023. For the Russian fishing industry19 (2.2 percent of Russia’s total exports to China), the People’s Republic is the most important customer on the Pacific coast. In contrast, trade in services has so far played a relatively small role in Sino-Russian trade, with the rapidly growing flow of Chinese tourists to Russia being an important exception.20

After the start of Moscow’s full-scale invasion and the West’s harsh sanctions against Russia, trade between China and Russia briefly collapsed. Imports from China fell from $7.3 billion in January 2022 to just $3.8 billion in March of that year. This collapse was mainly caused by the chaos and extreme uncertainty of the first weeks of the sanctions. Logistics and financial relations were disrupted in many areas. However, already in May 2022, Sino-Russian relations began to recover rapidly. By December 2022, Russian imports from China reached a new record high of $8.8 billion.

In the fourth quarter of 2023, China exported machinery and electronics21 to Russia at a rate of $4 billion per month. While the increase in machinery follows a multi-year trend, these goods are also key to the West’s technology embargo. EU exports to Russia in these categories have fallen by two-thirds because of the sanctions.

According to surveys conducted among Russian companies after the start of the full-scale invasion, the majority are looking for substitutes for Western supplies in China.22 While this is in line with exports of machinery and equipment, it does not seem to be reflected in the top line of direct Chinese imports of electronics to Russia, which only reached the level of December 2021 in the final month of 2023.

|

Figure 2

|

|

Figure 3

|

|

Figure 4

|

|

Figure 5

|

The most significant growth of Chinese exports to Russia occurred in vehicles trade. In the fourth quarter of 2023, over $2 billion worth of vehicles were delivered to Russia every month, a fivefold increase from the level before the full-scale invasion. Monthly imports of Chinese passenger cars23 rose from $100 million per month to $1.4 billion in November 2023. Exports of commercial vehicles to Russia also took off. In July 2023 alone, deliveries of Chinese semi-tractors24 to Russia amounted to $611 million, although the volume fell again afterwards to around $300 million per month.

The main reason for the increase in vehicles trade is the collapse of Russia’s domestic production capacity, which was mostly controlled by Western companies such as Renault, Volkswagen or Hyundai. When these companies withdrew and their factories stopped production, Russia was faced with a shortage of cars. Russian consumers were left with the choice of buying Western cars imported through third countries at very high prices, very basic Lada models, or Chinese brands. Before 2022, Russia also relied mostly on Western commercial vehicles such as trucks, while imports from China were insignificant. Now, China controls most of the Russian commercial vehicle market. In June 2023, Chinese models occupied places one to five in the list of the most popular trucks in Russia.25 While the Russian-made Lada Granta still tops the list of passenger cars sold, Chinese cars also dominate this ranking.26

Russia also receives many different components and materials that may not result in trade volume changes as drastic as those in the auto industry, but which are key to Russia’s ability to sustain its economy and mobilize production for the war. For example, Russia’s military industry remains dependent on Western semiconductors. After the spring of 2022, exports of semiconductors from China to Russia increased dramatically. Russian customs data show that a large part of these exports is not actually Chinese or “Made in China”, but were produced for Western companies such as Intel, Texas Instruments or Infineon in third countries, especially Malaysia and Taiwan, before the chips found their way to the Russian market via China. Although major Chinese IT companies turned their backs on Russia after 2022, fearing secondary sanctions from the U.S., the People’s Republic has become the largest sanctions-busting jurisdiction for dual-use goods.27

Like Russia’s imports from China, Russia’s exports fell briefly at the beginning of the full-scale invasion, but due to rapidly rising energy prices, this decline was much less pronounced. As early as April 2022, Russia’s exports to China reached a new all-time high of $9.2 billion. Crude oil volumes arriving to China by ship grew continuously, although the People’s Republic was not the main buyer of additional Russian oil after the EU introduced its embargo in late 2022: most of the oil previously sold to Europe ended up in India, which is easier to reach from Russia’s European ports.

Chinese investors not interested

While the partnership between Moscow and Beijing in foreign policy, security and trade relations grew ever closer, Chinese companies remained reluctant to invest in Russia and played only a minor role in the Russian economy. After Russia’s full-scale invasion began, Chinese investors became even more sceptical.

According to the latest available data on foreign investment published by the Central Bank of Russia (CBR), the stock of Chinese foreign direct investment (FDI) in Russia amounted to just $3.3 billion at the end of 2021, less than one percent of Russia’s total inward FDI stock ($610 billion).28 In reality, however, China’s share is somewhat larger. Some investments are not included in the bilateral statistics because they reach Russia through third countries, mostly Russia’s traditional offshore jurisdictions such as Cyprus, the Cayman Islands or the Bahamas.29

|

Express railway Moscow-Kazan: The eternal flagship project |

||

|

Since the first meeting of the Intergovernmental Russian-Chinese Commission on Investment Cooperation in 2014, the list of major bilateral investment projects has been headed by the plan to build a high-speed railway between the cities of Moscow and Kazan (located 700 km east of Moscow). To date, Russia does not have a dedicated high-speed rail network. The project was intended to be the flagship of Sino-Russian cooperation. The line would have been part of a long-distance connection between China and Europe via Russia. However, its construction is no longer being actively pursued.a Beijing had agreed to invest 52 billion rubles (€700 million at the time) in the first stage of construction and to provide the railway operator with an additional $1 billion at the second stage. In addition, the People’s Republic offered a loan of 400 billion rubles (then €5.7 billion) through the China Development Bank. In 2016, Beijing even abandoned its initial demands for Russian state guarantees for these loans.b |

But the project was fraught with problems. Russia’s state railway operator said the Chinese loans were too expensive and too small. At the same time, Russia began negotiations with a German consortium consisting of Siemens, Deutsche Bank, and Deutsche Bahn to build a high-speed rail line on the same route.c Russia was trying hard to consolidate its budget during this time, since it faced low oil prices and Western sanctions in 2014, and it cut funding for the high-speed rail project by 30 percent.d In addition, a legal dispute arose between the Chinese design firm planning the line and the Russian state railroad.e The plans to build the railroad were eventually shelved in 2020 due to lack of funds and projections of low passenger demand, which would make the line unprofitable. Instead of the high-speed railway to the east, Putin announced a new plan to build high-speed tracks between Moscow and St. Petersburg, without China, although the express train Sapsan has been serving this route for many years (without a dedicated express railroad).f |

|

|

a Anastasiya Boyko et al., “Vlasti otkazhutsya ot finansirovaniya VSM Moskva-Sankt-Peterburg iz FNB” [The authorities refused to finance the VSM Moscow-Saint-Petersburg from the National Welfare Fund], Vedomosti (online), 24 March 2022, https://www.vedomosti.ru/economics/ articles/2022/03/24/915136-vlasti-finansiro vaniya-vsm-moskva (accessed 19 August 2023). b “Kitay predostavit dlya VSM v Rossii 400 mlrd rubley na 20 let bez gosgarantiy” [China will provide 400 billion rubles for VSM without a state guarantee], Vedomosti (online), 3 June 2016, https://www.vedomosti.ru/ business/news/2016/06/03/ 643548-kitai-predostavit-400-mlrd-rublei (accessed 19 August 2023); Natal’ya Skorlygina and Anastasiya Vedeneyeva, “Yuani do Kazani” [Yuan until Kazan], Kommersant (online), 25 May 2016, https://www. kommersant.ru/doc/2995577 (accessed 19 August 2023). |

c Natal’ya Skorlygina, “Kitayskiye skorosti okazalis’ dorogovaty” [Chinese speeds proved to be expensive], Kommersant (online), 10 October 2017, https://www.kommersant. ru/doc/3435118 (accessed 19 August 2023). d Natal’ya Skorlygina and Anastasiya Vedeneyeva, “S oporoy na sobstvennyye shpaly” [With an accent on own swells], Kommersant (online), 19 October 2016, https://www. kommersant.ru/doc/3119744 (accessed 19 August 2023). e “‘Dochka’ RZD podala v sud na proyektirovshchikov VSM Moskva-Kazan” [Subsidiary of RZhD sues planners of VSM Moscow-Kazan], Interfax (online), 15 May 2020, https:// www.interfax.ru/russia/708900 (accessed 19 August 2023). f “Khusnullin ob”yasnil reshenie otlozhit’ proyekt VSM Moskva-Kazan’ vysokoy stoimost’yu” [Khusnullin explains decision to postpone the project VSM Moscow-Kazan with high costs], Interfax (online), 8 March 2021, https://www. interfax.ru/moscow/698235 (accessed 19 August 2023). |

|

The latest investment data from the Chinese Ministry of Commerce includes these indirect flows to some extent, reporting a stock of $10.6 billion for 2021. However, this does not alter the conclusion that Chinese investment has not played a significant role in the Russian economy so far. From the perspective of the People’s Republic, Russia is even less important: it accounts for only 0.4 percent of China’s total outward FDI stock.30

