From Competition to a Sustainable Raw Materials Diplomacy

Pointers for European Policymakers

SWP Research Paper 2023/RP 01, 24.02.2023, 45 Seitendoi:10.18449/2023RP01

Forschungsgebiete-

German and European businesses are highly dependent on metals. Demand for these raw materials is expected to grow even further as they will be needed for the green energy and electric mobility transition, digitalisation and other emerging technologies.

-

Geopolitical developments influence security of supply. China’s central role in mineral supply chains is a major factor of uncertainty in this context.

-

The European Union has set ambitious sustainability targets. Implementing these in complex multi-tier metal supply chains is no easy matter, given the magnitude of environmental and human rights risks.

-

Nevertheless, sustainability should not be sacrificed for security of supply. Instead, the European Union should pursue a strategic raw materials policy that reconciles the demands of both.

-

The two biggest challenges in sustainability governance are: firstly, the diversity of standards and their inconsistent implementation and enforcement; and secondly, power asymmetries and lack of transparency along metal supply chains.

-

A sustainable raw materials policy must seek to reduce dependency through strategic diversification and partnerships with countries that share European values. Transparency-enhancing measures and a regulatory “smart mix” will be decisive elements.

Table of contents

2 Starting Situation: Dynamics in Security of Supply

2.1 Growing demand and import-dependency

2.2 Geopolitical dynamics and strategic raw materials policy

2.3 Human rights and sustainability obligations

3 Metal Supply Chains: Characteristics, Governance, Key Actors

3.1 Material flow and characteristics

3.3 Vertical and horizontal governance

4 Standard-Setting: Regulatory Heterogeneity in the Sustainability Sphere

4.1 Private standards and certification systems in metal supply chains

4.2 Inadequate transparency and standard-setting in the international trading sector

4.3 First regulatory initiatives for the financial sector and investments

4.4 National regulation in the mining and processing sectors

5 Challenge: Implementing and Enforcing Sustainability Standards

5.1 Difficulties in the individual stages of the supply chain (horizontal dimension)

5.2 Difficulties in transnational supply chains (vertical dimension)

6 Comparing Metal Supply Chains: Platinum and Copper

6.2 Lead firms and state cooperation

6.3 Important counterweights: Civil society and trade unions

7 Seeking a Sustainable Raw Materials Diplomacy

7.1 Diversifying supply chains

7.2 Reducing dependency on China

7.3 Building and expanding strategic raw material alliances

7.4 Intensifying European and international cooperation

7.6 Promoting multi-stakeholder processes

Issues and Recommendations

European businesses depend heavily on imported metals as the bloc possesses very limited reserves of its own and recycling cannot satisfy demand. Given the pace of developments in green energy, electromobility and digitalisation, demand for metals is expected to increase significantly in coming years. The International Energy Agency (IEA) expects global demand for critical metals for green energy technologies to quadruple by 2040.

The discussion has been driven by rapid real-world developments. First the Covid-19 pandemic starkly exposed the structural risks associated with supply chains. Then the Russian invasion of Ukraine disrupted supplies of metals such as nickel, as well as food and energy. Making matters worse, great uncertainty has arisen over China – a central actor in the supply chains for many critical metals. We are currently observing growing geopolitical rivalry over access to metals.

These developments are playing out in parallel to growing pressure for companies to comply with corporate due diligence obligations and improve the sustainability of their business practices. A series of initiatives to minimise negative human rights and environmental impacts of corporate activity in global supply chains has been launched over the past ten years. While standards were initially private and voluntary, we now see a mix of voluntary standards and mandatory regulation. Multi-stakeholder initiatives play an important role, bringing together state actors, civil society organisations, the private sector and state-owned enterprises. Some EU member states committed to the path of binding regulation, for instance Germany with the passage of the Act on Corporate Due Diligence Obligations in Supply Chains in 2021. The member states of the European Union have also agreed to introduce a European Corporate Sustainability Due Diligence Directive.

Geopolitical challenges now threaten to undermine support for longstanding sustainability efforts. It would, however, be short-sighted to prioritise security of supply over human rights and sustainability. A succession of recent studies demonstrate that sustainability standards are in fact integral to security of supply, because they prompt corporate and state actors to think more strategically and act to preempt supply chains risks. On the other hand, the technical and geopolitical characteristics of metal supply chains limit the possibilities for European actors to influence sustainability. As customers they generally lack direct influence on the initial stages of production such as mining and refining.

The present study therefore explores the question of which governance approaches European actors can apply to improve sustainability in metal supply chains, and how they can influence other actors and the upstream stages of the supply chains to that end. The term “sustainability” is employed in the sense laid out in the United Nations Sustainable Development Goals.

The study is based on in-depth analyses of two metal supply chains: copper from the Andes and platinum from Southern Africa. It focuses on – and supplies policy recommendations for – the issue of supply chains in industrial mining.

The empirical material stems from more than 130 discussions and interviews with interlocutors from politics and administration, industry, civil society and academia, conducted in 2021 and 2022 as part of the research project on “Transnational Governance of Sustainable Commodity Supply Chains in the Andean Region and Southern Africa”, funded by the German Federal Ministry for Economic Cooperation and Development (BMZ). The centre of interest lay in the mining nations of Chile, Peru, South Africa and Zimbabwe, the trading centres of Switzerland and the United Kingdom, and the implications for Germany and other EU countries as major importers.

Comparing the two supply chains permitted us to conduct a systematic analysis and reach conclusions considering both metal-specific and contextual factors. We were able to identify two major challenges for governance of metal supply chains:

First, the multitude of voluntary and compulsory sustainability standards that have emerged over recent years is confusing and frequently also inadequately implemented and enforced. While some of the sustainability standards are certainly complementary, there are issues with competing systems, diverging priorities and contradictory definitions of sustainability. Inadequate sustainability governance especially in the financial sector and commodity hubs fosters opacity in metal supply chains and constrains the regulatory influence of downstream actors.

Second, power asymmetries grant specific actors great influence over sustainability governance. The research perspective must take into account that each metal follows a different path, and that the supply chains and the (networks of) actors involved in them are metal-specific. Within any supply chain a small number of firms and states can play a very important role in implementing sustainability by setting and enforcing standards. The ability of civil society organisations and trade unions to influence supply chain governance is much more limited.

Lack of transparency in metal supply chains hampers the identification of power asymmetries. “Chokepoints” – smelters/refiners and traders – make it hard to trace material flows and supplier relationships.

In order to advance the cause of sustainable and effective supply chain governance, the EU and its member states must take action to expand diversification. The goal must be to reduce excessive dependency on individual countries, especially China. That means fostering dependable partnerships with resource-rich countries that seek high sustainability standards. Such arrangements should take into consideration the partners’ needs and offer corresponding support. Sustainable supply chain governance should also work to improve transparency and reduce power asymmetries. This can be supported by targeted measures, such as promoting multi-stakeholder processes in order to achieve a “smart mix” of voluntary and mandatory governance instruments.

Starting Situation: Dynamics in Security of Supply

A secure supply of metals is a matter of central economic importance for the EU. Growing global demand for metals will exacerbate geopolitical rivalries in the coming years, while pressure increases to ensure sustainability in procurement. European businesses face a challenge here: Having little involvement in mining and initial processing, they generally lack influence over the initial stages of supply chains.

Growing demand and import-dependency

Industrial demand for metals in Europe is already considerable. In 2021 the EU imported metals, minerals and rubber worth €59.6 billion. These imports increased in total value by 6.7 percent between 2002 and 2021.1 The EU is almost self-sufficient in non-metallic minerals but remains a net importer of metals, with varying levels of dependency for individual metals and stages in the value chain. Demand within the EU will continue to grow because metals are central to green energy, e-mobility and digitalisation, and thus to implementing the European Green Deal.2

The International Energy Agency (IEA) calculates that consumption of minerals for green energy technologies must quadruple by 2040 if the Paris climate targets are to be met. The accelerated transition required to achieve global net zero by 2050 would require a six-fold increase by 2040.3 The International Renewable Energy Agency (IRENA) identifies five metals that will be especially crucial for limiting global warming to 1.5°C: copper, lithium, nickel, and two rare earths, neodymium and dysprosium.4 The EU began listing economically relevant raw materials subject to significant supply risks in 2011. The current – fourth – list of critical raw materials comprises thirty items.5

The idea of satisfying European demand for metals through domestic mining and recycling will remain unrealistic for the foreseeable future, even if the EU’s circular economy action plan (updated in 2020) and major investments under the EU Critical Raw Materials Act are rapidly implemented. That path, which is also highly relevant for achieving greater EU autonomy in the long term, would require enormous technological progress and a massive expansion of the circular economy, on a scale that cannot be accomplished in a short space of time.6

Germany – as the EU’s biggest economy – is especially dependent on metal imports, and has no meaningful domestic extractive industry of its own. Its reserves of strategic metals are meagre and the legislative and technological preconditions for extraction lacking. No other EU member state has any significant mining sector either. The same applies to processing operations such as refining.7

For certain metals European import dependency is 100 percent.

