The Geopolitics of Hydrogen

Technologies, Actors, and Scenarios until 2040

SWP Research Paper 2023/RP 13, 16.11.2023, 45 Seitendoi:10.18449/2023RP13v02

ForschungsgebieteDr Jacopo Maria Pepe and Dr Dawud Ansari are Associates, Rosa Melissa Gehrung is Research Assistant in the Global Issues Research Division at SWP.

This SWP Research Paper was produced as part of the project “Geopolitics of the Energy Transition – Hydrogen”, which is funded by the German Federal Foreign Office.

The scenarios present purely hypothetical developments, and the countries mentioned therein serve only as examples and do not reflect the opinions of SWP.

-

The transition to a hydrogen-based economy is gaining momentum in both Germany and the European Union (EU). Used as an energy carrier, hydrogen holds the promise of freeing hard-to-decarbonise sectors like heavy industry, aviation, and maritime trade from their emissions. At the same time, policymakers hope that hydrogen will promote Europe’s energy independence, push sustainable development, and strengthen value-based trade.

-

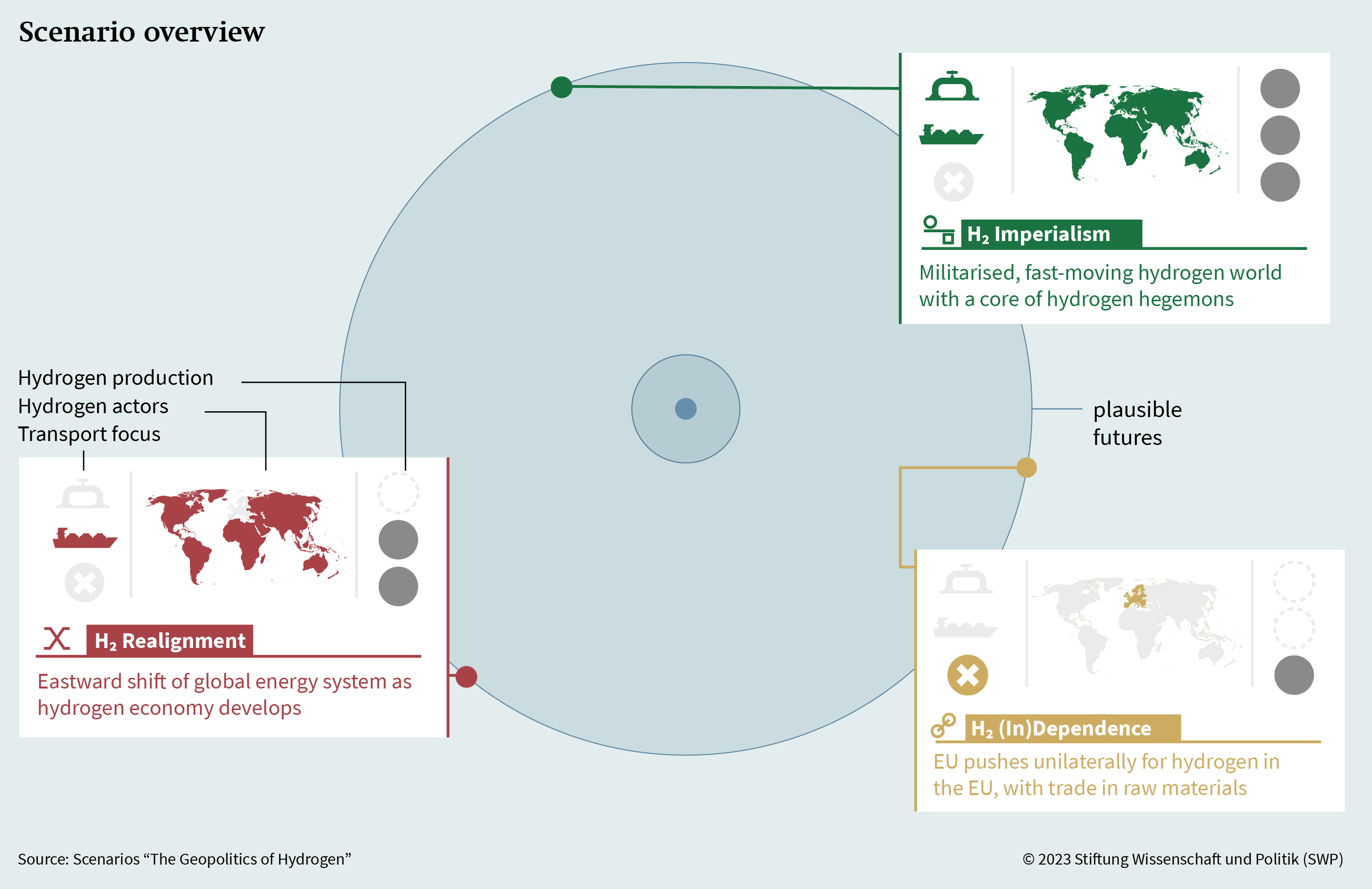

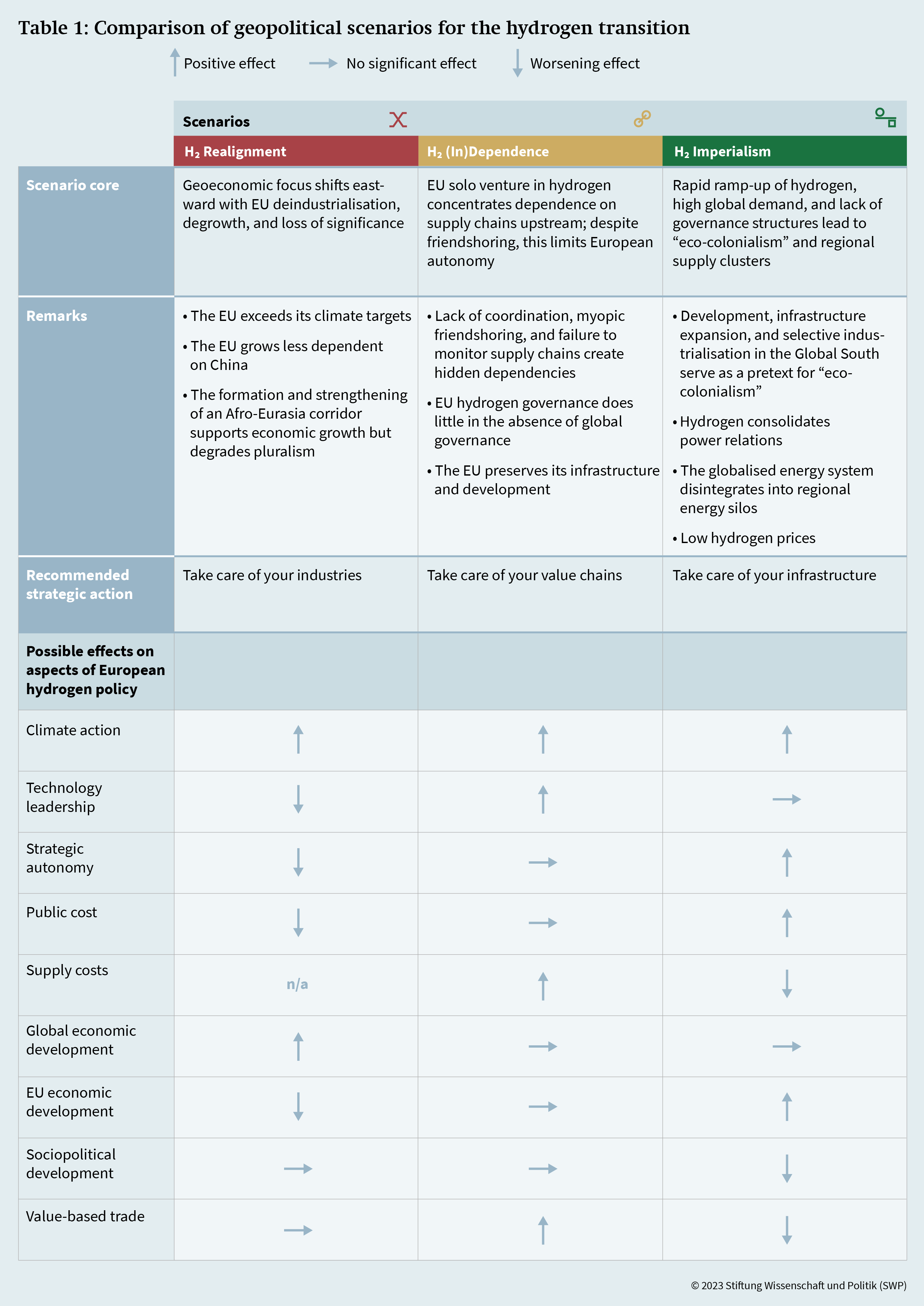

This study presents three plausible yet disruptive scenarios for the geopolitics of hydrogen up to the year 2040 (developed with a team of experts in a multi-stage foresight process). “Hydrogen Realignment” considers the possibility of an eastward shift of industry, power, and technological leadership; “Hydrogen (In)Dependence” depicts a future, in which Europe pursues hydrogen self-sufficiency but becomes dependent on raw material supply; and “Hydrogen Imperialism” delves into the dystopian scenario of a hydrogen transition dominated by hegemons and despots.

-

The transition to hydrogen is likely to shift and complicate Europe’s external dependence rather than eliminate it; the role of supply chains will become more important. Moreover, the potential of hydrogen trade for global sustainable development is limited and requires targeted efforts.

-

Resource distribution, production potential, current geopolitical power dynamics, and their interplay will influence hydrogen policy and decision-making along the entire value chain, with actors often giving priority to socioeconomic, geopolitical, and technopolitical considerations.

-

Germany and the EU must pursue a proactive hydrogen strategy, acknowledge the preferences of external actors, and form pragmatic partnerships to keep sight of climate goals, retain industry, and avoid losing global influence.