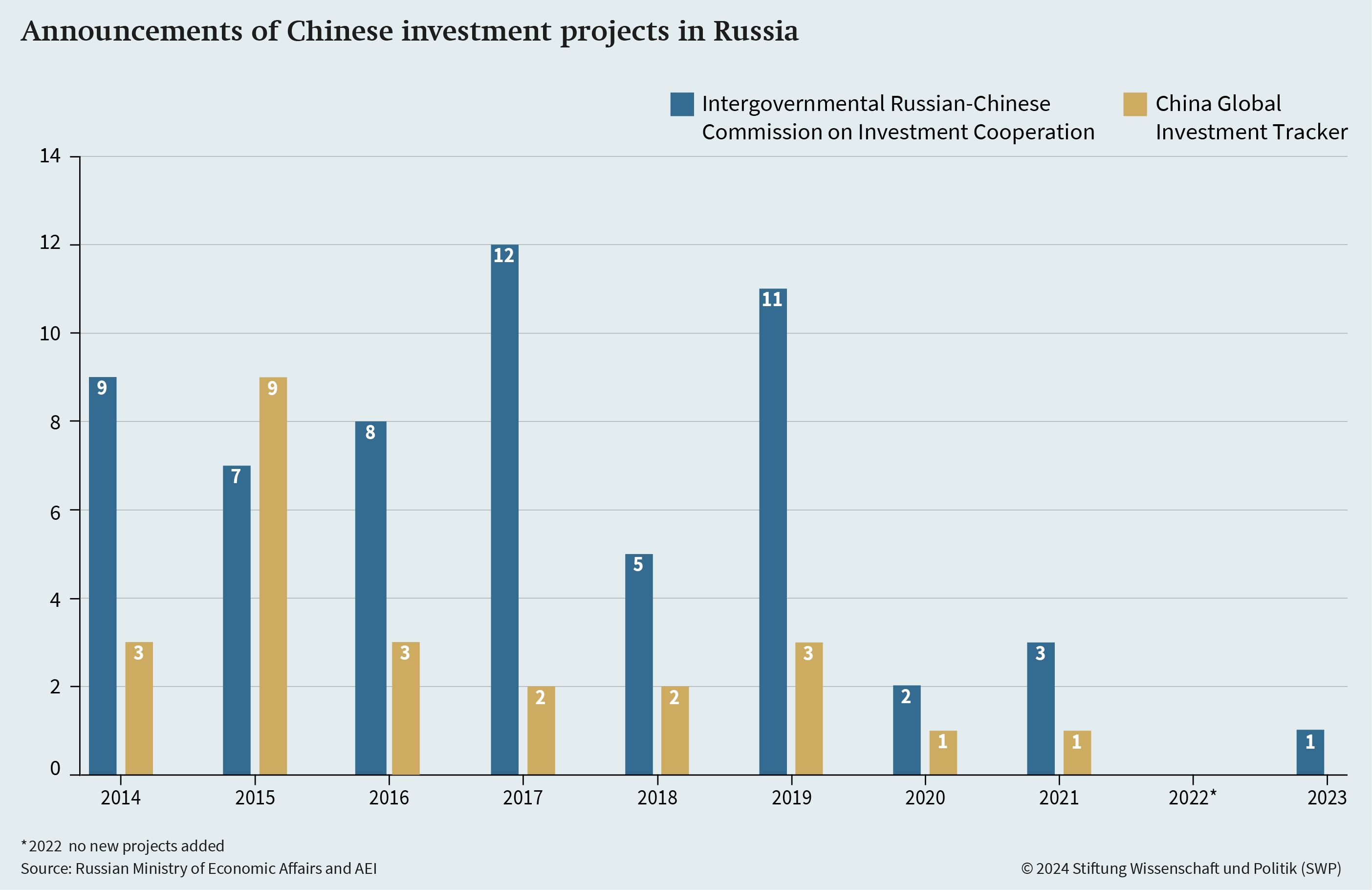

It is possible to get a better idea of the actual scale of Chinese investment in Russia from media reports and company press releases. The China Global Investment Tracker (CGIT) of the American Enterprise Institute collects these announcements for Chinese projects around the world.31 In the decade from 2012 to 2021, CGIT reports investment flows to Russia of about $4.5 billion per year, or 2.6 percent of the total value of Chinese projects abroad in that period. However, the CGIT also faces methodological challenges, as not all investment projects listed there have been realized to the extent originally planned. Nor does the tracker account for divestment of Chinese firms, which could lead to an exaggeration of the role that Chinese capital plays.

|

Figure 6

|

The sectors of the Russian economy that receive the most FDI from China are also those with the strongest exports to China. According to the CGIT, 55.2 percent (or $25 billion) of all FDI between 2012 and 2021 was in the energy sector. There were some very large investments in oil and gas production, but Chinese firms also bought into Russian electricity grids and power plants. Mining and metals accounted for 7.7 percent ($3.5 billion) of total Chinese FDI in Russia. In recent years, Russia’s chemical industry has also been the focus of Chinese investors (11 percent or $5 billion, including $4.5 billion in 2019–2021).

The Intergovernmental Russian-Chinese Commission on Investment Cooperation also compiles a list of significant bilateral investment projects at its annual meeting (see the list from November 2023 in the Appendix, p. 35ff.), but most of the projects do not go beyond the announcements over the years. Many of the projects on the Commission’s list were added in 2014–2019. The list is incomplete and includes projects of very different types and sizes. For example, China’s large investments in Russian Novatek’s LNG projects are missing. Despite these shortcomings, the list shows a similar trend to the data compiled in the CGIT. After the beginning of the Covid pandemic, the number of new projects decreased. After 2022, there are no new entries in the CGIT list (as of autumn 2023), and only one relatively small new project on the Commission’s list (as of November 2023). Meanwhile, the minutes of the Commission’s 2022 meeting, the first after the start of the full-scale invasion, refer to “unprecedented challenges” for Russia-China investment cooperation.32

|

Figure 7

|

The small number of Chinese investment projects reflects the lack of attractiveness of the Russian market for Chinese companies. Western sanctions are part of the reason why Russia’s long-term economic prospects are not promising. Russia is also not usually chosen as a production location to serve other foreign markets: it is difficult to find qualified workers and the infrastructure is underdeveloped. In Russia’s Far East, where Moscow had hoped to use Chinese capital to boost the regional economy, the lack of infrastructure is a major obstacle.33 Russia’s bureaucracy and red tape do not help either. Navigating the country’s formal and informal market barriers, which are often maintained by local business lobbies seeking to fend off Chinese competition, is difficult for Chinese companies that lack experience in the Russian market.