European manufacturers import most of their metals from other regions of the world; import-dependency for many lies between 75 and 100 percent.8 Many of the imported primary raw materials originate from countries in the Global South. Initial processing is often conducted there, before the material is transported to European countries for final processing (in many cases with an intermediate stage in China).

Geopolitical dynamics and strategic raw materials policy

Various geopolitical shocks have disrupted metal supply chains in recent years. The Covid-19 pandemic and associated shutdowns in various regions created global supply bottlenecks. The situation was exacerbated by an energy crisis in China, which in 2021 for example caused a global magnesium shortage that also affected German firms.9 Altogether there are growing concerns over China’s reliability as a key supplier of critical metals, for instance due to export restrictions in response to international frictions (as in the trade conflict with the United States), its ongoing domestic energy shortage, or other domestic or foreign policy-related reasons.10

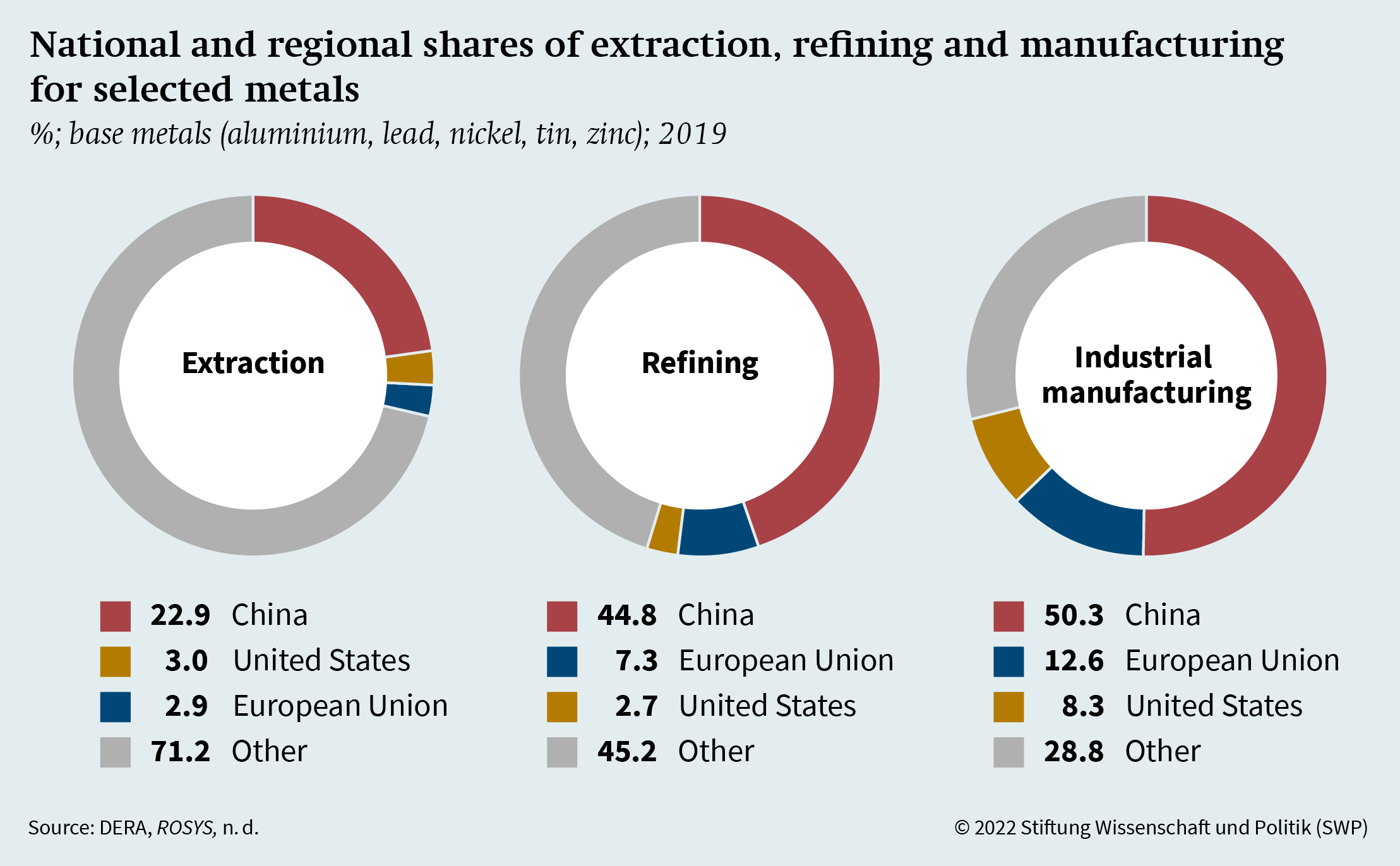

The Russian invasion of Ukraine has brought further shifts in the global markets, as Russia – an important exporter of metals such as nickel and palladium – became a political and economic risk. For instance, in 2020 German companies imported metals worth €2.8 billion from Russia.11 Since the beginning of the war many companies have ceased doing business with or in Russia, and imports of metal products have fallen considerably. However many metals (ordered before the sanctions) continued to be imported into the EU.12 At the same time political attention has turned to Europe’s enormous dependency on China for mineral raw materials (see info box “China’s dominance” and Figure 1, p. 10).13

European efforts to secure raw materials have been stepped up since the pandemic, in response to multiple emerging challenges. The German government for example adopted its first raw materials strategy in 2010. A revised version naming seventeen measures was presented in January 2020.14 In January 2023, in response to current geopolitical developments, the German Federal Ministry for Economic Affairs and Climate Action (BMWK) presented three pillars for a revised raw materials strategy: 1) circular economy, resource efficiency and recycling; 2) diversification, including monitoring and crisis management in critical supply chains, and increasing international and European cooperation, including the strengthening of mining and production capacities within and outside the EU; and 3) ensuring a fair and sustainable (international) market framework.15

|

China dominates the supply chains for many critical metals. Over recent decades it has massively expanded its domestic mining sector and opened up numerous reserves. In 2021 China was the largest producer of 42 percent of the mining products (industrial minerals, metals and coking coal) listed by the German Mineral Resources Agency (Deutsche Rohstoffagentur, DERA) as subject to high price and supply risks. For another almost 25 percent China was second or third. Furthermore, the Chinese government has committed to a “Going Global” strategy and expanded the influence of Chinese enterprises in various metal supply chains, in particular through its Belt and Road Initiative. The participation of Chinese enterprises in all stages of these supply chains has secured strategic advantages in the global competition for raw materials. As well as investing in domestic and foreign mining and transnational infrastructure, Beijing has prioritised promoting domestic smelting and refining. According to data from DERA, China accounted for 93 percent of refined products with a high supply risk in 2021. This global dependency also affects the wider group of high-risk trade products, which includes semi-finished products. Here China is the biggest net exporter with a 41 percent share of the global market. |

Such strategic dependencies are, as the Russian invasion of Ukraine demonstrates, associated with great risks. They weaken European economic sovereignty. China’s preeminence – in mining and processing of metal ores, in manufacturing, and as an international commodity trading centre – represents a risk that businesses must address – with political backing. a DERA, DERA-Rohstoffliste 2021, DERA Rohstoff-Informationen 49 (Berlin, 2021), 5, https://www.deutsche-rohstoffagentur.de/ DE/Gemeinsames/Produkte/Downloads/DERA_Rohstoffinforma tionen/rohstoffinformationen-49.pdf?__blob=publicationFile (accessed 8 February 2022). b Schüler-Zhou et al., Einblicke in die chinesische Rohstoffwirtschaft (see note 10), 8. c Ibid., 52–56. d Ibid. e DERA, DERA-Rohstoffliste 2021 (see a). f Jane Nakano, The Geopolitics of Critical Mineral Supply Chains: A Report of the CSIS Energy Security and Climate Change Program (Washington, D.C.: Center for Strategic and International Studies [CSIS], March 2021), https://csis-website-prod.s3. amazonaws.com/s3fs-public/publication/210311_Nakano_ Critical_Minerals.pdf. |

|

Similar initiatives are also under discussion in other European countries – first and foremost France16 – and at the EU level. The German and French governments have already presented joint proposals for a European Critical Raw Materials Act.17 The European Commission intends to publish a first legislative draft in spring 2023.18

The Critical Raw Materials Act is part of the EU’s newly unveiled Green Deal Industrial Plan, in which the EU Commission has set itself the goal of strengthening its strategic autonomy, by reducing its dependencies in strategic sectors. In January 2023, Commission President Ursula von der Leyen further strengthened this approach, by announcing a Sovereignty Fund to boost investment in European industries of strategic interest.19

|

|

|

Source: Deutsche Rohstoffagentur (DERA), ROSYS – Rohstoffinformationssystem, https://rosys.dera.bgr.de (accessed 22 August 2022). |

The US government has also since 2020 intensified its measures to increase resilience and diversify mineral supply chains.20 Considering critical minerals as economic as well as national security concerns, the Defence Production Act (DPA, June 2022) gives the President authority to use economic incentives to boost supplies of critical minerals. The Inflation Reduction Act (IRA) of September 2022 provides for such investments and grants tax credits under certain conditions (for example where raw materials for production are sourced in the United States or from countries with which the United States has free trade agreements). These provisions are viewed critically in the EU. Yet the Biden administration is proactively fostering international cooperation in the minerals sector. In June 2022 the latter launched an international initiative called the Minerals Security Partnership (MSP). Together with major mineral-exporting and industrial economies (including the EU), the MSP seeks to enhance security of supply for crucial metals required for the “clean energy transition”.21 The initiative’s members have recently identified concrete projects that will be promoted along mineral supply chains (all stages, including circular economy).