-

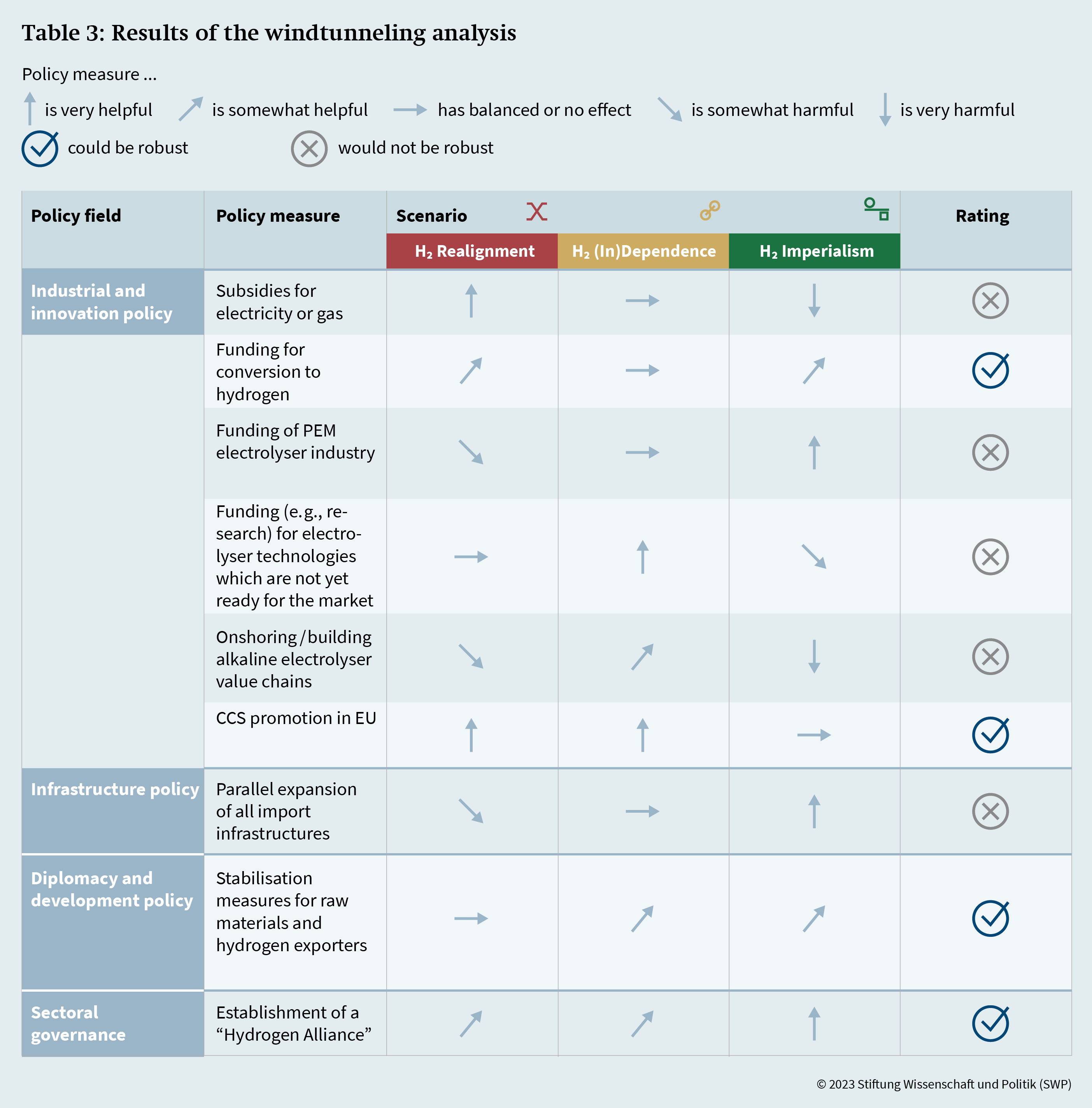

In addition to promoting targeted technologies, decision-makers must manage dependencies across sectors and do so in an anticipatory way. Pursuing diversification is indispensable, and instituting targeted diplomacy and development assistance would be helpful. The new hydrogen sector also needs governing institutions – for example a “Hydrogen Alliance” – to mitigate geopolitical risks and allocate investments correctly.

Table of contents

2 Geopolitics, hydrogen, and scenarios for the future

2.1 The geopolitics of hydrogen: Resources, technology, power, and the world order

2.2 Using strategic foresight to envision hydrogen geopolitics

3 Technology pathways, modes of transportation, and regional preferences: An overview

3.1 Technologies, resources, and dependencies: Hydrogen production

3.2 Pipelines, shipping, and choke points: Geopolitical transport challenges

3.3 Regional incongruities and geopolitical divergences

3.3.1 Europe on the edge: Between wishful thinking and (geopolitical) reality

3.3.2 Continental Eurasia in transition: Geopolitical impacts on hydrogen potential and priorities

3.3.3 Africa and the Middle East: Great opportunities meet great expectations

3.3.4 The Indo-Pacific in flux: Hydrogen politics between global and middle powers

4 Three scenarios for the geopolitics of hydrogen

4.3.1 Harder, better, faster, stronger

5 Analysis and evaluation of the scenarios

5.1 Ambivalent futures: Climate and development

5.2 Hydrogen Realignment: Hydrogen between Eurocentrism and eastward shifts

5.3 Hydrogen (In)Dependence: Friendshoring is no substitute for diversification

5.4 Hydrogen Imperialism: Tension and mismanagement are unleashed on the Global South

6 Recommendations for a proactive hydrogen policy

7.1 Methodology and the Foresight Process

7.2 Participants in the Foresight Process and Acknowledgments

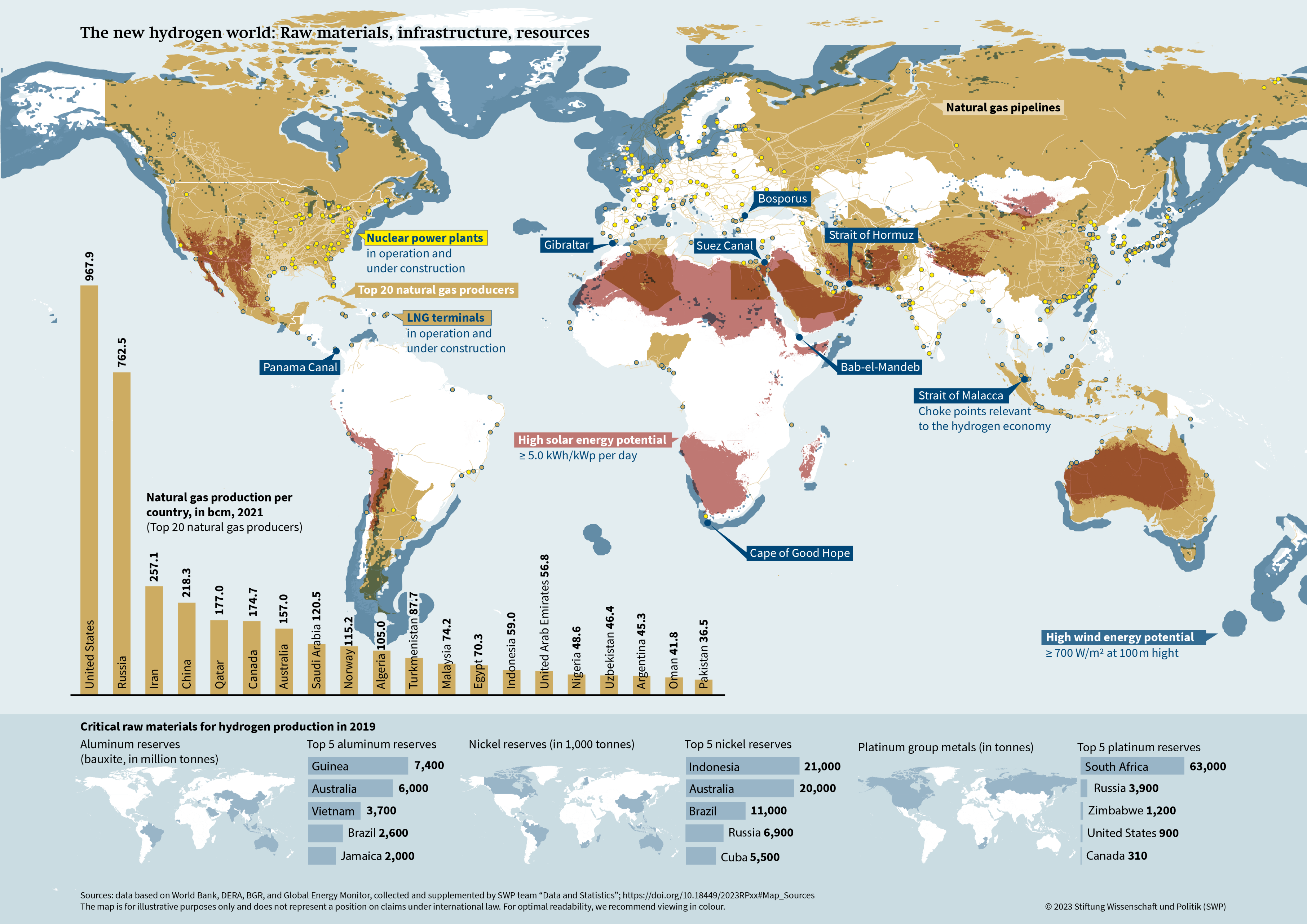

7.4 Sources for map (p. 9 ) “The new hydrogen world: Raw materials, infrastructure, resources”

Issues and Conclusions

Governments around the world are throwing their weight behind the new “hydrogen economy”– particularly in Germany and the EU. Clean hydrogen could ultimately help decarbonise such economic sectors as heavy industry, aviation, and maritime trade, thereby mitigating climate change. However, recent geopolitical events such as the Russian invasion of Ukraine have cemented the previously latent shift in the EU’s narrative of the energy transition – from climate action and justice towards strategic autonomy and industrial policy. Policymakers are thus eyeing hydrogen as a way to achieve long-term energy independence. At the same time, Germany and the EU will have to rely on hydrogen imports – a fact that throws a spotlight on the international dimension of hydrogen. As that dimension evolves within a maelstrom of surging (technological, industrial, and systemic) competition, security tensions, and the fragmentation of global supply chains, it is ever more important to consider the geopolitics of hydrogen.