Western sanctions and the fear of secondary sanctions are also a direct obstacle for potential Chinese investors. In the wake of the 2022 sanctions, Russia has become almost toxic to Chinese companies, which are wary of jeopardizing their own access to Western markets. Russia’s own response to the sanctions exacerbates this problem, because Moscow has allowed Russian companies to be less transparent about their exposure to Western sanctions so as to protect them from the consequences. As a result, it has become more difficult for foreign companies to assess the risks of working with Russian partners. Since Russia is a relatively small market from a Chinese perspective, large corporations and banks are generally unwilling to take significant risks to invest in Russia.34 The only exception is Chinese state-owned enterprises, which can afford risky investments if they have political backing.

The lack of Chinese investment is disappointing for Moscow, which had hoped for greater Chinese involvement once Western companies left Russia in droves. In March 2023, Putin called on Chinese companies to invest, saying Moscow was ready to help anyone interested in replacing Western companies’ production in Russia.35 Chinese investors were in talks to take over the appliance factories of some Western companies.36 So far, however, there have been no concrete results. The situation is similar in the Russian automotive industry, which has been particularly hard hit by sanctions. There are reports of possible investors from the People’s Republic who could fill the gap left by Western companies. But the Chinese side does not appear to be interested in a long-term commitment, focusing instead on exporting its Chinese production to Russia or, at best, organizing the final assembly of semi-knocked-down vehicles in Russia.37

Strategic Cooperation

Although Russia and China are cooperating in a growing number of economic sectors, some are more strategically relevant for Russia than others. Traditionally, energy relations have been the most important pillar in bilateral cooperation. Large investments in energy infrastructure require stable and predictable diplomatic relations. Similarly, cooperation in the defence industry, considerable ties in the digital economy, and joint efforts in financial infrastructure and monetary cooperation are strategic because they often lead to long-term dependencies. In some of these strategic sectors, cooperation between Russia and China has intensified, while in others sanctions and the war are major obstacles.

Energy remains the backbone

Since the mid-2000s, the energy industry has been at the centre of Sino-Russian economic cooperation. Since then, crude oil has dominated Russian exports to China. A major milestone in the development of oil relations was the construction of the nearly 5,000-kilometer Eastern Siberia-Pacific Ocean (ESPO) pipeline, which was completed in 2012. After several expansions, the pipeline can currently transport about 80 million tons of Russian oil per year, or 1.6 million barrels per day. Almost half of these supplies, up to 35 million tons per year, go directly to China via a connecting pipeline. The rest is either processed in the Far East or loaded onto tankers at one of Russia’s Pacific ports.38

The construction of ESPO was agreed in 2009 and financed with a $25 billion loan from the China National Petroleum Cooperation (CNPC). In return, Russia’s state-owned oil company Rosneft guaranteed it would export 15 million tons of crude oil per year for 20 years.39 In 2013, it was agreed to double deliveries to China via ESPO and also to send Russian oil to the People’s Republic via Kazakhstan.40 Russian oil exports increased more than sixfold between 2010 and 2022, from 12.8 million tons (6 percent of Russia’s total oil exports) to 86.2 million tons (36 percent).41

So far, China has not been much help to Russia in the exploration and development of new oil fields, which are becoming increasingly difficult and technologically challenging. Chinese energy companies are not an alternative to highly specialized Western service providers, most of which withdrew from Russia after sanctions were imposed on the Russian energy industry. Large oil reserves on the Arctic shelf remain out of reach to the Russian industry, which could limit production volumes in the long run as more and more existing oil fields are depleted.42

In contrast to oil, natural gas has not played a significant role in the Sino-Russian energy relationship until recently. This changed in December 2019, when the key segment of the Power of Siberia (PoS) pipeline was inaugurated by Vladimir Putin and Xi Jinping. The PoS connects Chinese gas consumers to Russian gas fields in eastern Siberia. Plans for the pipeline were first developed in the 2000s, followed by years of varying negotiations. The final go-ahead came in 2014, shortly after the West unleashed its first round of sanctions against Russia’s energy sector. At the time, Gazprom estimated the total value of gas to be delivered to China under a new 30-year contract at $400 billion, or $13.3 billion per year, depending on the pricing formula. Initially, the capacity of the pipeline was planned to reach 38 billion cubic meters (bcm) per year by the mid-2020s.43 Gazprom hopes that China will agree to increase deliveries to 44 bcm by 2032. In 2023, 22.7 bcm were delivered to China via PoS, up from 15.4 bcm in the previous year.44

For Russia’s oil industry, Chinese energy companies are not an alternative to highly specialized Western service providers.

Gazprom wants to further develop its relations with China with new pipelines through the Altai Mountains or Mongolia and aims to increase its export volumes to 130 bcm in the long term.45 In 2022, Gazprom lost its most important foreign markets after the Kremlin decided to cut off supplies to the EU. Gazprom’s pipeline deliveries to the EU had amounted to 137 bcm in 2021 and fell to 25 bcm in 2023.46 Significant parts of the company’s huge production capacities on the Yamal Peninsula are now idle. Diversion of gas from Western Siberia to China is impossible without new pipelines.47 Plans to build a 50 bcm pipeline from there to China via Mongolia have advanced in recent years. However, it remains doubtful whether China’s demand prospects justify a new, very expensive pipeline of this size. This is likely the main reason why China has not given a green light to the project. Beijing may also be wary of antagonizing Europe by benefiting too openly from the Russian gas cutoff that caused turmoil in EU energy markets. If the pipeline is built, exports would most likely not begin until the 2030s.48

China is also a major buyer of Russian LNG. Before the war in Ukraine, Russia planned to significantly increase its LNG exports in the coming years to become one of the leading exporters on the world market. Russia’s former energy minister Aleksandr Novak estimated in late 2020 that LNG production would reach 68 million tons (about 94 bcm) annually.49 It is doubtful that this goal can be achieved after the West’s latest round of sanctions against Russia’s energy sector. Russia had been relying on Western technology provided by companies such as Germany’s Linde. In 2022, Russian LNG production totaled 32 million tons (44 bcm). Most of it came from Novatek’s giant LNG projects on the Yamal Peninsula, built with both Western and Chinese capital. A total of 6.5 million tons of LNG, or about one-fifth of Russian production, was exported to China in 2022.50 According to Chinese customs statistics, imports of Russian LNG rose to 8 million tons in 2023, while total Russian LNG production slightly declined.51

Russia’s exports of coal (lignite and hard coal) to China have also increased in recent years, rising from $1.9 billion (25.6 million tons) in 2017 to $4.6 billion (53.6 million tons) in 2021. Coal and lignite have been major elements of Russia’s growing exports to China during this period. Russia is interested in further increasing its coal exports to China because Western sanctions cut off its coal industry from European markets in 2022. In the year when Russia’s full-scale invasion began, coal shipments to China increased by 11.2 percent to 59.5 million tons, while total Russian coal exports fell by 7.5 percent to 210.9 million tons.52 Coal production is of great socio-economic importance to some Russian regions, especially the Kuznetsk Basin in Siberia. The main bottleneck for exports to China is Russia’s rail system, the main mode of transportation for Russian coal. It is already operating at maximum capacity. Since the value of coal is relatively low compared to its weight, it often makes more sense to use the limited capacity for higher-value goods such as crude oil.53

Finally, Russia and China have been cooperating in the field of nuclear energy for several decades. The People’s Republic’s largest nuclear power plant in Tianwan was built in the 1990s with the help of Russia’s state corporation Rosatom. In May 2021, Moscow and Beijing agreed to build four more reactors for nuclear power plants in Tianwan and Xudapu. Russia is also helping China build the CFR-600 fast reactor, which will receive its fuel from Rosatom. Compared to the export of oil, coal, or gas, nuclear cooperation plays only a minor commercial role in the Sino-Russian energy partnership. Nor is China dependent on Russian technology. On the contrary, it has become one of Russia’s main competitors in the global market for the construction of nuclear power plants.54