All these strategic initiatives formulate strict sustainability requirements for the mining and processing of mineral raw materials. As such they build on diverse initiatives for creating sustainable supply chains that have been set in motion in recent years.

![]() Human rights and sustainability obligations

Human rights and sustainability obligations

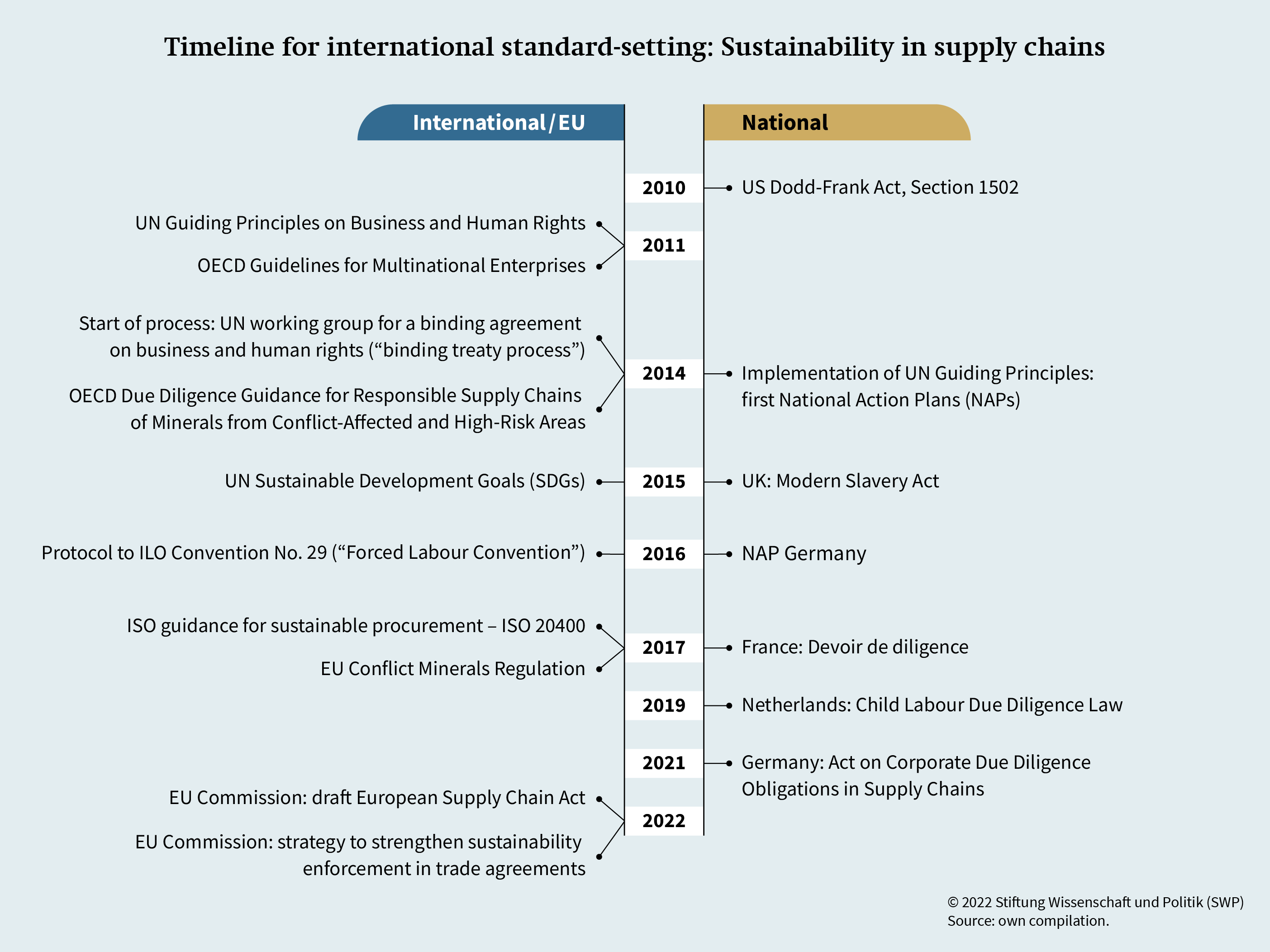

A string of initiatives at the international level have emerged since publication of the United Nations Guiding Principles on Business and Human Rights in 2011. The OECD Guidelines for Multinational Enterprises and the norms of the International Labour Organisation (ILO) and the International Organisation for Standardisation (ISO) are all now broadly recognised (see Figure 2).

Moves to define sustainability standards have also emerged during the past decade at the EU level and in individual member states. Legislation to impose corporate due diligence obligations is planned or has already been enacted, encompassing general measures as well as initiatives specifically for mineral supply chains.22 In 2017 the European Union adopted its first legislation requiring corporate due diligence in metal supply chains; this was the Conflict Minerals Regulation for gold, tin, tantalum and tungsten.23

In March 2022 the EU Commission presented the Corporate Sustainability Due Diligence Directive (CSDDD), which will apply to minerals sector as a whole. In comparison to the German LkSG, the CSDDD draft covers the entire value chain, expansion of environmental and climate-related due diligence obligations, and corporate civil liability.24 On the basis of this draft, so-called trilogue negotiations between the Commission, the Parliament and the Council are currently taking place. A final draft law is expected by next year. Germany and France have already adopted cross-sector supply chain due diligence laws. The German Act on Corporate Due Diligence Obligations in Supply Chains came into force in 2023 and the French Duty of Vigilance Law in 2018. Similar legislative proposals are currently being discussed in other EU member states, such as Italy, Denmark and Sweden.25

The German government has been very active, acknowledging its international obligations under the Sustainable Development Goals (SDGs). Germany has also accepted the UN Guiding Principles and in 2016 adopted its first National Action Plan for Business and Human Rights (NAP). An update to the NAP is currently in preparation.

Metal Supply Chains: Characteristics, Governance, Key Actors

Metal supply chains are complex and structurally diverse. Many of the actors remain out of sight. That, combined with the lack of traceability, makes it hard to enforce due diligence on human rights and environmental concerns. Yet ensuring sustainability is particularly important in metal supply chains, which pose great environmental and human rights risks, above all in mining and processing (see pp. 14ff.).

Material flow and characteristics

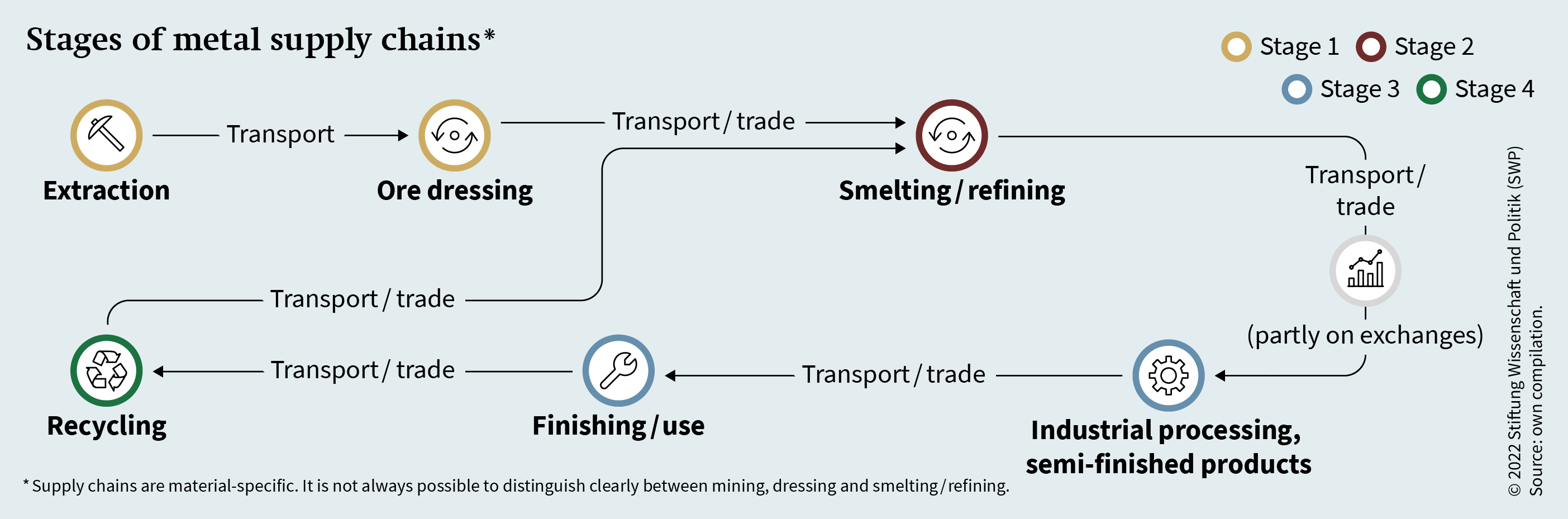

Metal supply chains can be broadly divided into four stages (see Figure 3, p. 14). The beginning of the process – here the first two stages – is described as upstream, the later stages as downstream.