Studies on the dynamic interactions of market factors, geopolitical path-dependency, and national motives vis-à-vis the hydrogen economy are absent so far. The current discourse in Germany and Europe has yet to consider anything but domestic technological, regulatory, and political preferences; the intentions of other actors are practically absent. Yet the preferences of foreign actors are diverse, dynamic, and reflect the geopolitical environment. Simultaneously, policymakers formulate a growing number of (sometimes inconsistent) expectations for the hydrogen transition – ranging from global sustainable development to restricting trade to narrow “value-alliances” to energy independence. Since conflicts, dependencies, and market setups can and might be reshaped for decades to come, it is essential for Germany and Europe to identify and strategize relations, trade-offs, risks, and interdependence.

This study provides a first overview of the geopolitics of hydrogen. In addition to presenting technology choices and preferences emerging in the hydrogen economy, we present three novel, interdisciplinary scenarios – “Hydrogen Realignment”, “Hydrogen (In)Dependence”, and “Hydrogen Imperialism” – for the hydrogen world up to 2040. These scenarios offer disruptive yet plausible futures that highlight conflicts, risks, opportunities, and potential for action.

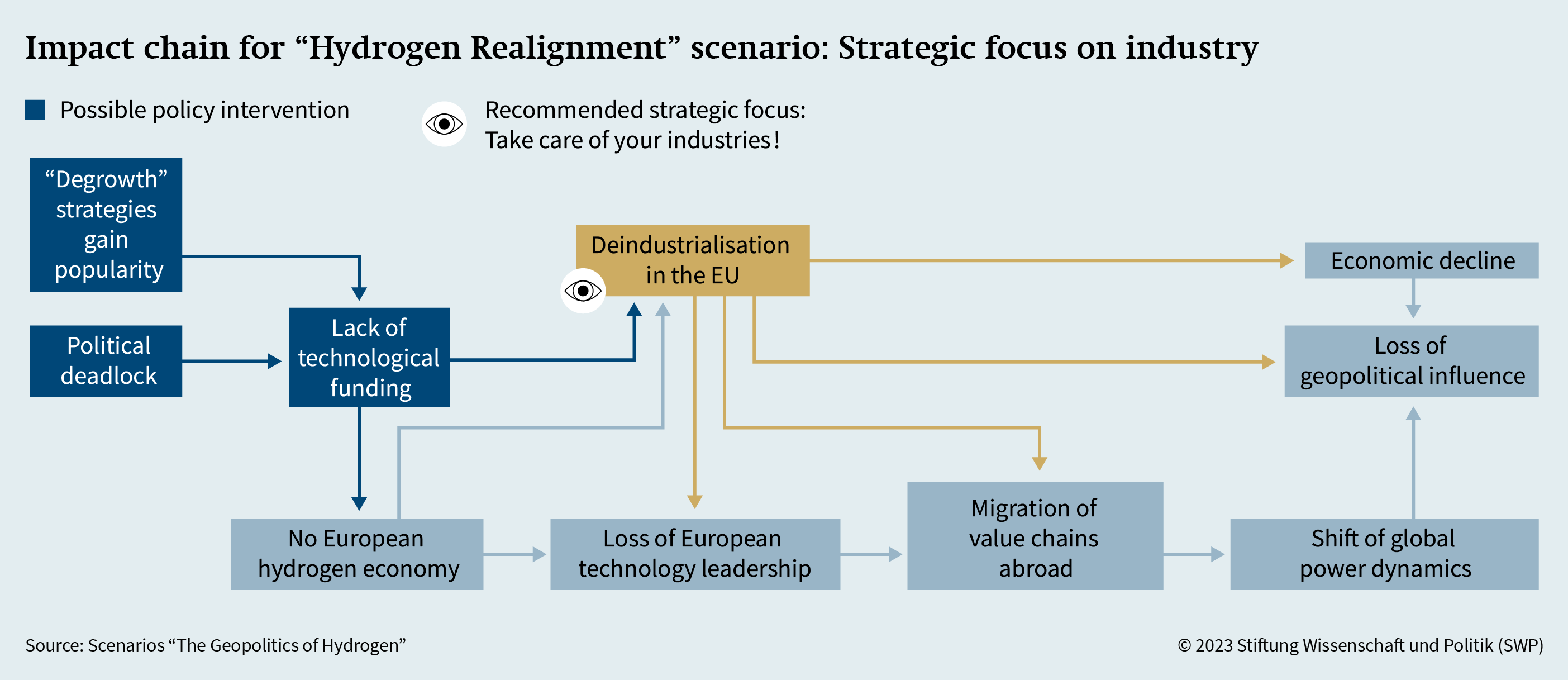

“Hydrogen Realignment” envisions the combined effects of ambitious Chinese hydrogen governance and European deindustrialisation – foretelling a shift in energy flows, industry, and geopolitical power towards the Gulf and Asia. New power dynamics and supply chains emerge within Afro-Eurasia, while Europe meets its climate goals but loses its geopolitical influence.

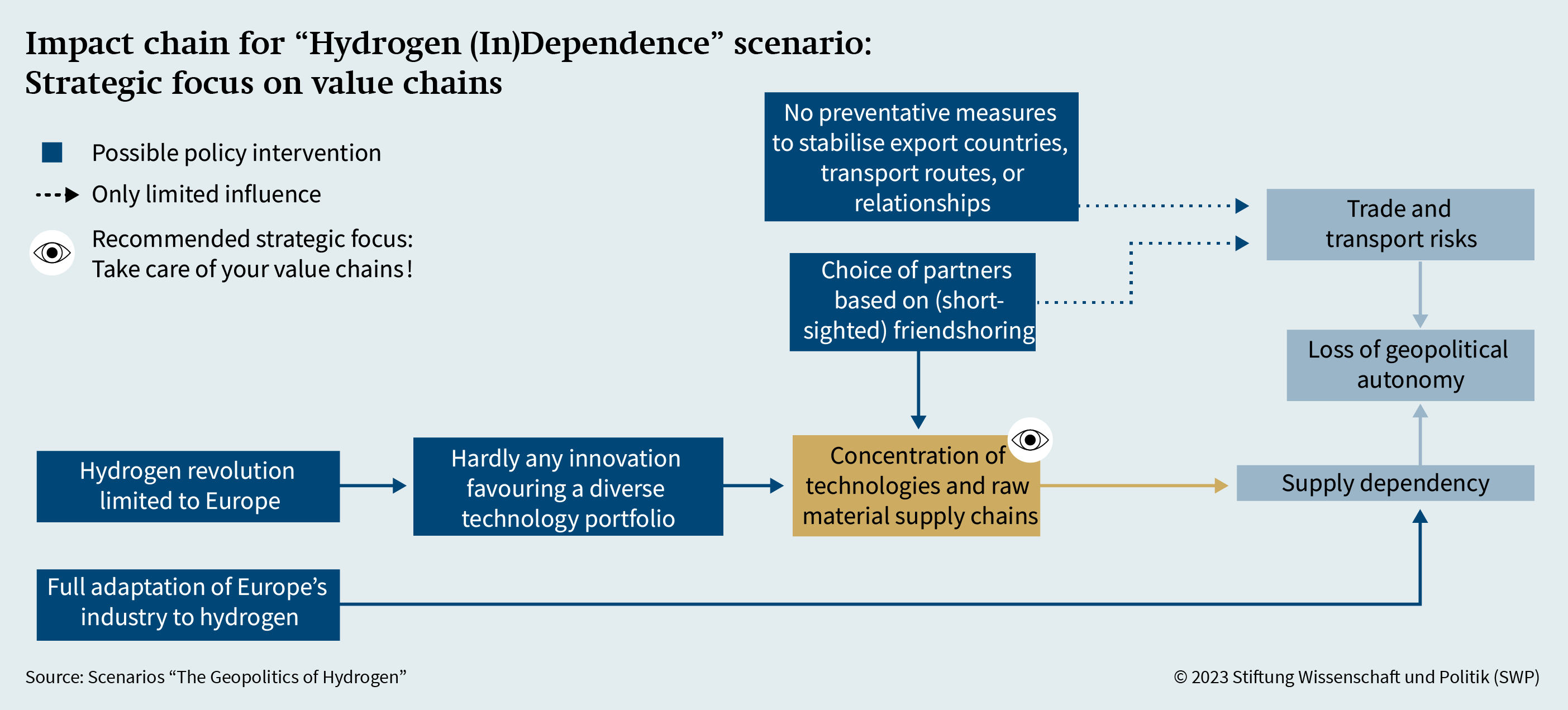

“Hydrogen (In)Dependence” pictures a more fragmented world in which only Europe commits to the hydrogen transition – as part of its quest for energy autarky. However, previously ignored dependencies on raw material supply from foreign actors ultimately threaten the EU’s security autonomy, forcing it back into the energy trade.