Russian advantage in arms technology is shrinking

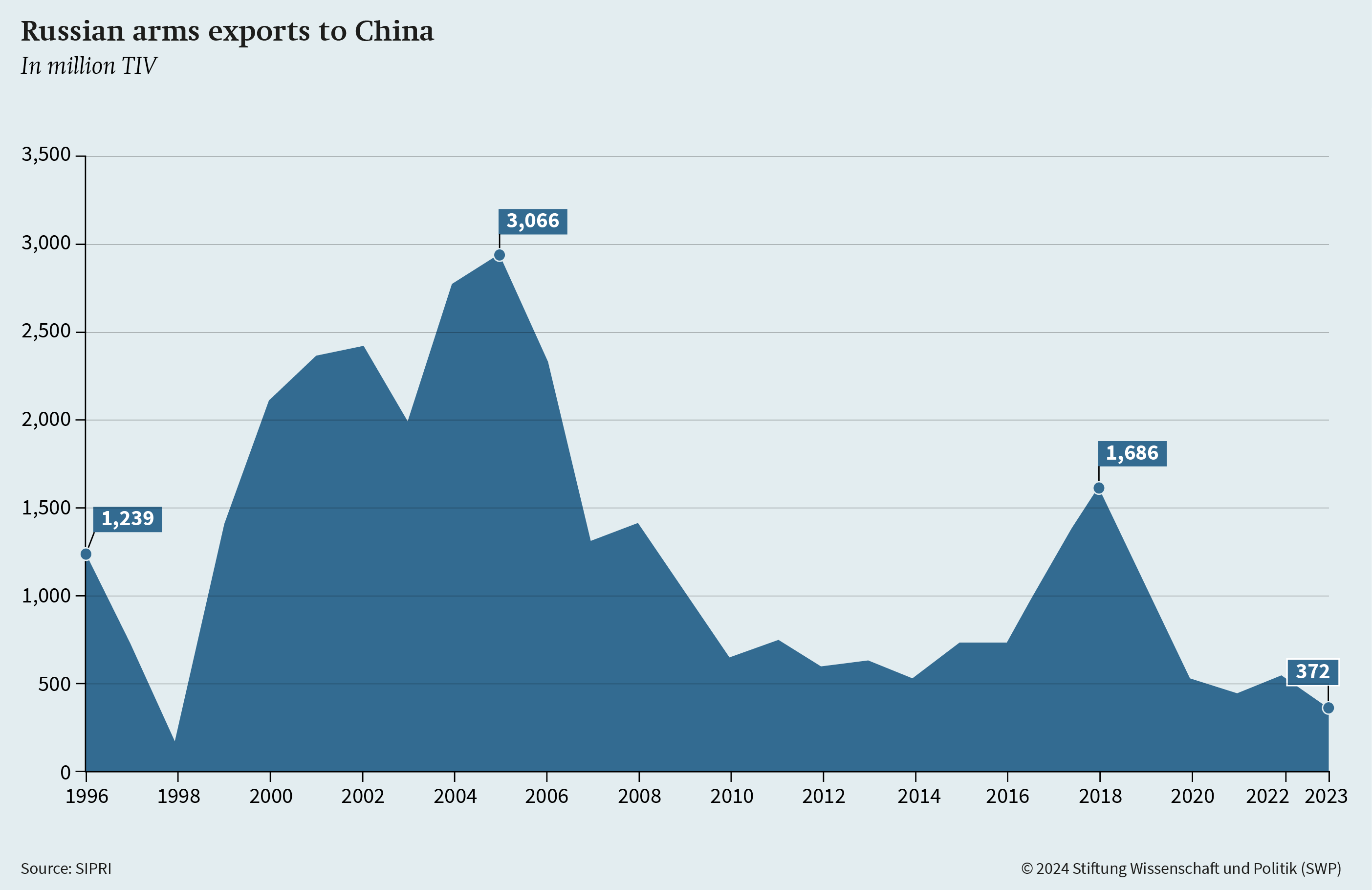

Military cooperation between Russia and China has increased significantly in the 2010s. Joint naval manoeuvres,55 military exercises on land56 and cooperation on a missile early-warning system57 show that neither side is shying away from closer engagement. Russian arms exports reversed their long-term downward trend in the period from 2014 to 2018, but fell again afterwards. In the early 2000s, Beijing was a major customer for Russian arms. The Stockholm International Peace Research Institute (SIPRI) estimates Chinese arms imports from Russia at 3 billion TIV in 2005.58 Arms trade between Russia and China declined thereafter, reaching a low of 561 million TIV in 2014. For many weapons systems, China had reduced its dependence on imports through licensed domestic production and the development of indigenous models, some of which were based on Russian designs. Fearing technology theft, Moscow has traditionally been reluctant to export its latest developments to the People’s Republic.59

|

Figure 8

|

Russia’s reluctance eased when it faced isolation from the West after the start of the Ukraine crisis in 2014. Moscow agreed to sell China its most advanced S-400 air defence system and 24 Su-35 fighter jets for a total of about $5 billion. Russia also exported helicopters (Mi-171), submarine technology, and a large number of jet engines on which China relies for some of its own fighter jet models.60 Negotiations on these deals had been underway for some time prior to 2014, but the deterioration in Russian-Western relations and Russia’s search for alternative partners most likely led to the final approval of these sales.61 In the years up to 2018, annual Russian arms deliveries to China grew to 1.7 billion TIV.

There was arguably also a military-strategic rationale behind Russia’s decision to provide China with advanced air defences and fighter jets. Both systems strengthen China vis-à-vis U.S. allies in the Pacific, such as Japan and Taiwan, but would not play a significant role in a hypothetical Russia-China military confrontation. Moscow also concluded that reverse engineering the exported systems would be time-consuming and would not add much to China’s own arms development efforts, while Russia would maintain its technological edge with next-generation weapons systems (S-500 and S-57).62

Moscow also expects China to gain ground with its own developments and become increasingly independent of Russian supplies. Ultimately, this could mean that the advantages of current Russian systems will disappear by the late 2020s.63 Only in the years leading up to this will China be interested in importing Russian weapons, giving Russia a limited window of opportunity to use its own capabilities in its relations with Beijing and benefit from them financially and politically.64

Against the backdrop of China’s own advances in arms technology, the future of Russian exports in this area is uncertain. SIPRI data show that Russian exports to China have started to decline again since 2018.65 Western sanctions are also making it more difficult for China to cooperate with Russia’s defence industry. Meanwhile, Russia needs all the weapons it can build to fight its war against Ukraine.

Due to its massive losses in Ukraine, Russia is now hoping to import arms and ammunition from China itself. Moscow has reportedly expressed interest in buying Chinese missiles, drones, armoured vehicles and specialized semiconductors.66 China’s export of components and materials to Russia that can potentially be used militarily has increased drastically since the start of the full-scale invasion.67 Beijing has assured the West that it has no plans to export weapons to Russia. American sources indicate that China has not supplied weapons to Russia on a large scale, but the possibility of supplies was discussed.68 Chinese companies are reportedly exporting large quantities of dual-use items to Russia, knowing full well that they are destined for the battlefield in Ukraine.69

Sino-Russian IT cooperation in trouble

Russia’s IT sector was one of the country’s few economic success stories in the 2010s. Companies such as Yandex, which evolved from a search engine into a digital giant rather like Google, were globally competitive. After a late start, Russian e-commerce has experienced explosive growth in recent years, driven by domestic online retailers such as Ozon and Wildberries. All of this has been made possible by widespread, affordable, and reliable fixed and mobile Internet access.