After successful geological prospecting and project development the first stage is mining (deep or open-cast). In industrial mining this stage is capital- and technology-intensive. The less formal extraction methods employed in artisanal mining lie outside the scope of the present study.26 The next step is to process ore into concentrate. This is normally done in ore-dressing plants close to the mines.

The second stage is smelting and refining, to extract the metal itself from the concentrate. Depending on geological and geographical factors, this may occur close to the mine or further away.

The third stage is industrial processing, where the refined metal is turned into semi-finished products such as sheet, wire and tube for use in manufacturing. The final products range from simple jewellery to extremely complex machines and electronic devices.

The fourth stage is recycling, where scrap metal is reintroduced to the cycle. The recycling stage is not the focus of the present study.

Most metal supply chains follow this scheme, but each has its own specific characteristics. These have as much influence on the supply situation as the sustainability governance. The specific structure is heavily influenced by material factors such as the distribution of geological deposits, the type of metal and its uses.

The number of processing steps in the supply chain is a relevant characteristic. Industrial metals, including copper and platinum, end up in an enormous range of products. This creates greater complexity than a case such as gold, for example, which is used principally in jewellery and as a store of value. The more industrial processes and the broader the spectrum of final applications, the more complex the supply chain will be – and the more difficult it will be to track the materials.

The longer and more complex the supply chain, the more difficult it is to track the materials.

As a result, secondly, supply chains are of different lengths. Raw material supply chains almost always span multiple countries, and often several continents. This increases the risk of non-compliance with sustainability standards, and may threaten security of supply.

A third characteristic is the concentration of production steps at specific locations. As well as the number of countries involved, the number of companies must also be considered.27 The greater the concentration at a particular stage the smaller the possibility for importers to switch to other countries or companies and the greater the dependency. At the same time, a high degree of concentration is conducive to traceability.28

Ultimately, the more complex a supply chain and the dynamics within it, the harder it will be to realise specific sustainability measures. If individual actors choose to block sustainability governance, risks can arise even in shorter and less complex supply chains.

Sustainability risks

The biggest sustainability risks in metal supply chains arise during the first stage, in connection with mining.

Environmental degradation can affect both the immediate vicinity of the mine and the broader region.29 Mining activities represent a major intervention in flora, fauna and habitat. Moving large masses of earth and rock (especially in open cast mining) has repercussions for diversity and landscape structure. Further environmental risks include air pollution through emissions, dust and blasting, and acidic mine drainage.30 Mining also consumes a great deal of water. For example 350 m3 of water is required to mine and dress one tonne of copper.31 Mining and dressing are also extremely energy-intensive. The management of overburden and tailings and the (lack of) rehabilitation of abandoned mines represent another sustainability problem, especially when mining wastes are not properly disposed of.32

Mining in populated areas also has direct social impacts, and is associated with risks to observance of human rights (for example the right to health and clean water). Adverse impacts on the livelihoods of local communities is by no means unusual. For example conflicts and violence may arise where resource extraction is permitted on land previously used for settlements or agriculture. Disputes over land use and questions of fair compensation are a perennial issue in mining regions, for example in South Africa.33 The lack of local value creation at the local and national levels is another bone of contention. The same applies to the distribution of costs and benefits between mining companies and workers, local communities and the state.

The lack of effective complaint mechanisms for communities affected by mining creates further potential for conflict, as does inadequate implementation of corporate “social and labour plans”, for example in connection with provision of local infrastructure and workers’ housing.34 The NGO Global Witness has documented more than 145 conflicts associated with mining and processing since 2012, including the deaths of more than 280 activists; the number of unreported cases is assumed to be even higher.35 Industrial mining (especially underground) poses great challenges for workplace health and safety. Important rights such as freedom of assembly or the right to join a trade union are restricted in certain countries.36 In many, women in the mining sector experience sexualised or sexual violence.37 According to the ILO women account for just 10 percent of mineworkers and gender-specific workplace discrimination is rife.38

While the risks associated with extraction are well-researched and the issues receive considerable attention at the political level, the same cannot be said of sustainability risks in the second stage (smelting/refining) and in transport. If labour and environmental standards are neglected, workers and surrounding communities will suffer. The metallurgical complex at La Oroya in Peru is alleged to have polluted the ground and water with heavy metals for decades until it was closed in 2009. A case concerning the grave health consequences was filed by the Inter-American Commission on Human Rights (IACHR) in October 2021.39

The industrial processes used to produce metals are energy-intensive, with environmental and climate consequences. The enormous amounts of energy required to smelt and refine platinum and copper, for example, still originate predominantly from fossil fuels.40 According to estimates by the United Nations Environment Programme (UNEP), mining and processing of metals accounted for approximately 18 percent of resource-related climate change in 2011.41

Bulk transport by land and sea, as in the case of copper, is also associated with large CO2 emissions.42 Lack of transparency about working conditions in the transport sector creates additional risks.43

China’s role in metal supply chains must be considered from the human rights and sustainability perspective.

If sustainability is to be achieved in metal supply chains, the central role of China will need to be considered from the human rights and sustainability perspective. There have been a succession of revelations concerning inadequate human rights and labour standards in Chinese workplaces. A statement by the UN High Commissioner for Human Rights recently laid out grave human rights abuses experienced by the Uighurs for example.44 Restrictive legislation and tight constraints on free speech and the press make it impossible for external observers – including academic researchers – to ascertain what is really happening in and around China’s mines, how metal-processing firms are operating, and to what extent they are implicated in violations.45 Nevertheless, there have been a string of revelations of human rights violations in Chinese production facilities, including those used by European companies.46