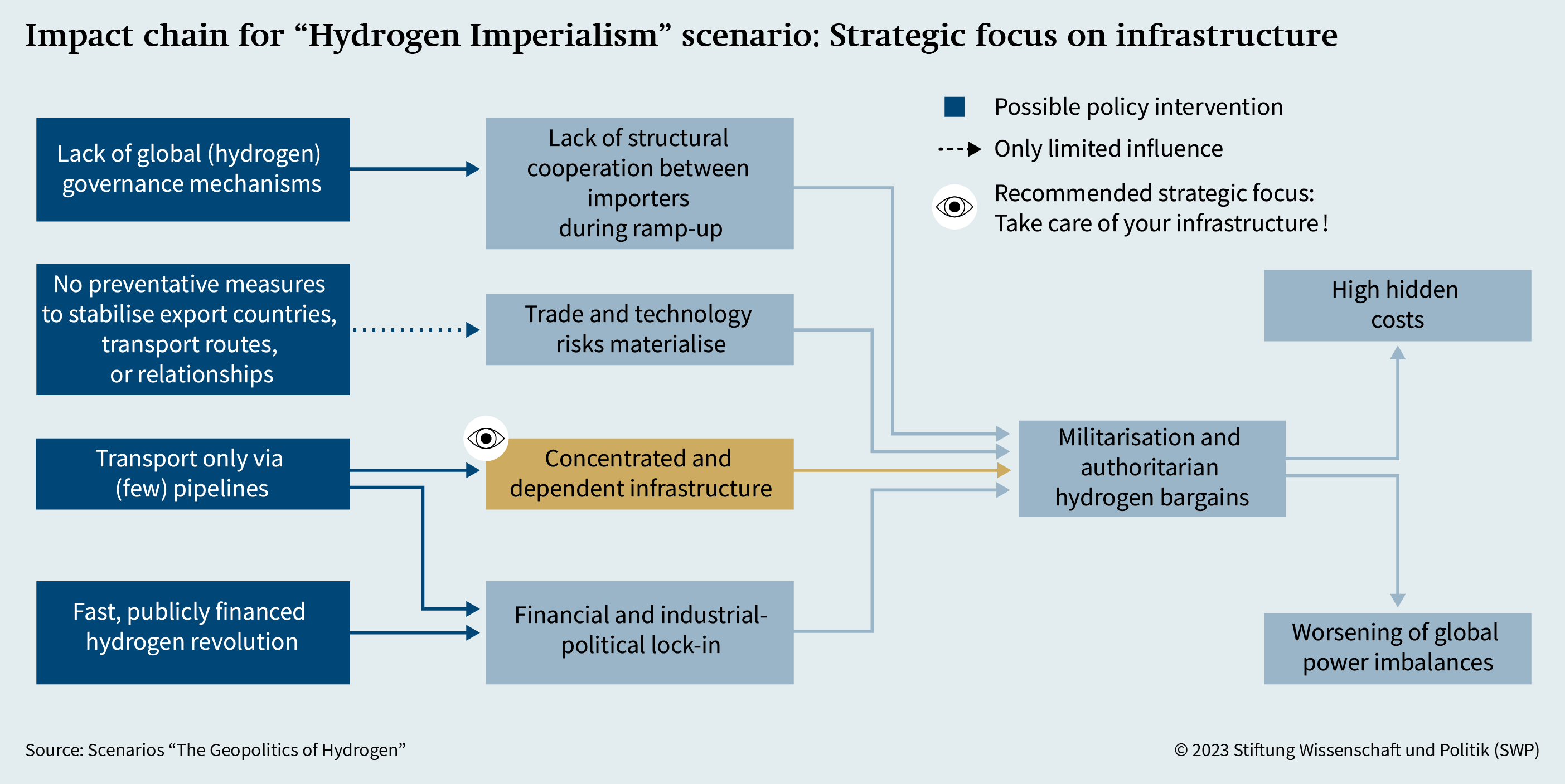

“Hydrogen Imperialism” explores the dystopian vision of a hydrogen-powered throwback to the era of historical protectorates. A unified push for hydrogen kicks off a race to divvy up value chains and exporters, but things go south when security incidents force large importers to become more assertive – and the original premise of “international development” becomes a pretext for supporting hydrogen dictatorships.

The study demonstrates that while hydrogen has the potential to significantly disrupt present energy geopolitics, it cannot overturn its basic premises. Under certain conditions, the degree of foreign energy dependence may indeed weaken. However, as value and supply chains grow more intricate and dispersed, dependencies may also end up becoming more complex and difficult to monitor. Even an economy that does not import hydrogen or its derivatives can still depend on other parties for raw materials, hydrogen technology, and components. Moreover, the hydrogen market may not necessarily develop in alignment with established structures and the goals European policymakers expect. Most governments prioritise socioeconomic, geopolitical, and industrial factors over climate policy; a fact that could result in growing asymmetries and incongruities between European consumers and global producers.

Despite ambiguities, challenges, and a persistent degree of foreign energy dependence, Germany and the EU should continue to consider hydrogen as essential for their energy transition efforts. Hydrogen will enable Europe to achieve climate targets while preserving its industries – and even establishing new ones; meaning the “old world” can make use of its geopolitical potential in an era of heightened competition for key industries. This will require four essential steps from Germany and the EU to proactively help the hydrogen landscape.

1) They must understand the preferences of non‑European actors and acknowledge realities. In dealing with external actors and selecting partners, they should take a pragmatic, compromise-oriented, and ambitious approach, as narrowly Eurocentric visions of the hydrogen economy do not reflect reality. If they do not, Europe risks not only missing its climate targets but also losing out in the global competition to acquire technology, set standards, and maintain influence.

2) They should promote technologies and industries in a targeted way. While it is generally advisable to support industry’s adaptation to hydrogen as well as versatile technologies like carbon capture and storage (CCS), Europe should also ensure that the technology portfolio it promotes be closely aligned with future geopolitical developments and energy sector dynamics.

3) They must actively manage dependencies connected to the hydrogen economy. Complex value chains call for comprehensive cross-sector dependency management, including managing raw material chains. Here, diversifying technology, raw material sourcing, and energy imports are crucial, regardless of the trading partner. Accompanying development policy and diplomacy that considers the interests of partner countries can help mitigate risk.

4) They must work to establish global hydrogen governance. A governance structure can help allocate investments correctly, mitigate the drawbacks of purely bilateral trade structures, and reduce geopolitical risks. One such format could be a “Hydrogen Alliance”, a multilateral, two-tiered trade club. Without suitable governance mechanisms to consider all potential market actors and acknowledge their agency, hydrogen’s potential to ease geopolitical tensions and promote collaboration will remain limited in the face of an increasingly uncooperative and fragmented world order.

Geopolitics, hydrogen, and scenarios for the future

The establishment of a hydrogen economy is widely considered an essential component of a sustainable energy system, particularly for decarbonising key industrial sectors that would otherwise be difficult to decarbonise. However – not least with the resurgent rivalry between the United States and China and Russia’s aggression against Ukraine – energy supply security, energy autonomy and resilience, and the struggle for technological leadership have remerged as central paradigms of both energy policy and foreign policy more generally.

While scholars have investigated how these factors interact for conventional energy sources, the geopolitics of hydrogen is still uncharted. Most studies of the hydrogen economy focus on the technologies, costs, resources, and infrastructure; they then extrapolate implications for the future geopolitical and market landscape from these aspects.1 Literature on the geopolitics of the energy transition meanwhile has yet to give adequate attention to the impact of existing (geo-)political dynamics overall and the individual preferences of potential market actors in particular. Energy scenarios for their part have yet to address the nexus of geopolitics and hydrogen.2

Examining the geopolitical implications of hydrogen requires identifying and mapping prospective actors, conflicts of interest, risks, and potential dependence relationships. Here the tools of strategic foresight prove useful.

The geopolitics of hydrogen: Resources, technology, power, and the world order

Geopolitics refers to the interaction of geographical factors (location, space, and resources) with political processes. The geopolitics of energy traditionally examines the impact on interstate power dynamics of concentrated (fossil) energy resources, including their transportation and trade.3 The interrelationship of geopolitics and energy markets is of course complex and anything but unidirectional.

The geographical concentration of fossil-fuels (coal, oil, and gas) has influenced patterns of power and prosperity ever since the Industrial Revolution. Energy resources have long served as a currency of power, a strategic asset, or a source of conflict. Technology, together with the distribution and concentration of resources, is key to the geopolitics of energy. New technologies can unleash major changes in extraction, production, transport, and distribution, thus triggering tectonic shifts in the geopolitical power balance. For instance, technological innovations influence the strategic importance of individual energy sources and promote new value chains, supply chains, and trade routes. This in turn may affect infrastructural and trade-related interdependence, redrawing economic and energy landscapes.

It is important to recall, however, that neither resource distribution nor technology are inherently “geopolitical”. Rather, they gain geopolitical significance only when they are “deployed in a political direction.”4

Market mechanisms and certain market configurations can minimise dependence risks, defuse conflicts, and depoliticise interdependence. However, existing geopolitical power constellations influence the political preferences of state and non-state actors and ultimately affect market mechanisms. This in turn influences energy relations, flows, and markets.

This reciprocal relationship between geopolitics and energy markets extends to the global order.5 On the one hand, energy relations have the potential to shape the global framework. (Arabia’s political integration in the world system in the 20th century is one example; Soviet/Russian gas exports into Eastern European economies before 2022 is another.) On the other hand, the global framework shapes the conditions for energy relations. A multilateral world order with well-functioning global institutions and global governance mechanisms is more conducive to the unimpeded flow of energy, open and liberalised markets, and fair competition than an environment with weak global governance institutions, competing powers, and a lack of cooperation among states. For example, the gradual liberalisation of energy markets and the pursuit of global energy governance (with the Energy Charter Treaty of 1991) occurred in a period of growing acceptance of a liberal, multilateral world order largely shaped by the West at the end of the Cold War.

The “new” energy world is even more dominated by technology, raw materials, and the desire to set regulatory and technological standards.

The ongoing transformation of the energy system, much like the current system based on fossil fuels, has its unique geopolitics. But the “new” energy world is even more dominated by technology, (critical) raw materials, and the desire to set regulatory and technological standards and maintain industrial leadership.6 Renewable energy resources are generally less concentrated (fig. 1). However, value chains and supply chains are longer, more convoluted, and spatially more dispersed; they are also more interconnected than in the case of fossil energy sources. Such factors craft and shift dependencies at different stages of value and supply chains along with their geography, making them potentially more complex. States, public entities, and private companies are competing for access to resources and transport routes as well as for key markets, components, production processes, industries, and their maintenance, and even investment flows and financing.

The geopolitics of hydrogen will presumably follow – and exacerbate – these trends. Depending on production technology, certification path, transport option, and final products, distinct value chains, supply chains, and production networks arise. Exporters of technology, hydrogen, and raw material therefore have a vested interest in establishing and proactively shaping dependence relationships, be it through technological and market leadership or through path-dependencies that favour specific technologies in production, transportation, or application.

Hydrogen’s resource, technology, and transportation landscape is indeed diverse (fig. 1). The new hydrogen world could well alter the role of concentrated resources as a determinant of the geopolitics of energy. For example, natural gas (one possible source material for hydrogen) is relatively concentrated, but other resources for hydrogen production such as solar and wind energy (as well as nuclear power plants) are more evenly distributed. Diversification could reduce the risk of geographic concentration. At the same time, critical raw materials (like nickel and platinum), their extraction, and their processing are crucial for hydrogen production. Like natural gas, these materials are rather concentrated, although they involve different owners. Transportation is yet another crucial issue. Building up new or/and upgrading existing infrastructure (especially ports, freighters, and pipeline networks) will tie-up major resources, and investment decisions will thus forge long-term interdependence and greatly influence the topographies of actors and power in the hydrogen sector.