This success was one of the products of Russia’s integration with the Western economy. Western companies provided capital, technology, and even business model blueprints that together drove Russian digitization. Until the full-scale invasion, Russia had a vibrant domestic startup scene that looked to the West for the right network of entrepreneurs, venture capitalists, and business partners. For example, Ozon, the booming Russian online retailer, turned to Nasdaq in November 2020 to raise fresh capital.70 Russia’s network infrastructure and servers were also largely built and operated with the help of Western companies.

Russian services trade statistics also show the dominance of the West in Russia’s digital economy. In 2021, Russia’s total imports of IT services71 amounted to $6.7 billion. Of this, only $111 million came from China (including Hong Kong and Macau), while $3.6 billion came from the EU-27 and $698 million from the U.S. Eighty percent of all Russian imports of IT services came from the Western jurisdictions EU-27, U.S., UK and Switzerland, and only 2 percent from China.

The picture is similar for Russian exports of IT services. They totalled $7.2 billion, of which $2.3 billion went to the EU-27, $2.3 billion to the United States, and only $247 million to China (including Hong Kong and Macau). The EU-27, U.S., UK and Switzerland accounted for 76 percent of Russia’s IT services exports, while China accounted for only 3 percent.

However, led by Huawei and Alibaba, several of China’s digital economy behemoths began actively expanding into Russia in 2018. The companies were not only interested in selling to the Russian market. They were also looking for qualified Russian IT professionals. In just a few years, Huawei established a dense network with Russia’s leading research institutes and universities in the field of IT and telecommunications. The company set up its own research centres in university cities such as Nizhny Novgorod and Novosibirsk,72 awarded research grants, and organized competitions for IT students.73

From 2019 to 2020, the number of Russian employees in Huawei’s research and development centres grew from 550 to 900. The Chinese company had plans to hire 1000 additional specialists by 2024.74 Moreover, in June 2019, Huawei acquired the facial recognition software of the Russian startup Vocord for $50 million and brought most of its developers on board. Other Chinese companies are also increasingly interested in Russia’s expertise in artificial intelligence, such as Dahua Technology, which is working with Russia’s NtechLab on face recognition technology.75

After the start of the full-scale invasion of Ukraine, the prospects for Sino-Russian IT cooperation deteriorated drastically.

AliExpress, a subsidiary of China’s Alibaba, is a leading competitor in Russia’s fast-growing e-commerce sector. Russia has become Alibaba’s most important foreign market. The company planned to build on this success and expand into other post-Soviet markets with the help of Russian partners. In December 2018, Alibaba Group signed a joint venture agreement with the Russian Direct Investment Fund (RDIF), the mobile operator Megafon, and the internet conglomerate Mail.ru.76

Megafon and Mail.ru are part of the media empire of Russian businessman Alisher Usmanov, who has close ties to the Kremlin and often handles politically sensitive assets (especially via mass media) for the Russian government. Usmanov was sanctioned by the U.S. and EU in 2022 and has since retired to a quieter life in his native Uzbekistan. Cooperation on e-commerce was not his only project with Alibaba: he also planned to cooperate on digital payments with Alibaba’s Ant Group.77

Russian state-owned companies also partnered with Chinese companies in the IT sector. Sberbank turned to Huawei as a strategic partner for its cloud business. The bank’s director, German Gref, had planned to transform Sberbank into a modern digital services provider, but Western sanctions put an end to those ambitions.78

Chinese companies also have a significant presence in Russia’s digital infrastructure. Huawei has a big market share in Russia’s mobile networks, although Russian operators also continue to use Western technology from Ericsson and Nokia, particularly in the larger cities. From Moscow’s perspective, Huawei was not seen as more trustworthy than Western vendors. The Russian telecom regulator only differentiated between foreign and Russian-made equipment. To reduce foreign dependencies, the state corporation Rostec was supposed to develop a local 5G alternative by 2024.79 There was speculation about an exclusive partnership between Rostec and Huawei, as the Russian state corporation does not have the experience, capacity or financial resources to perform the task alone, but this partnership never materialized.80

After the start of the full-scale invasion of Ukraine and Western sanctions in 2022, the prospects for Sino-Russian IT cooperation deteriorated drastically. Immediately after the invasion began, Huawei stopped supplying network and server technology to Russia (as did Nokia and Ericsson), bringing the development of mobile networks in Russia to a halt.81 Over the course of 2022, Huawei partially withdrew from Russia, closing local stores and offices and offering employees the opportunity to relocate abroad, such as to Kazakhstan, to work for Huawei outside of Russia.82

Huawei urged programmers of apps for its own mobile operating system, HarmonyOS, to strictly comply with U.S. sanctions, while deleting the apps of sanctioned Russian banks from its AppGallery store. It also blocked the Russian state-sponsored credit card MIR on its HuaweiPay mobile payment system.83 The U.S. sanctions also put an end to Huawei’s cooperation with Sberbank; the Russian bank was forced to spin off and sell its cloud business in May 2022.84 But Huawei did not leave Russia altogether. It continued to hire Russian IT specialists. The work in its Russian research and development centres continues. In the summer of 2022, Huawei hired about 250 former Intel experts in Nizhny Novgorod, after the American company closed its local branch.85

The promising cooperation between Alibaba and its Russian partners also came to a halt after Western sanctions were imposed. Both Alisher Usmanov and the RDIF were sanctioned in March 2022, creating several compliance issues for Alibaba. The fact that Alibaba also operates in Ukraine made things even more complicated. Shortly after the full-scale invasion began, the company informed its Russian partners that it did not intend to continue investing in the joint venture. In turn, RDIF and Usmanov’s holdings stopped their participation as well.86 In August 2022 it became known that one of the joint venture’s shareholders, the Mail.ru subsidiary VK, had written off its entire 10 billion rubles stake in the project.87

Chinese yuan – for lack of a better option

When the first round of financial sanctions was imposed on Russia in 2014, Moscow realized that its integration into Western capital markets and its reliance on Western currencies were a key vulnerability for its economic security. Since Beijing also sees the dominance of the U.S. dollar as a problem, the “de-dollarization” of trade and finance became a central topic of discussion in many meetings between the presidents and representatives of China and Russia.88 The first concrete steps towards closer currency cooperation came in 2014, when the central banks of Russia and China agreed on a swap deal of up to 150 billion yuan. The agreement gives both sides access to liquidity in each other’s currency. In 2015, the Russia-China Financial Council was established by Russia’s Sberbank and China’s Harbin Bank. In June 2019, the two sides signed an agreement to promote the use of their national currencies in bilateral trade, which at that time was still dominated by the U.S. dollar.89