Vertical and horizontal governance

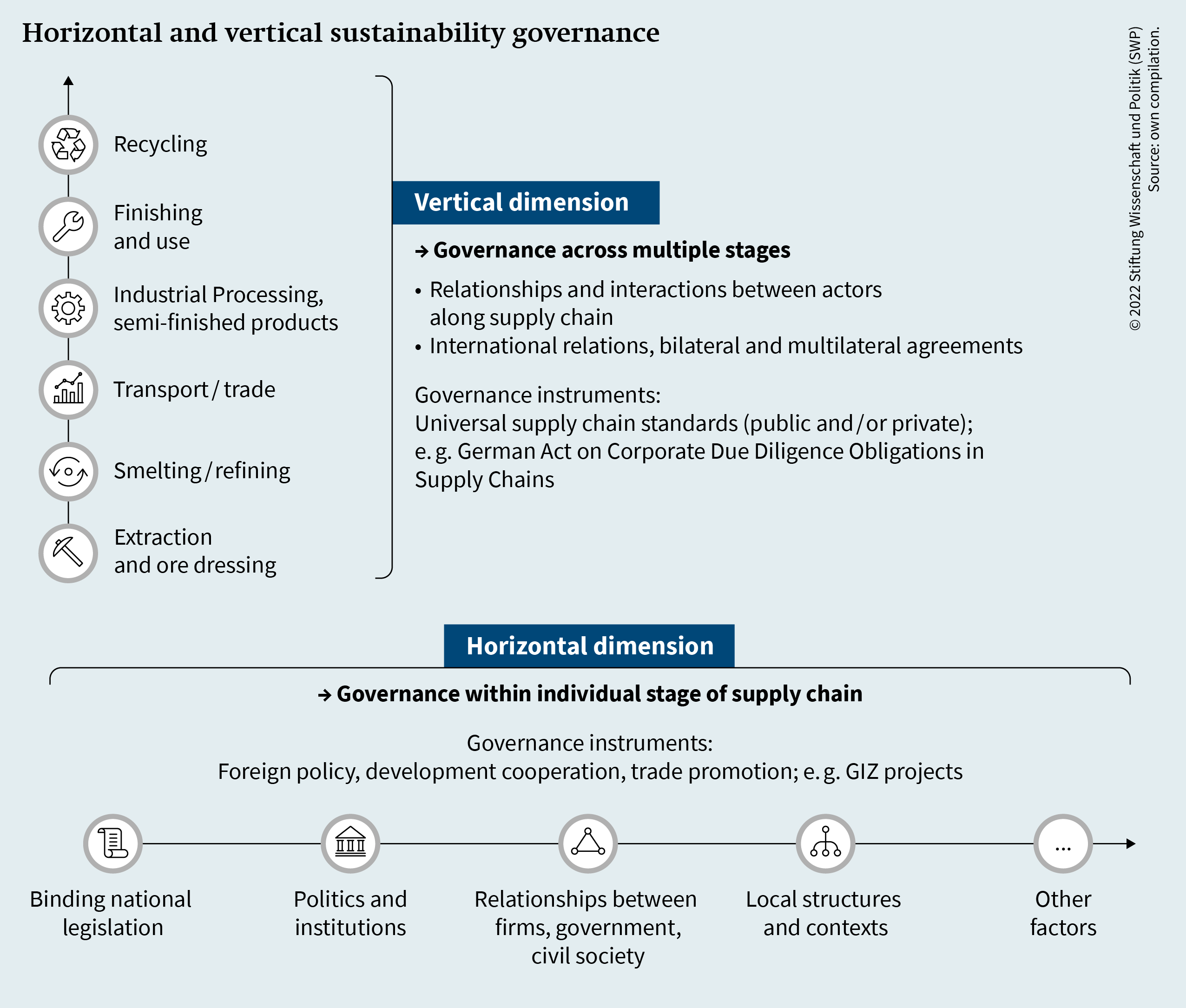

In the great majority of cases, the participation of European firms in metal supply chains begins with industrial manufacturing (stage 3). This begs the question which instruments are available to influence the first two stages. The concept of supply chain governance is understood as the entirety of the co-existing forms of collective regulation, including binding legislation, voluntary standards, norms, initiatives and institutions.47 This understanding of governance extends beyond binding legislation and includes further possibilities at various stages, in both the vertical and horizontal dimensions (see Figure 4).

The vertical dimension comprises the transnational flow of materials through the various stages of the supply chain. The analytical focus here is on the actors and standards that connect the various stages. The starting points for sustainability governance on the vertical plane are national instruments that apply throughout the supply chain (in other words with extraterritorial effect). These include the German Act on Corporate Due Diligence Obligations in Supply Chains and the EU Conflict Minerals Regulation, as well as their supporting measures. Private standards may also influence actors’ behaviour at multiple stages. The “Copper Mark”, for example, is a certification system covering the entire copper supply chain.

The horizontal dimension focuses on the individual stages and geographical locations, where power constellations, actors’ interests, local governance structures and political factors all play salient roles. Openings for the EU and its member states include foreign policy and development cooperation instruments as well as trade promotion.

There are also instances where horizontal and vertical sustainability governance instruments overlap, for example where the same actors interact on both levels, where the same standards are applied along the entire supply chain, and also through international standards such as the UN Guiding Principles.

Central actors

Various actors and networks influence supply chain sustainability governance, in the sense of developing and implementing standards.48 The following six groups of actors can be distinguished.

Firstly the United Nations and other international organisations, which are increasingly involved in setting standards for sustainable supply chains; secondly states where one or more stages of a supply chain are located. A third group is businesses operating at the national or transnational level, in particular (private-sector or state-owned) mining enterprises, transnational traders and exchanges, and the financial sector. The certifying agencies and initiatives that develop and/or audit standards form the fourth group; workers in or affected by mining and processing, local communities and their civil society representatives the fifth. Sixth and last is the (intermediate and final) consumers. The relative influence of these actors and groups varies considerably.

Businesses and states are without doubt the most important actors in supply chains. The former organise the material flow and exert decisive influence over the organisation. They can also (co-)determine the forms and scope of sustainability management through their own standards and initiatives (for example for reducing CO2 emissions). States create the legislative and regulatory framework for mining, processing and trading within their sphere of influence and define concrete terms for companies operating within supply chains. The companies (lead firms) and countries that occupy key positions in the supply chain are especially influential. For example, control of very large mining and/or refining capacity for a critical metal implies great potential influence on sustainability governance in the individual stages of the supply chain. The centrality of key actors enables them to promote sustainability along the entire supply chain (see pp. 32ff.). That makes them important partners for European actors seeking to improve sustainability in upstream stages.

Certain central actors function as chokepoints for transparency (see info box “Chokepoints”, p. 27) and/or as links between different stages and geographical locations. As such they are decisive for the implementation of sustainability instruments throughout entire supply chains. The first chokepoint is the smelters and refiners. They frequently process ores from different mines and can therefore actively promote – or hinder – transparency by revealing their sources and suppliers.49 This second stage is generally very opaque, partly because of inadequate standard-setting, but also because the second stage for many critical metals occurs in China. Another chokepoint is the commodity traders and metal exchanges, which pass information from the upstream supply chain to downstream actors. Traders and metal exchanges also have possibilities to set their own sustainability standards, but have to date made very little use of these.50

Greater attention needs to be paid to the role of transport as an important link in supply chains. The movement of raw materials and products within countries and across borders is associated with significant environmental impacts and human rights risks, as well as numerous dangers of disruption. Financial actors represent another link. Their role in enabling material flows and projects in capital-intensive raw material supply chains gives them the opportunity to enforce requirements.51 Here again, much of the potential for implementing sustainability standards remains untapped.

Standard-Setting: Regulatory Heterogeneity in the Sustainability Sphere

Sustainability governance in raw material supply chains involves voluntary and mandatory instruments and regulations, established and implemented by private and state actors.52

Private standards and certification systems in metal supply chains

Many of the firms involved in metal supply chains have instituted internal systems to guard against sustainability risks and fulfil their corporate responsibilities, employing external certification systems as well as internal controls. This applies to the major mining and refining companies in the upstream supply chain as well as the buyers of raw metal and semi-finished products in the downstream supply chain. This development is an outcome of growing public pressure, but also reflects tightening legal requirements (see pp. 11f.).

The quality of sustainability reporting often fails to meet stakeholder expectations.

Communicating sustainability goals and strategies to investors and the public is a routine aspect of business today. Downstream actors, such as European automobile manufacturers, originally tended to concentrate their sustainable supply chain management and standards more on social aspects of mining such as human rights violations than on negative environmental externalities.53 In the meantime climate issues, for example quantifying and publishing CO2 emissions, have become a major topic along mineral supply chains,54 partly overshadowing other aspects, which are also more difficult to monitor and quantify.

Many companies in mining and in the upstream supply chain continue to pursue a strongly compliance-driven approach, driven by external requirements.55 Much more comprehensive (risk) analyses are needed, covering the gamut of environmental, human rights and governance risks. But corporate strategies should not focus exclusively on risks. Long-term development potentials need to be identified and the necessary cooperation with suppliers and local actors strengthened, in order to initiate permanent, sustainable improvements in metal supply chains.56 The quality of ESG-related reporting in the mining and metals sector generally remains poor, for example by not setting specific performance targets and reporting accumulated rather than mine-level data.57

Buyers of raw metals and semi-finished products apply various internal measures to enforce standards on partners further up the supply chain. For example many employ contracts requiring their suppliers to observe environmental standards and human rights and to conduct (or arrange for) risk analyses and audits, or use questionnaires to gather sustainability-related information. Large companies in particular often work closely with their suppliers in the scope of corporate social responsibility activities and capacity-building.58

Upstream businesses (in the first and second stages) sense the pressure to respond to growing sustainability requirements. In adopting internal measures and communicating these externally, they orientate clearly on the demands of their respective parent companies and customers.59 Local and international industry organisations like the International Council on Mining and Metals (ICMM) also exert great influence on standard-setting in mining.

On the other hand, firms along the supply chain are also making increasing use of external private standard and certification systems to achieve their own sustainability goals and/or to satisfy external requirements. A series of problem-specific and sector-specific private standards have become established in metal supply chains, with widely differing target groups, levels of obligation, scope and reach. Most of these are voluntary initiatives, with different requirements for corporate reporting, verification (auditing) and traceability.60 The diversity of voluntary standards is confusing and makes it difficult for businesses to select and implement the one that suits them best (see pp. 26f.).

The establishment of private-sector standards and certificates is a fundamentally welcome development. Three aspects need to be considered, however.

Firstly, many relevant private-sector standards and certificates are heavily shaped by industry actors and thus reflect particular interests. As a consequence, these actors often find their legitimacy questioned by local communities and civil society.61 In that context, multi-stakeholder initiatives like the Initiative for Responsible Mining Assurance (IRMA) represent a relevant corrective.

Secondly, most private standards lack consistent guidelines concerning implementation and publication. Standards run by industry actors like the ICMM place great weight on agenda-setting and negotiating corporate guidelines and less on enforcement and monitoring.62

Thirdly, few of the available private standards and certificates cover the entire supply chain. And where they do they are rarely material-specific. As a result they fail to cover (material-) specific production conditions and contexts and thus lack regulatory depth. Furthermore, very few of the existing standards include industrial processing (stage 3), while insufficient attention is likewise paid to risk-associated activities like transport.63 Certification (or more thorough certification) of the entire supply chain would be a major undertaking. But it would offer a welcome opportunity to address the problem of transparency (see pp. 27f.) in transnational supply chains.

Inadequate transparency and standard-setting in the international trading sector

In contrast to mining and processing, regulation efforts tend to pay a great deal less attention to the metal traders and exchanges, which often represent an important chokepoint, and the financial sector. In fact it would be vital to include them if one wishes to improve transparency and realise universal standards, as the EU CSDDD sets out to do.