In addition to technologies, resources, and transportation routes, political decisions (heavily influenced by competing connectivity, industry, and energy policy preferences) are crucial in shaping markets and geopolitical developments.7 Current power dynamics – particularly increasing fragmentation, the erosion of the liberal order, and geopolitical competition as reflected in (re)militarisation of global affairs – may thus have a direct impact on the nascent hydrogen economy and significantly shape future hydrogen geopolitics. For instance, in addition to the US-China rivalry and the ongoing tensions between the EU and Russia, various actors are realigning their priorities and preferences – including emerging powers like India and regions with new geopolitical weight like the Gulf States. Even within the traditionally strong and value-driven transatlantic relationship, fault lines are emerging.

Although it is far from clear who the winners and losers of the emerging hydrogen economy will be, a more precise exploration of hydrogen’s geopolitical implications is indispensable, not least in aiding the EU and Germany as they develop coherent courses of action.

Using strategic foresight to envision hydrogen geopolitics

The geopolitics of hydrogen is emblematic of the “VUCA world” – it is developing in an environment characterized by volatility, uncertainty, complexity, and ambiguity.8 Such an environment renders reliable predictions of future developments infeasible, which is why we turn to strategic foresight and scenario generation.

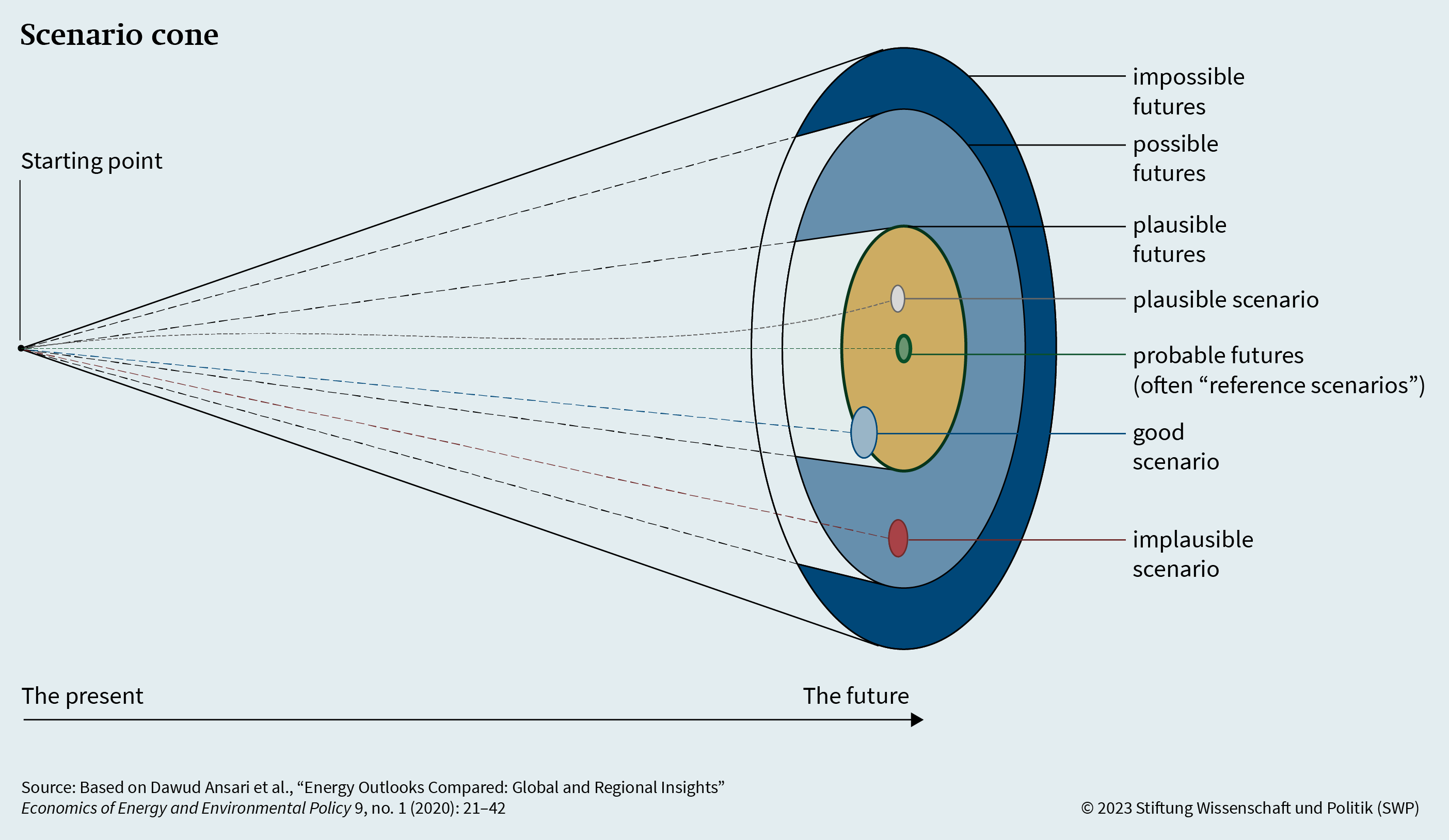

Scenarios are hypothetical sequences of events that lead from the present to an endpoint in the future (see fig. 2).9 Their purpose is to explore and anticipate uncertain developments, unknown factors, and emerging opportunities and risks. Scenarios differ from predictions in both conceptual and practical terms. Predictions rest on the probability of an envisioned future and strive for precision, typically operating in a short-term framework. Scenarios, on the other hand, seek to generate new insights and create preparedness, and their main criterion is plausibility, meaning that they demand internal consistency and credibility. They may even deliberately target visionary or improbable futures in an attempt to give bounds to the range of possibilities10 (see again fig. 2). The scenario-generating process draws on structured qualitative analysis, heterogeneous and interdisciplinary expertise, and participatory frameworks.

Scenarios eschew rigidity, formality, and reductionism and instead aim at evoking a “memory of the future” with the audience.

The hybrid and fluid nature of scenarios, which occupy the intersection of logic and intuition, is their strength compared to more linear and “sterile” approaches. Scenarios eschew rigidity, formality, and reductionism and instead aim – in a somewhat artistic process – at evoking a “memory of the future” with the audience. Ideally, this enables decision-makers to anticipate previously unforeseen consequences and risks and develop preparedness through strategic options.11

This study presents the first scenarios at the nexus of hydrogen and geopolitics. While scenario foresight has become a centrepiece of the energy sector, geopolitical aspects or security policy are rare — even though the method calls explicitly for interdisciplinary expertise. However, scenarios are arguably the best method of approximating the complex and ambivalent chains of cause and effect in the geopolitics of hydrogen – and assessing them strategically. Before presenting the scenarios, we first map out the technological and technopolitical aspects of hydrogen production and transport and provide an overview of the hydrogen ambitions in different regions and their geopolitical context.

Technology pathways, modes of transportation, and regional preferences: An overview

Currently, there is neither a global nor a regional market for (clean) hydrogen as an energy carrier, and both supply and demand need to be established.12 The range of conceivable production methods, technologies, products, transportation routes, and applications for hydrogen is wide. The paths actors choose to take in the future will be determined, on the one hand, by their political preferences and, on the other, by existing market and power structures. Different requirements for raw materials, components, and know-how will in turn create different energy (market) structures, new relationships of interdependence, and – potentially – new centres of power. Here, an overview of the world’s potential hydrogen actors helps place their respective preferences in geopolitical context.