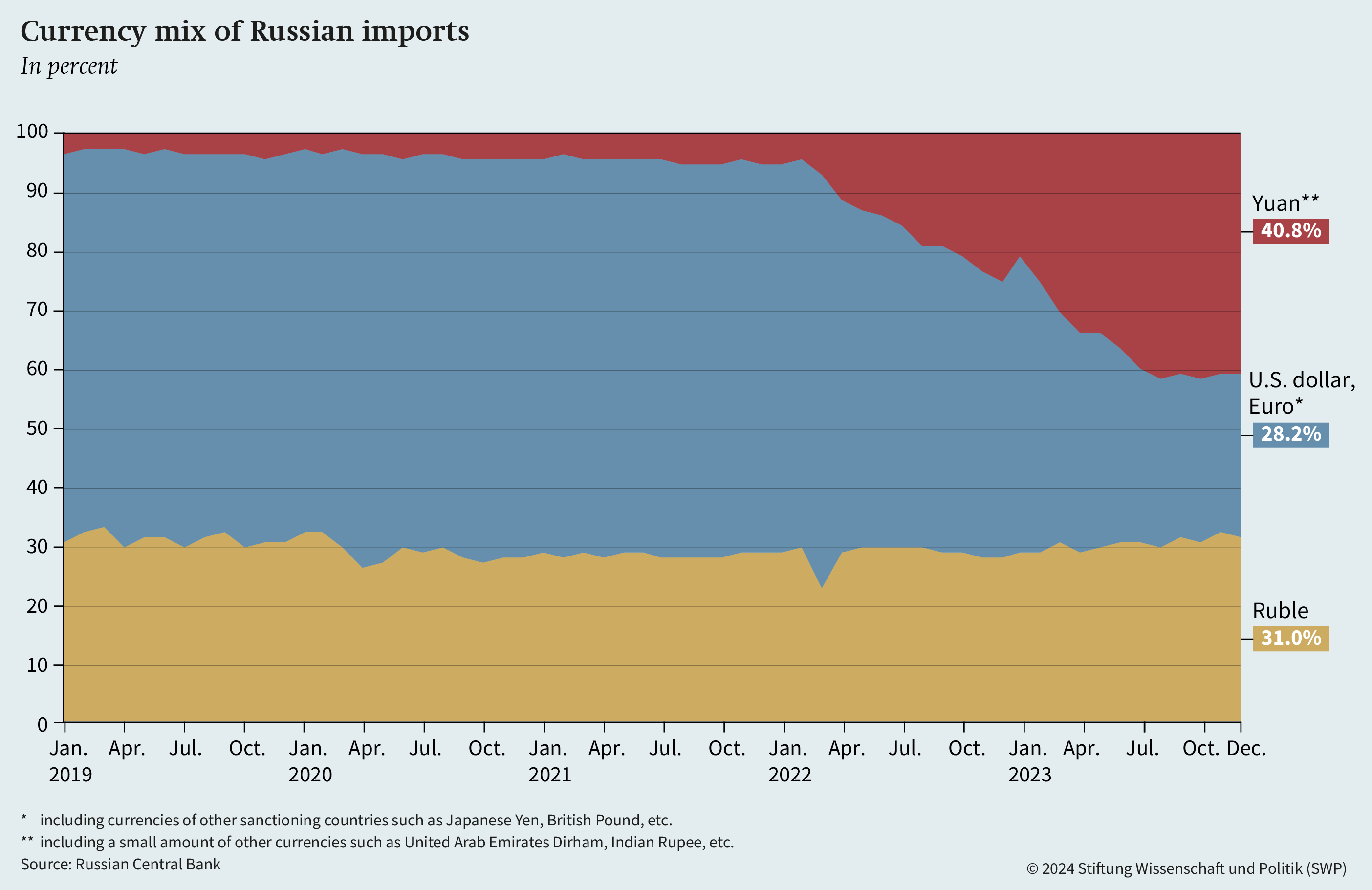

Overall, however, the Sino-Russian “de-dollarization” project remained an empty promise from 2014 to 2022. Moscow intensified its attempts to become less dependent on the U.S. dollar but saw other Western currencies such as the euro or the Japanese yen as more practical solutions. Unlike the yuan, the yen and the euro are freely convertible, making their use much easier. During Donald Trump’s first presidency, Moscow feared mainly unilateral U.S. sanctions, while the prospect of massive, coordinated sanctions by all G7 countries seemed rather remote. For example, after a wide-ranging package of sanctions announced by the U.S. in April 2018, the Russian Central Bank reduced the share of the U.S. dollar in its reserves, but mostly shifted the holdings to yen and euro, and increased the share of yuan only to 14 percent of its currency reserves.90

Until 2022, the Chinese yuan played a negligible role in Russia-China trade. But this changed when the avalanche of Western financial sanctions hit Russia after the full-scale invasion began. The sanctions made it very complicated, expensive, and in some cases impossible for the Russian government, businesses, and individuals to use the U.S. dollar, euro, or yen. Most of Russia’s major banks were unable to offer accounts or transactions in Western currencies. The Central Bank of Russia lost access to its currency reserves in the West. As a result, the Chinese yuan gained in importance, although it did not become an equivalent substitute for Western currencies.

In December 2023, 37.5 percent of Russian total imports and 40.8 percent of Russian total exports were settled in yuan. The Chinese currency is dominant in Russia-China trade, while it still plays a very small role in Russia’s trade with third countries, where only 5 percent of payments are settled in yuan and the U.S. dollar continues to play the leading role.91 The intensive use of the yuan also led to more active trading of Chinese currency on the Moscow Exchange, where the share of the ruble-yuan currency pair in total trade grew from 0.32 percent in February 2022 to almost 40 percent in May 2023.92

Nevertheless, Western sanctions not only encouraged financial cooperation between Russia and China, but also disrupted it. Fearing U.S. secondary sanctions, Chinese banks became much more cautious in their dealings with Russian banks. Several sanctioned Russian banks had planned to offer credit cards linked to China’s UnionPay system after losing access to MasterCard and Visa, but UnionPay refused, leaving Russia’s domestic MIR system as the only alternative (which in turn is not accepted by China’s AliPay and HuaweiPay payment services). Deeper integration of Russian banks with the Chinese interbank settlement system CIPS, which offers similar functionality to the financial messaging provider SWIFT, has made little progress because China does not want CIPS to become a shady alternative for sanctions evasion.93

Due to sanctions, the Chinese yuan became Russia’s only reserve currency.

Russian households have also shown a growing interest in the yuan as a store of value. During 2022, many Russian banks began offering yuan savings accounts to their customers. By February 2023, the number of these banks had risen to 50. The Chinese currency is attractive to Russians because it can protect them against inflation in Russia or a devaluation of the ruble, while not being directly exposed to Western sanctions. In many cases, bank fees for yuan accounts have also been lower. However, yuan deposits still account for only a small share of the total foreign currency deposits held by Russian households. In February 2023, their total value was $6 billion, while the value of all household foreign exchange deposits was $53 billion.94

Russian banks have also started to offer yuan loans to Russian companies.95 Some of Russia’s largest exporters have issued their own yuan bonds, which are traded on the Moscow Exchange. The growing role of the yuan in the debt market is a natural consequence of changes in trade settlement, as Russia’s exporters try to hedge against exchange rate fluctuations. Since a large part of export revenues will be denominated in yuan, it makes sense to finance projects and repay loans in the same currency. The first yuan bond was issued by Russian aluminium giant RUSAL in August 2022. Other commodity exporters such as Rosneft (oil), Polyus (gold), Metalloinvest and Norilsk Nickel followed soon after.96

As a result of sanctions, the Chinese yuan became the sole reserve currency for Russia’s Central Bank and Ministry of Finance. The sanctions forced Moscow to change the distribution of its reserves, which will now consist almost entirely of gold and yuan. Other non-Western currencies are impractical for the Russian government, either because their exchange rate is too volatile, or there is not enough liquidity, or the economies behind the currency are not large enough. The Finance Ministry has changed its fiscal rule, not only relaxing it to allow for more spending on the war, but also using gold and yuan as the only liquid investments if the price of oil rises above $60. In the future, up to 80 percent of Russia’s liquid reserves in the National Welfare Fund will consist of yuan.97

China’s domestic capital market, however, does not play a significant role for Russian companies or the Russian government. Although RUSAL already issued a bond in China in 2017, becoming the first Russian company to do so,98 Chinese capital controls severely limit what Russian companies can do with funds raised in China. Chinese investors have also not replaced Western investors in Russian ruble government bonds, up to one-third of which used to be held by (mostly Western) foreigners. Currently, placing government bonds in China is not a realistic hope for Moscow because of the restrictions imposed by China’s capital controls.99

Russia’s reliance on the yuan exposes it to numerous economic and political risks. The yuan’s exchange rate is essentially controlled by Beijing. If the Chinese leadership decided to artificially devalue the yuan to boost exports, Russian deposits and reserves would also be devalued.100 The liquidity of yuan trading in Russia is also not yet comparable to the markets for Western currencies before the full-scale invasion, which sometimes limits the ability of market participants to buy or sell yuan.

|

Figure 10

|

The composition of Russia’s currency reserves, which is dominated by the yuan, also does not correspond to the share of currencies in Russia’s payments of imports, in which the U.S. dollar still plays a significant role. The share of currencies classified as “toxic” by the Central Bank of Russia has fallen from 65 percent to around 30 percent in 2023, but it has stabilized there (see Figure 9). In the event of a currency crisis, yuan reserves could only be used to pay for a certain share of Russian imports. In addition, Beijing would have to agree to the sale of reserves, which would put a strong political lever in the hands of the Chinese government. In the unlikely scenario of deteriorating Sino-Russian relations, Moscow may regret its bet on the Chinese currency.101 In this scenario, the fact that after Western sanctions were imposed Russia had no realistic alternative will not provide much comfort to Moscow.