The structure of the commodity trade is not conducive to introducing systematic sustainability standards.

Implementing sustainability standards in the commodity trading sector is especially challenging. Trading operations tend to be material-specific, the actors dispersed and hard to pin down. Within Europe Switzerland and the United Kingdom (London) are the decisive trading hubs; neither is an EU member. To date both countries lack corresponding legislation and the corporate sustainability initiatives of traders and exchanges are largely voluntary.

Switzerland is one of the world’s largest trading centres for metals and home to major transnational commodity traders, such as Trafigura and Glencore. Various trading instruments, including prefinancing of production, enable these enterprises to influence producing countries and shape prices and availability.64 In recent years Switzerland has initiated a number of processes to improve transparency and tighten corporate responsibility. It is an active member of international bodies like the OECD and the Extractive Industries Transparency Initiative (EITI), the latter focussing on good governance and transparency in the raw materials sector. Switzerland has also issued guidelines for implementation of the UN Guiding Principles, aimed at trading houses.65 Finally, the Swiss Code of Obligations was amended in January 2021. It now requires resource-extracting enterprises to disclose all (aggregate) payments of 100,000 Swiss francs (approx. €102,000) or more made to government authorities. But overall the legal obligations placed on businesses remain weak. The referendum for the Responsible Business Initiative, which proposed a Swiss equivalent of the German supply chain legislation, failed at the end of 2020.66

The United Kingdom is regarded as Europe’s commodity hub on account of the London Metal Exchange (LME), which conducts a significant proportion of the world’s metal trade. Not until 2019 did the LME publish sustainability guidance orientated on the OECD Guidelines. It will be obligatory for all market participants from 2023, with failure to comply potentially leading to exclusion from trading activities. The LMEpassport introduced in 2021 allows producers to provide information about the sustainability of their products, albeit on a voluntary basis.67 The main criticisms of the LME are that the instruments are not necessarily binding, violations are not consistently followed up, and complaints from supply chain actors are not published.68

There are also a number of over-the-counter trading centres, such as the London Platinum and Palladium Market (LPPM). The LPPM introduced obligatory Responsible Sourcing Guidance for all refiners in 2020. Although its scope could be broader, it is nevertheless an important step forward as it is based on verification by independent actors (third-party audits). In spring 2022, for example, LPPM was able to use this mechanism to rapidly exclude Russian refiners.69

The leading producers and traders are increasingly working to establish ESG standards in their business practices.70 This trend is driven both by growing customer expectations and by sometimes massive pressure from NGOs.71 Nevertheless, the EU’s power to regulate transnational supply chains and the associated traders remains indirect in nature. The many smaller traders, which are often based in Switzerland, continue to be completely overlooked. They focus largely on purchasing as cheaply as possible on digital platforms and are currently affected only indirectly by supply chain laws.72

First regulatory initiatives for the financial sector and investments

Legislators are only just starting to turn their attention to the financial sector and supply chain–related investments, despite their enormous influence on sustainability standards. For example half of all mining projects are funded by foreign investors.73 Private-sector – and to an extent also public – banks play a special role via their lending and investment guarantees. Financial actors are thus a vital factor for enabling major mining-related investments and for the activities of transnational traders.74

Changes in financing are beginning to be seen, initially in the area of environment and climate. New initiatives are emerging, such as the Task Force on Climate-Related Financial Disclosures (TCFD).75 Private-sector financial actors increasingly stipulate ESG terms in their lending and investment contracts, seeing this as a way of minimising the risk to their investments.

Similar developments are also observed in the public finance sector and its guarantee schemes. For example, investments by the Global Gateway Fund (GGF), which aims to support the EU’s Global Gateway strategy, need to follow the social and environmental standards of the European Investment Bank (EIB).76 In Germany the criteria for loans from the state-owned investment and development bank KfW and Untied Loan Guarantees (Ungebundene Finanzkredite, UFK-Garantien) are currently under review. The International Finance Corporation (IFC), the World Bank and other multilateral development banks have also laid out criteria that projects must fulfil if they are to receive funding.

While the mostly ESG-related criteria in these private and public financing schemes are of utmost importance, far-reaching challenges exist in terms of ESG-related data collection, comparability and monitoring as well as in transparency and disclosure.77 This is particularly relevant in connection with investments in high-risk sectors, such as the minerals sector. However, we also observe the introduction of stricter standards for the financial sector and other investments, driven by growing investor demand and by legislation.78 According to the Commission’s draft, the EU Corporate Sustainability Due Diligence Directive should also include the financial sector,79 although certain member states oppose this and the matter is not settled.80

National regulation in the mining and processing sectors

In the horizontal dimension initiatives for binding regulation of due diligence in supply chains – like the German Act on Corporate Due Diligence Obligations in Supply Chains or private standards and certificates – encounter local governance structures. Here it is crucial to have (or establish) a binding legal framework for labour and social rights and environmental standards in mining and processing countries (stages 1 and 2).

Certain countries in which metal ores are mined have established extensive legislation to regulate the mining and processing sectors. They often build on international frameworks, such as the ILO norms or the Universal Declaration of Human Rights. While South Africa has set high standards for environmental and social rights (also specifically for the mining sector), regulatory loopholes and legal uncertainties still remain for example in relation to land rights. As an OECD member Chile is already committed to that organisation’s guidelines. But it has gone further, passing numerous laws laying the groundwork for the implementation of sustainability and corporate due diligence. In both countries, however, the central challenge of sustainability governance lies in implementation (see pp. 25ff.).

The participatory rights of mining communities and civil society form a flashpoint in both these countries. In South Africa there has been criticism that participatory rights relating to licencing of mining projects are not adequately anchored in the legislation. Nor is there any provision for state agencies to deal with complaints or offer mediation.81 Certain Latin American countries such as Peru, have established state ombudsman’s offices to protect the rights of affected communities and mediate in the event of conflict. Here again the problem lies more in the implementation: the institutions are often regarded as biased or lack of sanctioning mechanisms constrains their effectiveness.82

In countries with weak governance and/or authoritarian structures it is especially hard to enforce sustainability standards.

Countries with weak governance and/or authoritarian structures present particular challenges for sustainability standard-setting. A business operating in such a setting that wishes to observe international standards must do so on its own initiative, and due diligence may be harder to realise. One good example is Zimbabwe, whose mining legislation is outdated and in great need of reform. There is a particular deficit concerning sustainability standards. Here the legislative processes have been bogged down for years.83 Authoritarian structures that restrict the rights of civil society and trade unions also make it harder to realise a sustainability agenda (see pp. 35f.).84

The absence of political strategies for expanding local value creation in mining regions is another controversial issue in many countries. Highly automated industrial mining offers only a very limited number of jobs directly. The lack of employment and training opportunities and the limited involvement of local companies in upstream industries often leads to local conflicts and blockades. This is closely associated with questions of transparency in the raw materials sector and profit distribution. Chile, South Africa and Zimbabwe are not members of EITI. Peru was recently suspended for failure to meet a reporting deadline.85

At this juncture it is instructive to consider China, which is increasingly setting its own standards for mining and processing, above all in the environmenttal and climate spheres. The Chinese government introduced environmental regulations more than a decade ago, including strict reporting obligations for enterprises. China is also pursuing specific strategies to promote “green mining” at home. But its labour and social standards – and not least complaint mechanisms – still lag far behind the international field.86 Multiple states and parliaments have sharply condemned grave human rights violations in China, up to and including crimes against humanity. In June 2022 the European Parliament reiterated its call for the Chinese authorities to allow independent monitoring and reporting, and appealed for European and UN engagement regarding the human rights situation in Xinjiang.87 Shortly thereafter the European Commission presented a legislative proposal on forced labour that would impose import restrictions on products made using forced labour.88

Challenge: Implementing and Enforcing Sustainability Standards

Increasing the number of standards does not automatically minimise the social and environmental risks associated with metal supply chains. The reason for this lies principally in the difficulties in implementation and enforcement. Firstly, certain producing countries have not set standards, or fail to implement those they do have. Secondly, not all businesses in the supply chain demand that their trading partners observe particular standards or hold particular certifications. Thirdly, opacity in the supply chain leaves certain businesses unable to identify their suppliers; this is the case for many EU buyers. Fourthly, actors in the downstream supply chain face the challenge of working concretely to implement and enforce sustainability standards in upstream stages, and in particular of verifying whether this has occurred.

Difficulties in the individual stages of the supply chain (horizontal dimension)

Governance deficits at individual production stages and thus at the national level affect the enforcement of sustainability standards. From the downstream perspective (where EU actors are often located) these gaps are difficult to identify and comprehend, because they result from complex political, social and economic circumstances.

Such deficits are found above all in regions with weak statehood,89 where the risk of negative environmental and social repercussions is especially high. The problem affects many mining areas, but transport and processing are by no means excepted (see pp. 14ff.).

Governance deficits hinder implementation of sustainability standards.