Technologies, resources, and dependencies: Hydrogen production

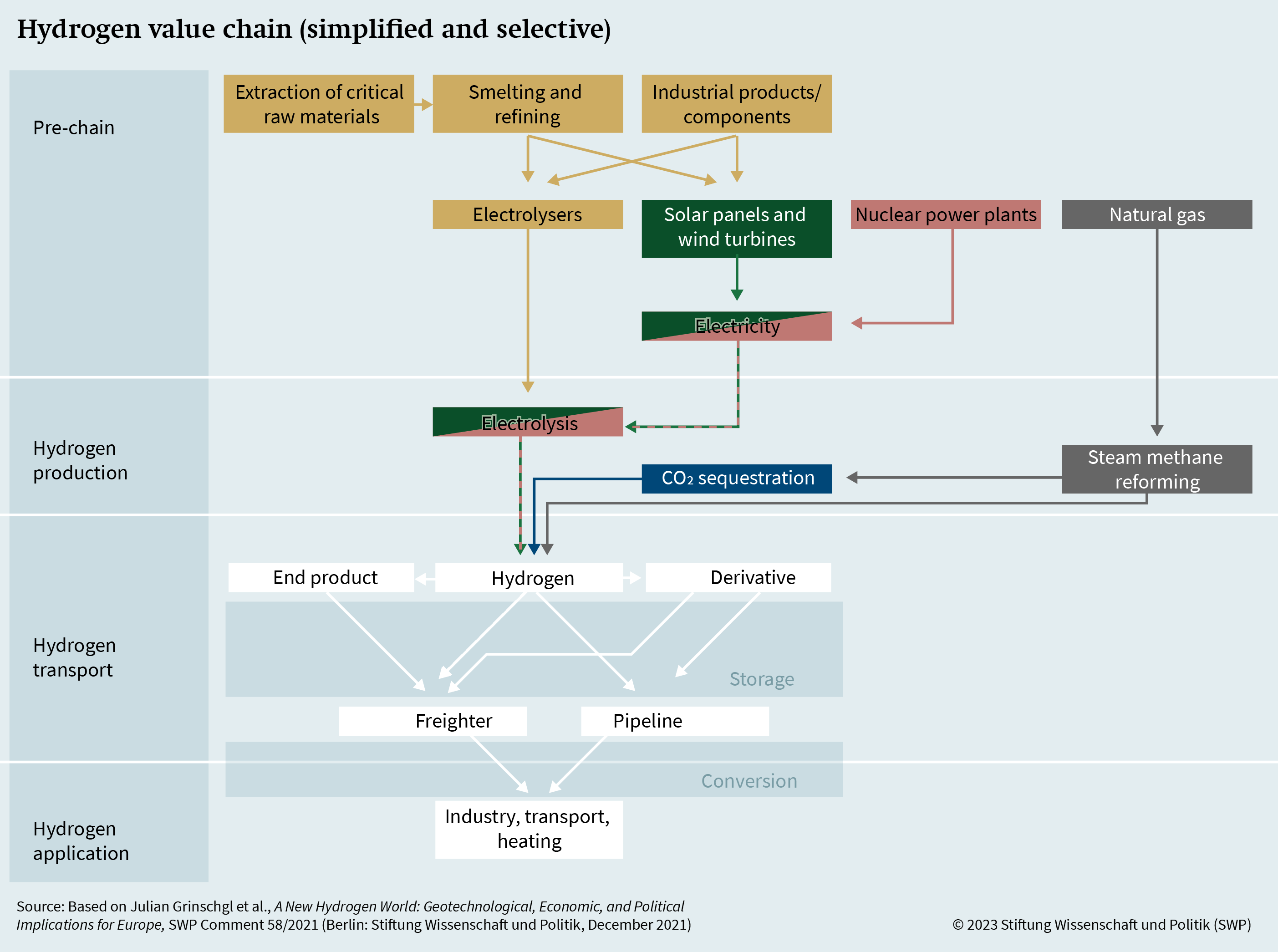

Most hydrogen produced today (>99 per cent) is derived from fossil fuels without methods to reduce accompanying carbon dioxide (CO2) emissions.13 Steam methane reforming (SMR), by far the most common production technique, uses heat and water (steam) to extract hydrogen from natural gas; the process emits large quantities of carbon dioxide and carbon monoxide. In 2021, about 12 to 13 tonnes of CO2 equivalents were emitted for every tonne of hydrogen produced, aggregating to about two per cent of global greenhouse gas emissions.14 Such hydrogen extracted from fossil gas via SMR is often referred to as “grey” hydrogen (fig. 3).15

For hydrogen to become a low-carbon or even carbon-free energy carrier, its production must be decarbonised. The carbon capture and storage (CCS) approach separates the emissions generated during the SMR process and stores them, typically underground.16 The captured CO2 could also find productive use, for example in enhanced oil recovery or potentially as raw materials; the process is then labelled Carbon Capture, Utilisation, and Storage (CCUS).

While this “blue” hydrogen yields fewer carbon emissions, the process is not entirely carbon-free. The residual emissions depend on the efficiency of the CCS/CCUS plant involved. Compared to renewable energy sources – which have received extensive research and government support over the past decades – CCS and CCUS technologies are still largely immature and can at present only capture a portion of total emissions. Estimates of future emission reductions vary widely; moreover, it is necessary to stop methane leaks in the natural gas supply chain.17

The cost of producing hydrogen using SMR depends significantly on the price of natural gas. From a European perspective, this increased notably with the onset of the 2022 energy crisis – at times reaching approximately 5 to 8 euros per kilogram.18

From a geopolitical perspective, low-carbon hydrogen from natural gas could consolidate and prolong the power of natural gas producers, who could continue to export gas via established trade relationships. The race to bring CCS to the market (along with the extent of natural gas reserves) will determine the degree to which fossil fuel exporters gain a foothold in renewable energy markets. Completed and planned commercial facilities are mainly located in North America, Australia, northern Europe, the Gulf States, China, and Southeast Asia, with capacity expansion planned, particularly in Europe and the Asia-Pacific region, to take place by 2030.19

However, Germany and the EU are focussing their hydrogen ambitions on producing hydrogen through water electrolysis powered by renewable electricity – so-called green hydrogen.20 Electrolysis involves using an electrolyser to split water (H2O) – or potentially other liquids – into oxygen (O) and hydrogen (H2). Hydrogen from electrolysis will be carbon-free, if the electricity has been generated without emissions (for example, from solar-, wind-, or nuclear power).

With current costs ranging from 4.60 to 7.30 euros per kilogram, green hydrogen is rather expensive.21 These costs, which will decrease over time, generally depend on the cost of developing renewable energies (and, thus, on geographical and meteorological factors). For example, estimates for 2030 see production costs for green hydrogen at around 1.90 euros per kilogram in sub-Saharan Africa and approximately 1.50 to 2 euros in the Gulf States.22

Electrolysers and the raw materials needed to manufacture them (see again fig. 1) are critical to scaling the market for green hydrogen.23 Two types of electrolysers currently prevail: alkaline electrolysers and polymer electrolyte membrane electrolysers (PEM).

Alkaline electrolysers are the oldest, most cost-effective, and most widely used technology, accounting for 61 per cent of globally installed capacity. They require nickel and (nickel-plated) steel. Nickel processing takes place primarily in Indonesia, China, and Japan.24 As some countries (like Indonesia) strive to prevent the export of unrefined nickel, China is securing on-site smelting capacities in these mining countries through strategic investments. This gives China the ability not only to produce most of the world’s alkaline electrolysers but also to offer them at a cost of approximately 190 euros per kilowatt (kW) – one-sixth of the European price.25

PEM electrolysers are slightly better suited to the fluctuating supply of renewable energies, but their technology is less mature, and they are more expensive than alkaline electrolysers. Their current global market share is just under 31 per cent, with costs ranging from 1,300 to 1,960 euros per kW.26 Europe currently holds an advantage in terms of PEM patents and production. Platinum and iridium are required for production, and their distribution (and potential supply chains) is highly concentrated. South Africa holds the world’s largest reserves of platinum group metals (approximately 91 per cent), including iridium, followed by Russia (about 6 per cent) and Zimbabwe (about 2 per cent).27 In contrast to alkaline electrolysers, the supply of components for PEM electrolysers tends to be concentrated among individual manufacturers in the EU, the US, the UK, and Japan.

Hydrogen from renewable electricity could well lead to the emergence of a new class of exporters along new and more diffuse value chains in comparison to those of fossil fuels; dependencies in such chains will also be more diffuse. Competition for resources may diminish, but competition for components, expertise, and modes of transportation remains relevant.

Pipelines, shipping, and choke points: Geopolitical transport challenges

Large-scale hydrogen transport can in principle take place in gas or liquid form: either through pipelines (in gaseous form) or shipping (either as liquid hydrogen, through Liquid Organic Hydrogen Carriers, or as hydrogen-derived products like ammonia, see again fig. 3).

Most attention is currently given to liquid ammonia shipping and pipeline transport of gaseous hydrogen; this is because both would be able to benefit from existing infrastructure, tested production methods, and established supply chains and markets.

Existing natural gas pipelines can be repurposed for hydrogen, or new pipelines can be constructed. Estimates consider pipeline transport to be a cost-effective solution in the long term for distances of up to 4000 km for new pipelines and up to 8000 km for converted pipelines, provided projects carry sufficient volume.28 Repurposing pipelines for hydrogen depends on a steady decline in demand for natural gas, going hand in hand with the extensive transformation of national and (inter)regional natural gas pipeline networks. New pipelines require not only high initial investment, intense diplomatic effort, and years (or even decades) to complete, but also create path-dependence due to infrastructure rigidity. Moreover, their inherent limitations are not conducive to interregional trade. In the case of onshore pipelines, risks of third-party dependence increase with distance and the number of countries such pipelines cross.

Compared to pipelines, ships could be more competitive, especially over long distances. This mode of transport depends less on network infrastructure, which favours global trade – also as distance has only a moderate effect on transportation costs. Although liquid ammonia is a promising candidate for shipping, its transportation technology is still immature. The crucial factors here are port infrastructure, freighter design, and the processing technology for deriving ammonia from hydrogen and vice versa. Moreover, especially for derivatives like ammonia, investment security and economic viability depend on coordination and integrated network planning between buyer and seller countries29 – measures that tend to solidify long-term interdependency. Ultimately, maritime transport requires complex supply chain risk management, as demonstrated by choke points, global bottlenecks (for example in Suez, Malacca, and Panama), and potential threats to sea routes.

Regional incongruities and geopolitical divergences

Early decisions over technology and transport routes as well as the market setup underline the degree of political competition among potential future hydrogen actors – which results from their diverging preferences.30 In addition to resource availability, meteorological conditions, and existing infrastructure (see again fig. 1), the following subsections outline the respective strategies of these actors as well as broader regional geopolitical contexts.

Europe on the edge: Between wishful thinking and (geopolitical) reality

The EU has positioned itself as the largest demand centre for low-carbon hydrogen, and it aims to take a leading role in establishing a hydrogen market. As the EU’s technological-industrial competition with both the US and China appears to increase, initiatives such as the EU Green Deal, the REPowerEU plan, the Clean Hydrogen Partnership, and the European Hydrogen Bank are intended to accelerate the development of the hydrogen market in the EU.31 The goals are to solidify the EU’s technological and regulatory leadership, help the EU achieve climate neutrality (or establish a post-fossil energy system), and enhance the region’s supply autonomy.32

When the war in Ukraine broke out, the EU set the target of installing electrolysis capacity of over 120 gigawatts (GW) by 2030 for domestic hydrogen production. It aims to produce 10 million tonnes of hydrogen annually. Although the Net-Zero Industry Act of March 2023 also promotes CSS, its focus is on electrolysis powered by renewables.33 Areas in the EU with climates favourable to producing renewable hydrogen through electrolysis are limited, however; current industrial policy and access to resources and technology are moreover insufficient for a rapid scale-up of domestic production. The REPowerEU plan therefore also envisions importing 10 million tonnes of hydrogen to the EU annually, despite differing views among member states. Having ruled out the EU’s eastern neighbourhood — which could build on proximity and existing infrastructure — for security reasons, in the short and medium term, the EU has only a few suitable potential trading partners that can enable a swift ramp-up of hydrogen trade; these are mainly located in North Africa and the Gulf States. (See the subsection on Africa and the Middle East.)

Continental Eurasia in transition: Geopolitical impacts on hydrogen potential and priorities

The current security situation notwithstanding, Russia, Ukraine, and countries in Central Asia offer significant long-term potential for hydrogen production. Proximity to both European and Asian markets could make continental Eurasia a natural swing producer. However, the geopolitical and security environment has significantly shifted priorities and opportunities in the future hydrogen market.