Russian Elites and Public Opinion

A small group of elites with close personal ties to Russian President Vladimir Putin, who control much of Russia’s energy industry and military-industrial complex, have been the main beneficiaries of the deepening economic partnership with China. Their decisions tend to carry more weight in bilateral relations than the policies of formally responsible ministries such as the Foreign Ministry or the Economy Ministry. The high degree of personalization of Russia-China relations, and the lack of China competence among key figures on the Russian side, create risks for Russia. In addition, conflicts of interest between different actors in the Russian regime make it difficult to shape economic relations with China to Russia’s advantage. While there are incentives for Russian officials to intensify cooperation with China, this often leads to an exaggeration of success. Russian officials and companies have signed numerous “memoranda of understanding” (MoU) that have failed to produce concrete results.

Beijing bets on Putin’s entourage

When it comes to controlling key strategic sectors of the Russian economy, Putin trusts only a small number of loyal elites, most of whom have been part of his personal network for over 30 years.102 Since the energy industry and the military-industrial complex have played a key role in Russia-China cooperation over the past two decades, it is not surprising that the same elites play a crucial role in Russia’s relations with the People’s Republic.

Among the Russian recipients of Chinese capital, billionaires and business partners Gennady Timchenko and Leonid Mikhelson stand out. Their companies, Novatek and SIBUR, account for one-third of all Chinese direct investment in Russia listed in the CGIT ($8.7 billion) for the period 2011–2023. Both men have also received substantial Chinese bank loans. Novatek’s Yamal LNG plant received Chinese loans of $12.1 billion and equity investments of 20 percent (China National Petroleum Corporation, CNPC, invested $1 billion) and a further 9.9 percent (China’s Silk Road Fund invested $1.2 billion).103 Chinese investors are also involved in Novatek’s second major LNG project, called Arctic LNG 2. CNPC and the China National Offshore Oil Corporation have invested 10 percent of the equity (about $2 billion each). In addition, a $5 billion loan is expected from the China Development Bank.104 Chinese companies also bought into SIBUR, Russia’s largest petrochemical company. Sinopec and the Silk Road Fund each bought a 10 percent stake for $1.2–1.3 billion, according to the CGIT.

Russia’s state oil company Rosneft, controlled by Igor Sechin, has also benefited from substantial Chinese loans and investments. In 2006, Rosneft used Chinese loans to finance the takeover of Mikhail Khodorkovsky’s oil business after he was imprisoned and expropriated. Later, Chinese banks provided loans for the construction of the ESPO pipeline. More recently, two Chinese investors bought two oil fields owned by Rosneft subsidiaries for a total of $2.6 billion. Another example is the Russian billionaire Oleg Deripaska, whose companies received $3.8 billion in Chinese investment between 2011 and 2023. The main beneficiary of the Sino-Russian arms trade is Russia’s state corporation Rostec, headed by Sergey Chemezov, a close Putin ally since they worked together for the KGB in Eastern Germany in the 1980s.105

Beijing offers the elites that are close to Putin billions of dollars in direct investment and loans.106 For China, this reduces the political risk in the economic relationship while Putin and his entourage are in power in Russia. The bilateral flagship projects are supported at the highest political level on both sides. Especially for Chinese investors, it is crucial not to bet on the wrong companies in Russia’s highly opaque business environment. The advantage of partnering with Putin’s allies is that bureaucratic hurdles are easy to overcome and direct access to the president is possible when needed. However, it also means that China is tied to the elites currently in power in Moscow. This gives Beijing a strong economic interest in the survival of the current political regime, which in turn benefits Vladimir Putin.

A key risk for Russia is the low level of China competence among Russia’s economic elites.107 This “illiteracy” has concrete consequences: in 2017, Rosneft planned to organize the sale of a large package of its shares worth $9.1 billion to the Chinese energy holding CEFC, then a fast-growing private company. To the surprise of the Russian side, the deal fell through at the last minute when the founder of CEFC was arrested in China and disappeared.108 After the Chinese state seized CEFC, it cancelled its investment in Rosneft, even though the Russian state bank VTB had already agreed to finance most of the acquisition.

The dominance of a small number of business elites, controlled only by Putin’s personal network, weakens the Russian bureaucracy that is formally responsible for foreign and economic policy. The ministries responsible for economic relations with China, the Foreign Ministry, the Ministry of Economic Development and the Ministry for the Development of the Far East, as well as the administrations of the border regions, often have less influence on economic cooperation with China than a few powerful figures from within Putin’s personal circle.109 As a result, Russia’s China policy tends to be dominated by narrow interests and opaque backroom deals rather than an overarching strategy.

This is particularly problematic when the narrow interests of certain elite figures conflict with Russia’s strategic national goals. One example is energy exports. It would improve Russia’s economic security if it were able to diversify its energy exports so as not to become overly dependent on China, but also to export to other Asian economies. This diversification was initially undermined by Rosneft CEO Igor Sechin.110 In 2013, he committed to a long-term relationship with China because he needed capital to finance the expansion of his own oil empire in Russia.111 China sometimes manages to play Russian energy companies off against each other. The close cooperation with Novatek was a reaction to long negotiations with Gazprom that did not produce the result China wanted.112 Novatek and Rosneft are both using their relationship with China to put pressure on Russia’s pipeline gas export monopoly, Gazprom.113

Potemkin cooperation in the regions

At the lower levels of the Russian state, cooperation with China is driven primarily by informal incentives. For Russian governors, ministerial bureaucrats, and businessmen, an ambitious MoU with a Chinese partner can earn attention from high places in Moscow or a ticket to the next high-level meeting between Putin and Xi.114

However, the result of these incentives is an inflation of bilateral projects that never get beyond the announcement stage. Even state-owned enterprises fail to follow up on these announcements if they are purely politically motivated. After a state visit, the impressive plans are often shelved if there is no real business interest behind them.115 Some businessmen and politicians in the Far East have gone even further and simply invented large-scale cooperation projects which, it turned out later, the supposed Chinese partners were not even aware of. These Potemkin successes of Sino-Russian cooperation led to no concrete results but still managed to create fears and resentment among the Russian population in the Far East.116

There are also contradictions in the political incentives for regional governments, because closer cooperation is not the only priority Moscow has set for the periphery. Attracting Chinese investment is an uphill battle for the relatively poor and underdeveloped border regions. Regional governments do not often have control over investment parameters such as taxation, regulation or subsidies to compete as a destination for Chinese companies. The regions are also dependent on federal transfers. As a result, for many, lobbying for federal funds is more promising than trying to attract Chinese investors. To get more transfers from Moscow, it sometimes helps to promote the region as a geopolitical outpost on the Chinese border. To underscore this point, regional governments do not shy away from portraying China as a possible threat to Russia.