In the mining regions investigated for this study it is often a lack of monitoring and enforcement of statutory requirements that prevents effective sustainability governance, even where high standards are set. Scarcity of funding, personnel and know-how is a problem within the national ministries – and even more so at the regional and local level. There is often a shortage of qualified administrators. Training opportunities are limited and qualified staff are often attracted away by better pay and conditions in the private sector. Deficits in digitalisation and organisational administration only exacerbate the problems.90 One effect is that fines are seldom enforced and prosecutions are rare.

Inadequate implementation capacity is frequently an issue in the sphere of environmental standards. In Peru for example a lack of control instances makes it hard for the authorities to police environmental standards in remote Andean mining regions, or to verify whether hazardous wastes are properly disposed of.91 In South Africa, too, state mine inspections can be unreliable, and the same applies to the monitoring of private-sector rehabilitation of abandoned mines. Both of these issues create local problems on the ground.92

There may also be conflicts of interest and competence. In South Africa for example the relationships between the national departments involved in regulating the mining sector are characterised by power imbalances and lack of cooperation.93 Questions of representation also affect implementation. To cite the South African example again: The role of traditional authorities is codified in law at the national level, but is interpreted inconsistently in practice and contested by parts of the local population. Conflicts between the national and local levels are also found in many mining regions. In Peru regional and local mining regulations sometimes contradict national rules or hinder their enforcement. Finally, corruption, whether in state institutions, affected communities or involved businesses, also impairs the state’s ability to enforce standards.

Widespread difficulties in enforcing legal and private sustainability standards are also observed among businesses in the respective stages of production. In some cases the guidelines of the often transnational mining and processing firms are implemented poorly or not at all at the local level. The reasons for this include inadequate communication, monitoring and training in the area of sustainability, as well as diverging goals between the levels of vertically integrated firms.94

Conflicts of competence also arise between company divisions and with suppliers. Examples are found in the relationships between large mining firms and their outsourced units, as well as with their local suppliers, such as transport firms and energy providers. In South Africa working conditions at sub-contractors are often a good deal worse than for those employed directly by the mining firms.95 In Peru mining companies only accept partial responsibility for their service providers.96 The question of responsibility can lead to prolonged legal conflicts. Some operators with low human rights and sustainability standards exploit legal uncertainty as a deliberate strategy to avoid responsibility.

Problematic conflicts of competence arise when firms take on tasks that are actually the responsibility of the state.

Conflicts of competence are also problematic when firms take on tasks that are actually the responsibility of the state but which the latter does not (or cannot) fulfil, such as the provision of infrastructure for basic public services. The voluntary or statutory engagement of the private sector in regional development, sometimes through public-private partnerships (PPPs), is fundamentally welcome. However, excessive expectations and confusion over responsibility offer potential for conflict especially with the local population. One problem is that if the commitment is voluntary the community lacks leverage to insist on fulfilment. South Africa’s statutory social and labour plans, in which companies commit to local development measures, are frequently orientated on local development plans. But their implementation is often inadequate, partly because the state invests too little in basic infrastructure.97

Difficulties in transnational supply chains (vertical dimension)

Implementing and enforcing sustainability standards throughout metal supply chains – across multiple stages – is problematic in the current configuration. It is crucial to create transparency throughout transnational supply chains (see info box “Chokepoints”, p. 27). If they are to fulfil their due diligence, buyers need to be able to verify the conditions under which the product has been produced, processed and transported.

Various instruments are available to European buyers wishing to ascertain the conditions under which their supplies were produced. Many employ internal instruments to fulfil their corporate due diligence by communicating directly with their suppliers, or participate in external initiatives (such as sector dialogues on implementing human rights due diligence). Or they can require their producers and suppliers to apply private standards and certificates, or recognise those the former are already using. These possibilities allow businesses to demand certain standards and monitor their observance (see pp. 19f.).

|

Chokepoints hinder transparency and traceability European companies are generally located in the downstream stage of metal supply chains (industrial manufacturing). If their supply chains are insufficiently transparent they will have difficulty ascertaining where the ores originate from, where the materials flow, what conditions are associated with the earlier stages of the process, and whether standards are observed. This poses great difficulties for sustainability management in the vertical dimension. Two characteristic chokepoints in metal supply chains restrict the traceability of the material and the identification of suppliers. The first is the smelters and refiners. If the companies involved fail to disclose the origin of the primary material and the conditions of its production, it is impossible for downstream actors to trace material back to specific mines (see pp. 29). The second chokepoint is the international commodity trade, which is largely decentralised and typically opaque. Long-term supply contracts between mining companies and smelters/refiners are common (and sometimes the same company operates in both stages). There are also – rather less frequently – direct supply contracts between firms operating in the second and third stages of a supply chain. On the other hand, most of the global trading of refined metals is conducted through specialised trading houses and metal exchanges. Here again, transparency concerning suppliers and provenance remains inadequate (see pp. 21f.). Information on refiners (especially those that are certified) is sometimes available through traders. But trading firms frequently supply no information on provenance. That is a problem, given that conditions vary from mine to mine within a country. |

If this is to succeed, industrial buyers in the EU must consciously strategise longer-term communication and cooperation with suppliers involved in mining and processing, where this is possible and viable. This challenging task demands determination and capacity.

On the other hand, companies along the entire supply chain need to address multiple challenges associated with the implementation of sustainability standards. The first difficulty lies in the heterogeneity of standards. Buyers have to choose a standard or certificate on the basis of what they can plausibly demand of their suppliers. It gets even trickier where buyers diversify their sources, because the selected standard has to be viable in different regional contexts. Firms in the upstream supply chain, for their part, find themselves dealing with multiple international customers each preferring different private standards and certificates (and often imposing stricter requirements than the local legislation).98

We are already seeing a decline in the number of private standards, however, with particular standards becoming more widely established.99 Developers of standards and certificates also confirm that harmonisation efforts are under way in certain areas. Companies all along the supply chains regard harmonisation and mutual recognition processes as central to enhancing clarity and transparency.

Cost is another problem. Companies in the downstream supply chain have to continuously monitor the scope and quality of the information provided to them by their suppliers – either directly or by third parties in the case of external audits. That is generally manageable for large, well-resourced companies, but not always for small and medium-sized enterprises (SMEs).

Additional cost and effort is also an important consideration in the upstream supply chain, where producers are required to report to their buyers and sometimes to pay large sums for certificates and audits. In the case of industrial metals like platinum and copper there is currently no price premium for certified material. This makes it difficult for producers of raw materials and precursors to pass costs on to their customers and reduces the incentives to seek certification, especially for small-scale mining companies.100 The latter therefore wish for more support from their buyers.

Unreliable audits the risk of greenwashing.

The third major difficulty concerns verification in production facilities in the upstream supply chain, irrespective of whether such audits are integral to transparency initiatives or requested by individual customers. In the latter case they are frequently conducted by third parties such as freelance auditors or established consulting firms. The dangers here include unfamiliarity with the local context, insufficient transparency concerning auditors’ activities, and lack of thoroughness. Superficial audits may be misused for greenwashing, and the certificate has no real value.101

The example of China demonstrates the importance of the quality of auditing. Inadequate reporting and disclosure by Chinese refiners participating in international certification systems has been documented.102 As a result their business practices remain opaque and information about the origins of their raw materials is unavailable. This is a problem because there are no alternative means of verification.

Comparing Metal Supply Chains: Platinum and Copper

Alongside the general challenges of implementing and enforcing sustainability standards in metal supply chains, certain metal-specific factors are central to sustainability governance. The specific structure of a raw material supply chain shapes the (possibilities of) participation and influence of states and other actors. If we are to identify the potentials for and obstacles to sustainability initiatives, we need to adopt a material-specific perspective. The following investigation of the examples of platinum and copper is based on our analysis of interviews conducted in 2021–22, supplemented by secondary sources.

Structural differences

The supply chain for platinum from southern Africa to the EU is shorter than the copper supply chain and exhibits greater geographical and firm concentration, especially in the first two stages. This makes it easier to identify material flows and participants than in the lengthier and more diversified copper supply chain.

In 2022, Europe had the world’s third-largest demand for platinum, after China and North America. Within the EU, Germany is the biggest importer (see Table 1, p. 30).103 Platinum is used in catalytic converters and thus an important input for the European car industry. Other industrial uses are found in the chemicals, electronics and medical sectors. Platinum is also used in jewellery, and increasingly also as a store of value.