In 2021 Russia’s export plans34 envisioned delivering 2 million tonnes of hydrogen per year by 2035, with the goal of maintaining the country’s leading role as a global energy exporter.35 Now that Europe is no longer a viable market (for security reasons), Russia is focusing on cooperation with India and China, although neither of these countries is currently positioning itself as major demand and import centre. Ukraine for its part could still play an important role in the EU’s hydrogen import plans but is unlikely to become a player in the hydrogen economy until after 2035 at the earliest.

The war in Ukraine has created an opportunity for the countries of Central Asia to position themselves as an alternative to Russia and Ukraine for the European market.36 They are interested in increasing the resilience of their own (carbon-intensive) economies and integrating into “green value chains” of other key players, including China, the EU, the United Arab Emirates (UAE), and Russia. Now that Russia has ceased to be a primary transit country to Europe, westward exports will depend on complex logistics along the intermodal corridor connecting the Caspian Sea to the Black Sea via the Caucasus. Central Asia’s hydrogen future is thus more likely to lie in the Asia-Pacific region, at least in the short and medium term.

Africa and the Middle East: Great opportunities meet great expectations

Oman, Saudi Arabia, and the UAE are probably closest to realising a hydrogen (export) economy.37 In addition to the Arabian Peninsula’s abundant resources (land, sun, wind, natural gas), these states can draw on extensive expertise in energy exports, the petrochemical industry, CO2 management, substantial financing capabilities, and agile decision-making.

The hydrogen economy could potentially stabilise current social and governmental power structures in the long term.

These Gulf States aim to establish a hydrogen export sector that compliments rather than substitutes the oil and gas business. Moreover, they seek to onshore value chains and increase domestic value-adds – for instance, using hydrogen applications (such as green steel). The hydrogen economy could potentially stabilise current social and governmental power structures in the long term and advance the region’s geopolitical ambitions. Potential buyers include Europe and countries in East Asia (especially Korea and Japan). Recent project awards and delegation visits suggest, however, that the scales are currently tipping from Europe towards East Asia.

Regional escalations of the Israeli-Palestinian conflict could potentially affect hydrogen flows to Europe – depending on the port of origin, hydrogen freighters must pass two choke points (see also fig. 1). Such escalations could also affect hydrogen policy in the Levant. To date, Israel sees itself a hydrogen importer, and Jordan considers hydrogen exports via and to the former.

North Africa on the other hand is a hotspot. This is driven by both supply (excellent renewable resources and – in the cases of Algeria and Egypt – natural gas reserves) and demand (EU’s hydrogen plans).38 The region as a whole has an ambivalent relationship with the EU, however. On the one hand, it desires economic integration; on the other it deliberately seeks to display differentiation (e.g., with respect to regulatory requirements for hydrogen). Overall, the region envisions itself as a hydrogen exporter. It gives precedence to economic and political considerations and only marginally associates hydrogen with local climate policy. While Egypt stands out for its geography and infrastructure, financial risks stemming from its debt crisis are a barrier.39 The states of the Maghreb benefit from an existing network of gas pipelines. Morocco, which already collaborates with the EU in different sectors, sees itself as a major exporter of renewable hydrogen to the EU.40 However, diplomatic differences with the EU and recent incidents overshadow this promising potential partnership. Algeria for its part seems less involved in the (renewable) hydrogen transition, both for institutional reasons and due to its focus on the existing gas industry. Further complicating the Maghreb’s emerging hydrogen economy is the ongoing conflict between Morocco and Algeria, which also involves Tunisia and Libya.

South of the Sahara, several countries are considering hydrogen exports mainly for economic reasons and often in response to EU hydrogen diplomacy. Examples include Namibia, Senegal, Nigeria, Kenya, and South Africa.41 With the exception of South Africa and Nigeria, these parties are relatively inexperienced when it comes to energy. They face significant financing and infrastructure constraints, making capacity expansion uncertain and reliant on substantial direct investments. Moreover, these countries are also looking towards East Asia. For example, Namibia’s hydrogen strategy notes that it intends to target export volumes to Japan, South Korea, and China in addition to the EU.42

The Indo-Pacific in flux: Hydrogen politics between global and middle powers

In the vast Indo-Pacific,43 different resource endowments, actor preferences, and energy policy orientations intersect.

China’s hydrogen ambitions are grounded in considerations of energy security and energy independence as well as in its sustainability aspirations and industrial policy. By 2025, the country aims to produce between 0.1 and 0.2 million tonnes of hydrogen annually from renewable energy, which will position it as both a self-sufficient producer and a hub.44 Its strategic competition with the US fuels the race for technological and market leadership. China already leads in the production of alkaline electrolysers, as a refiner of many raw materials, and as a manufacturer of such products as solar panels and, to a lesser extent, wind turbines.

India is also pursuing a protectionist approach to industry and value chains. The country aims for self-sufficiency by 2047 and seeks to export hydrogen and technology in addition to meeting domestic demand.45 It already envisions producing five million metric tonnes of hydrogen annually by 2030, primarily from electrolysis.46 Among the factors complicating India’s ability to meet this target, however, are high capital requirements; competing national priorities; India’s deep trade relations with both the West and China; and its reliance on Russian arms exports.

For their part, Japan and South Korea are focusing their hydrogen efforts to decarbonise their economies, build competitive domestic industries, and establish energy security and strategic autonomy.47 Both see territorial disputes with China as posing a fundamental risk to energy supply, further driving diversification efforts. With limited natural resources (including land), both countries prioritise imports. They plan to import green hydrogen from Oman and blue hydrogen from sources like the UAE and Australia.

Australia meanwhile aims to establish itself as a renewable energy superpower by leveraging its experience in energy exports, current domestic hydrogen production, and access to capital.48 Although trade with the EU would seem to be a logical outcome of strategic partnership, Europe will have to compete for Australian hydrogen exports with (geographically closer) Japan and South Korea.

Australia, Japan, and South Korea meanwhile all have extensive economic ties with China, driven not only by the three countries’ shared interests in regional peace and stability but also by the desire to counteract China’s regional influence. Increasing military-industrial cooperation between these three countries and the US is another factor in the security and geopolitical landscape.

In Southeast Asia – which includes traditional regional exporters of natural gas like Brunei, Indonesia, and Malaysia, as well as long-standing importers like Singapore and Thailand – the implementation of hydrogen ambitions remains limited, with the exception of Singapore.49 While some countries have substantial raw material resources (such as nickel in Indonesia or natural gas in the countries just mentioned), they lack technology, capital, and renewable energy infrastructure. China is of paramount importance to the region, not least because it is making development-oriented investments. However, countries in the region actively suffer from the ongoing systemic conflict, making peace and stability top priorities.

All in and all out: The United States as a strong prosumer alongside emerging exporters in Latin America

In the Americas, the US plays a special role as a potentially influential “prosumer” (both a producer and consumer) in the future hydrogen world.

The US takes a largely agnostic approach to hydrogen technology. Protectionist legislation such as the Inflation Reduction Act (IRA) of 2022 targets the production of both blue hydrogen and green hydrogen (through electrolysis powered by both renewable and nuclear energy).50 The US hydrogen strategy, released this year, envisions domestic production of 10 million tonnes of clean hydrogen annually by 2030, increasing to 50 million tonnes annually by 2050.51 This could not only meet almost the entire long-term domestic demand but also leave room for the US to export to allies.

The US push for clean hydrogen is driven not only by concerns about climate change but also by its systemic rivalry with China.

The US push for clean hydrogen is driven not only by concerns about climate change but also by its systemic rivalry with China. Other motives include the growing industrial-technological competition with both China and Europe (seen as a threat to US technological and economic leadership) and the pursuit of resilience and supply independence in critical raw materials and industrial components.

In Latin America, hydrogen is slowly entering the energy policy spotlight. Potential and interest are not evenly distributed, however. The countries aim for energy independence and decarbonisation through hydrogen development, while also seeking opportunities to export regionally and overseas. Chile and Brazil are prominent examples. Chile in particular stands out thanks to its favourable geographical and climate conditions. Brazil has particularly relevant experience in commodity trading, fossil fuel exports, and a petrochemical industry that already uses conventional hydrogen.

Chile’s production potential is estimated at 160 million tonnes of green hydrogen per year by 2050.52 It already plans to export green hydrogen and derivatives to Japan, South Korea, and Germany. Despite its highly advantageous access to both the Pacific and Atlantic Oceans, however, Chile lacks regulatory frameworks, infrastructure, and electrolyser technologies, which is hindering the initiation of exports. Chile’s export preferences and future trade configurations could well be influenced by its growing dependence on exporting resources to China and accepting Chinese investments in resource extraction and infrastructure. In Brazil, climate ambitions may take a back seat to competing priorities like alleviating poverty. Though the country stresses its willingness to increase cooperation with the EU on energy and climate issues, its position and role within BRICS, as well as its changing geopolitical preferences, might eventually influence the country’s choice of partners.