This contradictory attitude is also found in regional development strategies in the Russian Far East, where proximity to China is portrayed as both an opportunity and a threat. Access to cheap labour and Chinese investment are cited as economic advantages, while uncontrolled migration is presented as a risk. Some Russian regions even point out that being close to China makes it harder for them to develop because they cannot compete with Chinese regions in attracting foreign investors from third countries. The obvious hope behind these concerns is that the federal centre will send more subsidies to the borderland with China.117

Sinophobia is not an obstacle

Although there is a relatively open and controversial debate about China in Moscow, with many experts and some politicians expressing scepticism about too close a relationship with China, xenophobia or Sinophobia is not a real obstacle to bilateral economic relations. The leadership in Moscow is no longer worried about mass migration from China to the sparsely populated Russian Far East, and the prospect of Chinese claims to Russian territory is seen as remote. Surveys in Russia show that China is generally perceived in a positive light, which is certainly a reflection of the pro-China state propaganda in Russia.118 There is also respect for China’s economic success among Russians, with two-thirds of respondents saying they believe China is developing more successfully than Russia.119 However, the positive attitude towards China as a country on the world stage is not reflected in Russians’ attitude toward the Chinese people. Surveys show little willingness to open up to the Chinese, suggesting lingering resentment or racism.120

In some cases, Chinese investment projects lead to a popular backlash, but local protests are mostly linked to other issues, often environmental concerns, and are sometimes exploited by local politicians. Overall, anti-China protests in Russia are rather rare and not comparable in scale to similar protests in Kazakhstan.121

The most notorious protest case against Chinese investors took place at Lake Baikal, but it reverberated all the way to Moscow. A Chinese company planned to bottle drinking water from Lake Baikal for export to China. Local environmentalists claimed that the project would endanger a protected bird sanctuary. Local politicians then discovered the issue for their election campaigns. The protest movement gained a few supporters with Instagram fame in Russia, who brought the issue to a wider audience and to Moscow. In 2017, an online petition calling for an end to the Chinese project was signed by more than a million supporters. Eventually, then-Prime Minister Dmitry Medvedev also expressed concern about the project. Shortly thereafter, the Chinese construction permit was suspended by a Moscow court.122

It is no coincidence that politically sensitive issues such as environmental protection are sometimes linked to the activities of Chinese investors. Particularly in the Far East, there are fears that Chinese companies are colluding with corrupt officials to plunder the region’s natural treasures. There are similar concerns about the Siberian timber industry, which produces mainly for export to China. Chinese investors in Russian agriculture faced similar problems when they were accused of spoiling Russian soil with the wrong kind of fertilizer.123 In some cases, these concerns about corruption and environmental problems are justified. However, the association with xenophobia tends to make these protests more successful with a wider audience and leads to a more lenient government response. Of course, Russian officials and politicians are more sympathetic to the demands of environmental activists when the target of their criticism is a ruthless foreigner rather than Russian business or the government’s own environmental policies.

Outlook

Russia’s war of aggression against Ukraine and the economic sanctions imposed have triggered a far-reaching decoupling of the Russian economy from the West. Russia is at the beginning of another economic transition, the consequences of which will only become clear in the long run. Although the sanctions regime itself has changed little since the second year of the full-scale invasion, the gulf between the West and the Russian economy is widening with each passing year, as many of the measures take a while to have an effect. It is very unlikely, even in the longer term, that Russia and the West will again move closer together economically, since sanctions are likely to remain in place for an extended period of time. This means that the prospects for a further deepening of Sino-Russian cooperation are good. The gradual reorientation of the Russian economy towards China will also take time. Both sides need to gain more experience with each other, and new infrastructure must be built. Perhaps the most visible progress can be seen in the Russian car market, which is already largely in Chinese hands. In other areas of the Russian economy, the same transition could take until the end of the 2020s.

The longer-term prospects of the Russian economy depend on what kind of economic partner China can and is willing to become in the future. So far, Russian economic relations with China have intensified mainly on the trade front, but Chinese companies have avoided making lasting commitments to the Russian market. For China, Russia is interesting as an export destination and as a source of natural resources, rather than as an intermediate link in Chinese value chains. For Russia, this means that it could be degraded to a supplier of resources and a buyer of Chinese finished goods, which means less value added in Russia. The result would be lower living standards for Russians and less industrial potential in the future. This kind of cooperation with China would make Russia more like a real petro-state, while Russian manufacturing would be eroded.

Russia’s economic dependence on China could also affect the political dynamic between Beijing and Moscow. However, it is not yet clear how and when China would use its economic leverage for political goals. So far, the Chinese leadership does not appear to be exploiting its dominant position vis-à-vis Moscow. It is unclear what kind of demands the People’s Republic might formulate. Russian President Vladimir Putin is unlikely to compromise in his war against Ukraine. The Kremlin would probably tolerate even greater economic isolation rather than change course. At the same time, Beijing wants Putin to survive politically. In the eyes of the Chinese leadership, Putin is still the guarantor of the Sino-Russian partnership. Any political instability within China’s closest geopolitical partner could even damage the reputation of Chinese leader Xi Jinping. Therefore, Beijing is unlikely to use its leverage to push Putin into a corner in a situation that is already challenging him and his grip on power. At least in the short term, it is unclear what political dividend China could draw from its economic dominance.

For the EU, the most important issue in Sino-Russian economic cooperation is the effectiveness of Western sanctions. China’s help has been crucial in cushioning the impact of sanctions on the Russian economy. Depending on the course of the war in Ukraine and Beijing’s attitude toward Moscow, Sino-Russian economic cooperation could lead to more conflict between the West and China. Russia has significantly expanded its arms production, and is facilitated by the parts and machinery it imports from China. If the situation in Ukraine again becomes more threatening to Kyiv, China’s role as Russia’s economic enabler will rise high on the Western agenda. More Chinese companies will find themselves in the crosshairs of Western sanctions. If the war goes the other way, with Ukraine becoming increasingly successful and Russian military losses eventually threatening Putin’s political survival in Moscow, China may opt for more open and direct support for Russia, including the supply of weapons. If this were to happen, relations between the EU and the People’s Republic would certainly be plunged into a deep crisis.

Appendix

List of Russia-China cooperation projects

|

Source: 10th annual meeting of the CIC: Minekonomrazvitiya Rossii, Protokol 10-go zasedeniya Mezhpravitel’stvennoy Rossiysko-Kitayskoy komissii po investitsionnomu sotrudnichestvu [Protocol of the 10th meeting of the Intergovernmental Russian-Chinese Commission on Investment Cooperation], 20 November 2023, |

https://www.economy.gov.ru/material/file/f18a2042fc023f7e4344e4602abb1164/Protokol_10-go.pdf (accessed 19 March 2024). The list is not a complete representation of bilateral investment projects, but shows the projects deemed most important by the CIC. |

|

|

|

|

|

Federal district |

Planned since |

|---|---|---|---|---|---|

|

1 |

Construction of the Moscow-Kazan express train line |

Infrastructure |

(n/a) |

2014 |

|

|

2 |

Railway bridge in Nizhneleninskoye |

Infrastructure |

Jewish Autonomous Oblast |

Far East |

2015 |

|

3 |

Special economic zone for wood processing in Tomsk |

Wood industry |

Tomsk |

Siberia |

2014 |

|

4 |

Cooperation zone for forestry |

Wood industry |

Transbaikalia |

Far East |

2017 |

|

5 |

Joint production of nitrile butadiene rubber in Shanghai |

Chemistry |

(China) |

2014 |

|

|

6 |

Polyethylene production complex in Svobodny |

Chemistry |

Amur |

Far East |

2014 |

|

7 |

Construction of a refrigerator factory (Haier) |

Consumer goods |

Tatarstan |

Volga |

2015 |

|

8 |

Industrial complex for the production of aluminium in Henan |