Global demand for platinum is currently moderate.104 In the medium term the transition from petrol and diesel to electric vehicles will considerably reduce demand. It remains to be seen whether additional demand will arise in connection with new technologies (such as water electrolysis). A study commissioned by DERA suggests that demand for platinum in a future sustainability scenario will remain below today’s levels.105

Although the EU covers part of its current needs through its own recycling sector it still imports primary material, almost all of which comes from the world’s biggest exporter South Africa and arrives in a refined state. EU companies focus mainly on secondary production and recycling, with important producers being the German Heraeus Precious Metals and C. Hafner GmbH and the Belgian Unicore.106

Most of the world’s platinum reserves are located in South Africa and Zimbabwe, which together accounted for 76.5 percent of global mining output in 2021.107 Accordingly, primary production of platinum (stage 1 of the supply chain) is concentrated in Southern Africa. Ore mined in Zimbabwe is mostly dressed locally, close to the mines (still stage 1) and sometimes also processed into concentrate. But the refining (stage 2) is done exclusively in South Africa.

|

||||||||||||||||

The platinum supply chain also exhibits strong concentration at firm level. Just three transnational corporations dominate the first two stages of the supply chain: Sibanye-Stillwater, Anglo American Platinum and Impala Platinum. They control a large proportion of South African mining, and operate the refineries there, which process raw material from across the region. In addition they run the platinum mines in Zimbabwe, sometimes through subsidiaries. They often have long-term purchase contracts with smaller South African mining firms (offtake agreements), because refineries are costly to operate and only profitable above a certain threshold. Even though certain South African refiners have already been externally certified, for example under the LPPM Responsible Sourcing Standard, they still represent a chokepoint with all the associated problems of lack of transparency (see info box “Chokepoints”, p. 27).

The three largest importers of South African platinum are the United States, Japan and the United Kingdom.108 Platinum is traded through various channels, with a significant proportion over-the-counter – through LPPM in London – and via other specialised intermediaries. On the other hand, there are also direct contractual relationships between mining firms and those that conduct intermediate and final processing (some of which are European). But the physical product is often exported directly from the producer to the final customer. Because platinum is used in small amounts and has an extremely high value-to-weight ratio, it is usually transported by air freight.

While China plays no relevant role in platinum mining, it is a significant user of the material. In China – unlike Europa and North America – platinum is used principally for jewellery.109 Even if global demand for platinum is currently moderate, strong potential price and supply risks must be assumed. The reasons for this include strong concentration in mining and processing, as well as existing risks in source countries such as disruption of mining through strikes and protests. DERA accordingly classifies platinum as a supply risk and the EU also included platinum group metals in its 2020 list of critical raw materials.110

|

||||||||||||||||

The supply chain for copper from the Andes to the EU is longer than that for platinum. Copper mining is more globally diversified, with Chile and Peru the largest producers. On the other hand there is strong concentration in smelting/refining and industrial processing, which are centred on China.111

Germany has the most significant copper industry in the EU, and is the world’s fourth-largest importer of copper ores and concentrates after China, Japan and South Korea (see Table 2, p. 31). Major copper producers such as Aurubis and Wieland are German-based. Copper is a very widely used material, and is crucial in construction, engineering and electronics.112 It is also important for the transition to green energy and for numerous emerging technologies.113 For this reason demand for copper is forecast to increase massively. IRENA predicts global demand of 50 to 70 megatonnes in 2050, compared to 30 megatonnes in 2021.114 In light of the expected growth, recycling cannot be expected to cover demand in the medium term.115 Even if the EU already has significant copper recycling capacity, it remains highly dependent on the primary raw material.

The first stage of the copper supply chain is less concentrated than in the case of platinum, with meaningful reserves on all continents. Nevertheless, Latin American mining and export of primary raw material is crucial for the global market. Chile is one of the world’s biggest copper producers and an important supplier of copper ore and concentrates to the EU.116 Peru also exports significant quantities. The market share of small and medium-sized mining firms in the Andean copper sector is larger than for platinum in Southern Africa, but the market is ultimately still dominated by a handful of very large operators: Chile’s state-owned CODELCO and multinationals (MNCs) like Glencore and BHP.

The copper supply chain is bound up with a complex transnational transport infrastructure. While Chile possesses the world’s second-largest copper refining capacity, Peru’s is marginal.117 Both export most of their copper concentrate to China. Copper concentrate is a bulk product requiring complex logistics and transnational shipping.

Concentration in refining (stage 2) has increased over the past two decades, with additional capacity appearing principally in China. In 2019 China was the world’s biggest producer of refined copper, accounting for around 41 percent. China has also developed a large industrial processing sector (stage 3), both for its own consumption and as a global exporter of precursors and semi-finished products. Today China accounts for more than 50 percent of global demand.118

Material flows in the copper supply chain are especially difficult to trace, because diversification on the mining side is greater and the transnational transport routes are opaque. The chokepoint of Chinese smelting/refining presents a real challenge (see info box “China’s dominance”, p. 9). And the copper trade – another chokepoint – is considerably less centralised than the platinum trade. As a base metal, copper is traded in large volumes through transnational brokers and metal exchanges across the world, including the LME in London. The decentralised nature of the trade is a function of the very large volumes consumed by industry, where copper is used in countless different products.

On account of the moderate geographical concentration and country risks, DERA rates copper mining as uncritical; nor is it included in the EU’s list of critical minerals. On the other hand the degree of concentration in industrial processing in China warrants close observation.119

Lead firms and state cooperation

Their position towards the end of the supply chain offers European actors little direct influence over sustainability governance in mining and processing. If political decision-makers or businesses wish to take action to influence sustainability, they are dependent on cooperation with other actors. These differ from supply chain to supply chain and therefore need to be identified on a case by case basis.

European actors should collaborate with lead firms to manage sustainability in metal supply chains.

While research indicates that so-called lead firms are central to establishing standards in many transnational supply chains,120 our analysis of the copper and platinum supply chains reveals that no enterprise in either possesses sufficient market power to ensure the implementation and observance of particular standards on its own. There are, however, a number of companies whose position enables them to positively influence sustainability governance.

These are well-organised companies, mostly MNCs, operating in the first two stages of the supply chain. They play a leading role, often in connection with strong concentration at firm level, and are (theoretically) able to ensure that their suppliers introduce standards and have them regularly verified. They are also able to directly influence others, from smaller market participants to state institutions. The more vertically integrated these companies are, the better they are able to achieve this.121 This applies not only to mining firms but also to smelters/refiners and traders, and in particular to firms involved in several stages in the supply chain. Examples of the latter include Anglo American, which operates mines, smelters and refineries, and Glencore, a Swiss commodity trading and mining company. Such companies are in a particularly good position to make material flows transparent, and can supply urgently needed information (see info box “Chokepoints”, p. 27).

The most important actors in Southern Africa are the three market leaders, which control a large share of the platinum mining, smelting and refining: Sibanye-Stillwater, Anglo Platinum and Impala Platinum.122 They hold great sway over platinum extraction, smelting and refining in Southern Africa. And they influence South African mining ministry and other relevant actors in the area of standard-setting, in particular through the Minerals Council South Africa (MCSA).123 They are also able to influence working and production conditions in their facilities in Zimbabwe. The example of platinum also underlines the advantages of direct long-term supply contracts between producers and industrial users. They can improve cooperation and above all improve transparency in the supply chain. International trading centres like LPPM in London can achieve similar advances when they introduce standards (see pp. 21f.). Firms in Europe are therefore often relatively well-informed about the origins of their imported platinum.

When it comes to sustainability governance in the more diversified copper supply chain from the Andes to the EU, the Chilean state-owned CODELCO and a handful of MNCs are the decisive actors.124 Fundamentally, vertically integrated companies that are involved in multiple stages of the supply chain wield great influence. That certainly applies to CODELCO, whose state-owned status and dominance of mining and processing lend it a dual role in implementing and enforcing standards. Commodity traders like Glencore and metal exchanges like the LME also possess great sway over sustainability governance in the copper supply chain. They are only beginning to introduce standards for sustainability and transparency, so scope and enforcement still leave room for improvement (see pp. 21ff.). This is also relevant with respect to China, where traders often represent the link to the European market and are in a position to pass on sustainability and transparency requirements.

Most of the influential MNCs that dominate the two first stages of the supply chains analysed in this study are organised in the International Council on Mining and Metals (ICMM). Its guidance is influential, also on other MNCs and SMEs in the mining sector. SMEs tend to have fewer resources at their disposal for influencing their business partners to introduce and implement standards. Given sufficient demand, smaller, uncertified mines will also be able to find local or international customers, even if their standards are looser.125 Larger enterprises and industry associations tend to intervene more strongly. They are able to generate (public) pressure, and offer guidance and concrete support for implementation.

The industry-backed Copper Mark is becoming increasingly established as a resource-specific standard in the copper supply chain; the production facilities of certain European companies, including German-based Aurubis, have gained Copper Mark certifycation. It has also been awarded to a number of mines in important copper-producing countries like Chile.126 In the platinum sector, the multi-stakeholder initiative IRMA is increasingly important, not least on account of pressure from industrial users (in particular the European car industry).127

(Large) European companies exert influence largely through their direct relationships with producers in mining countries. But smaller buyers may find it difficult to trace their supply chains or to establish effective instruments with which to influence upstream sustainability. Remedying this requires state support measures, such as national helpdesks on business and human rights, the UN Human Rights Toolkit or the ILO Helpdesk for Business on International Labour Standards. Exchange between actors within a sector is also useful, for example through the Automobile Industry Sector Dialogue in Germany.