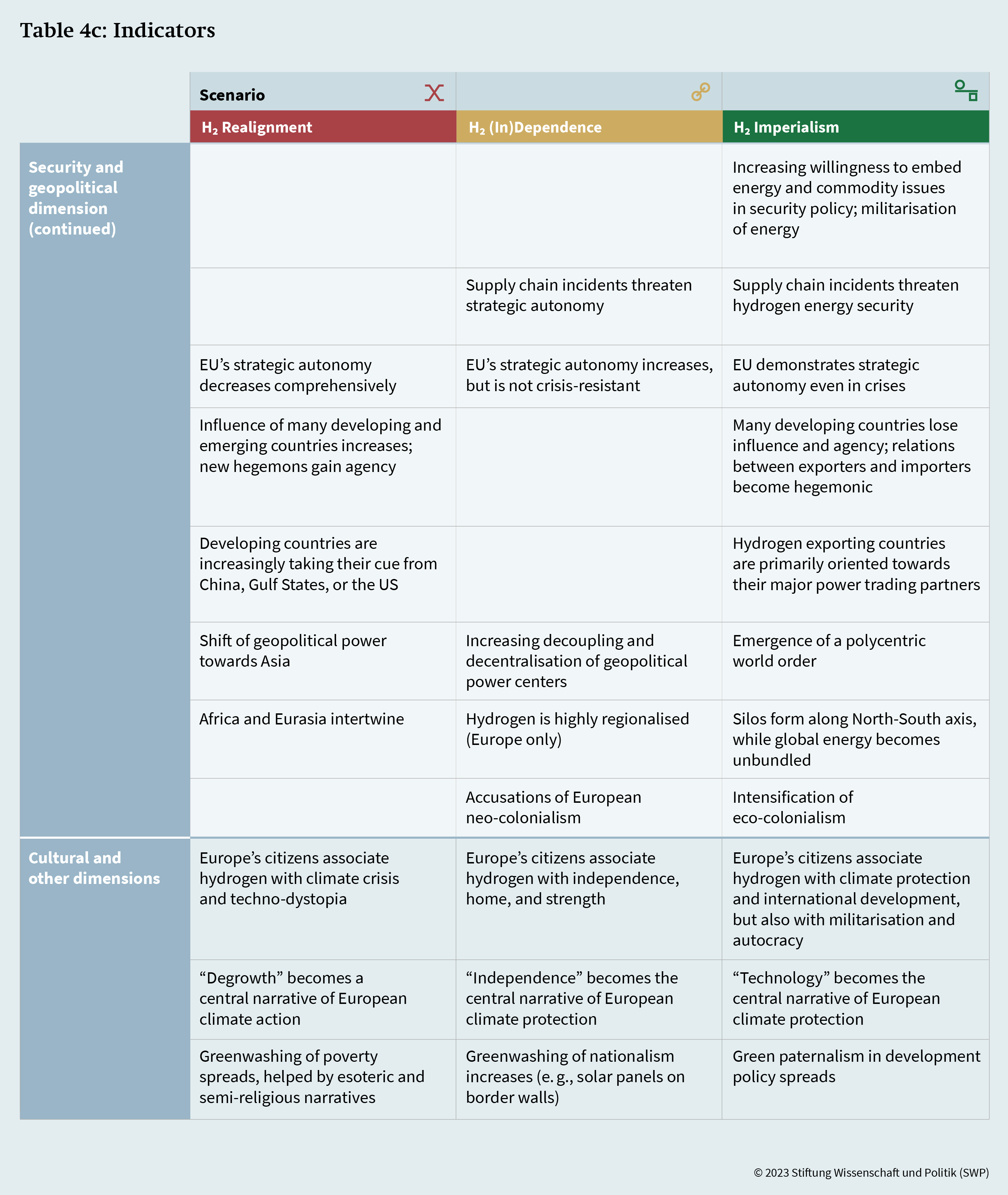

Three scenarios for the geopolitics of hydrogen

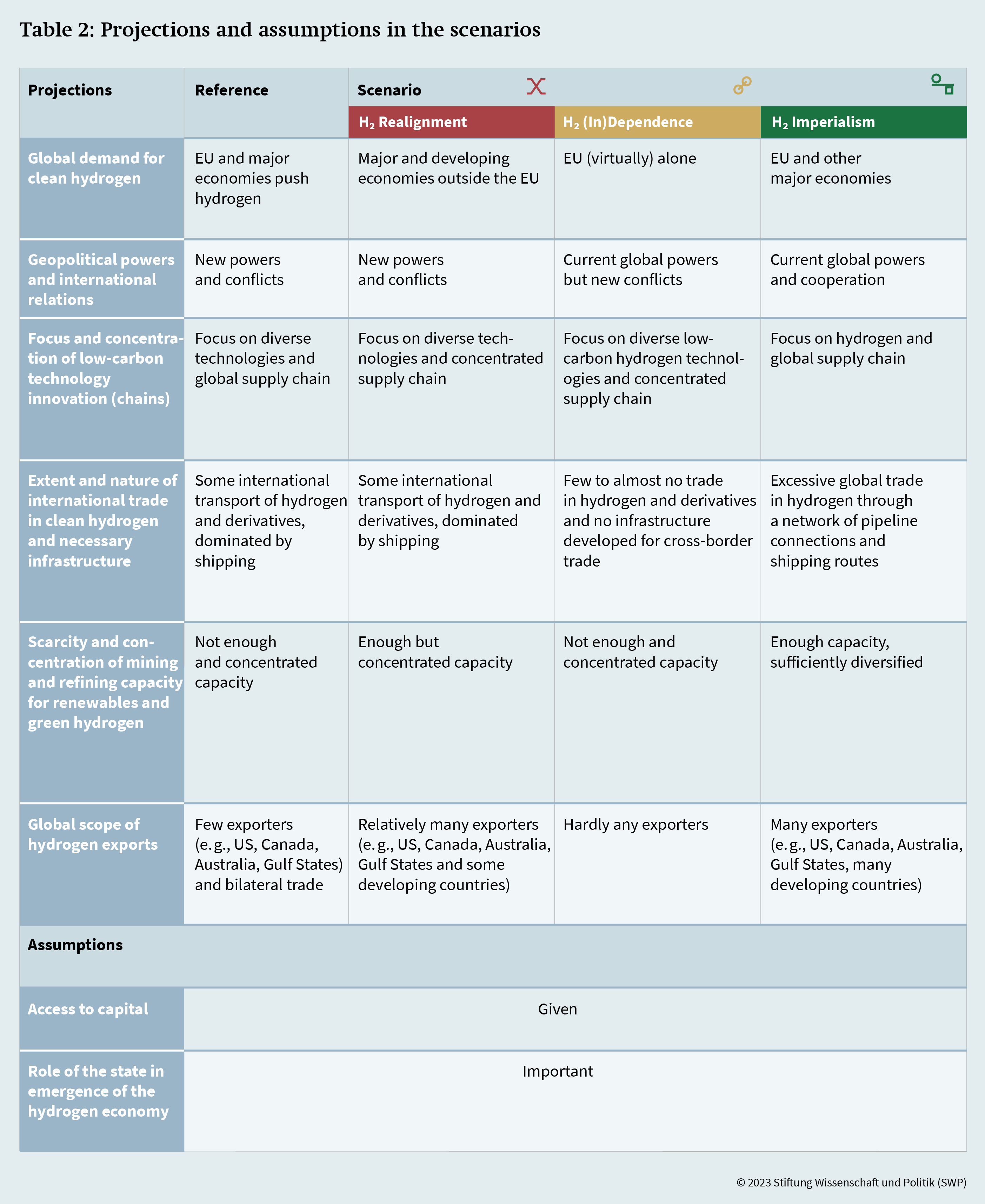

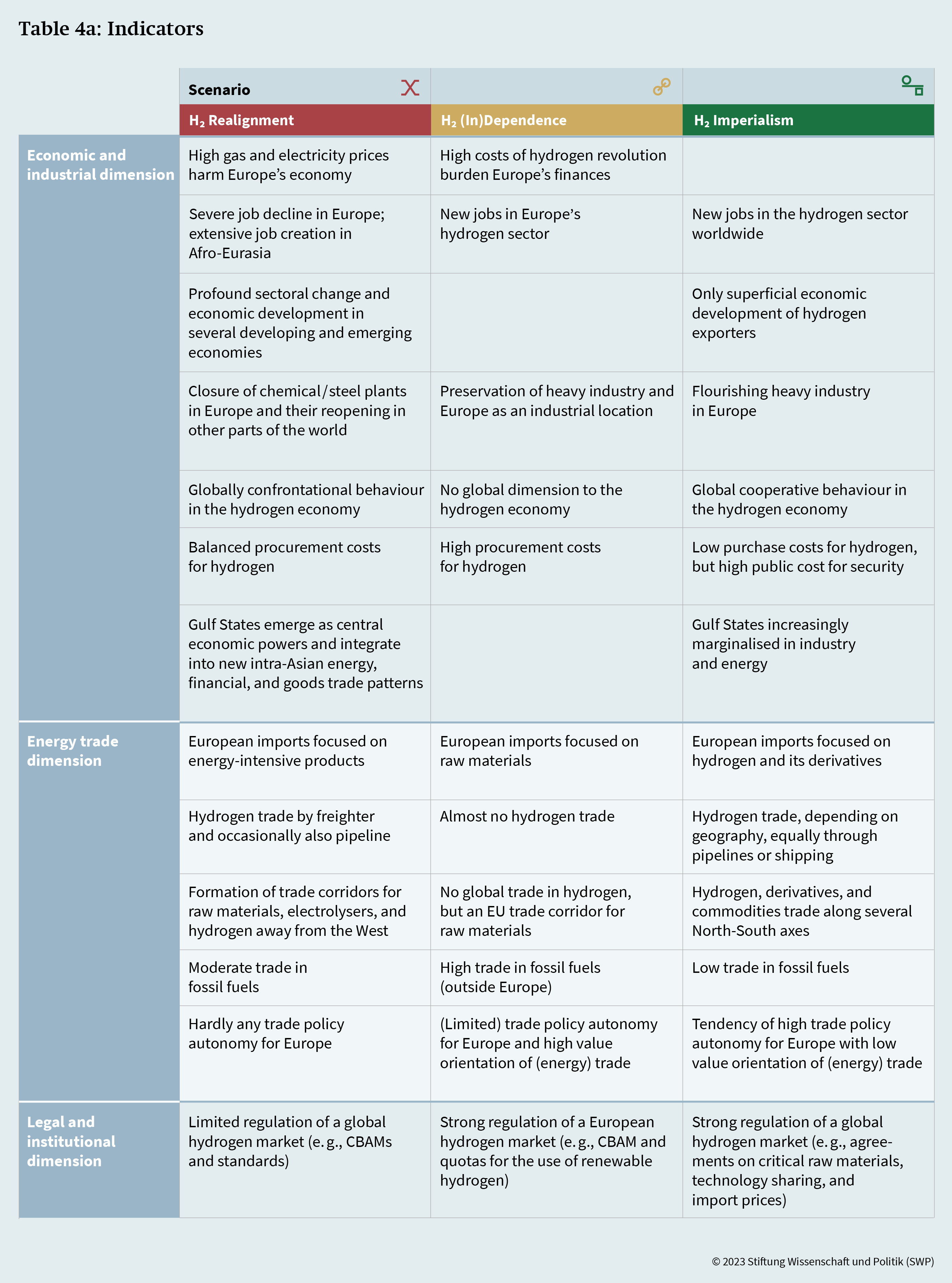

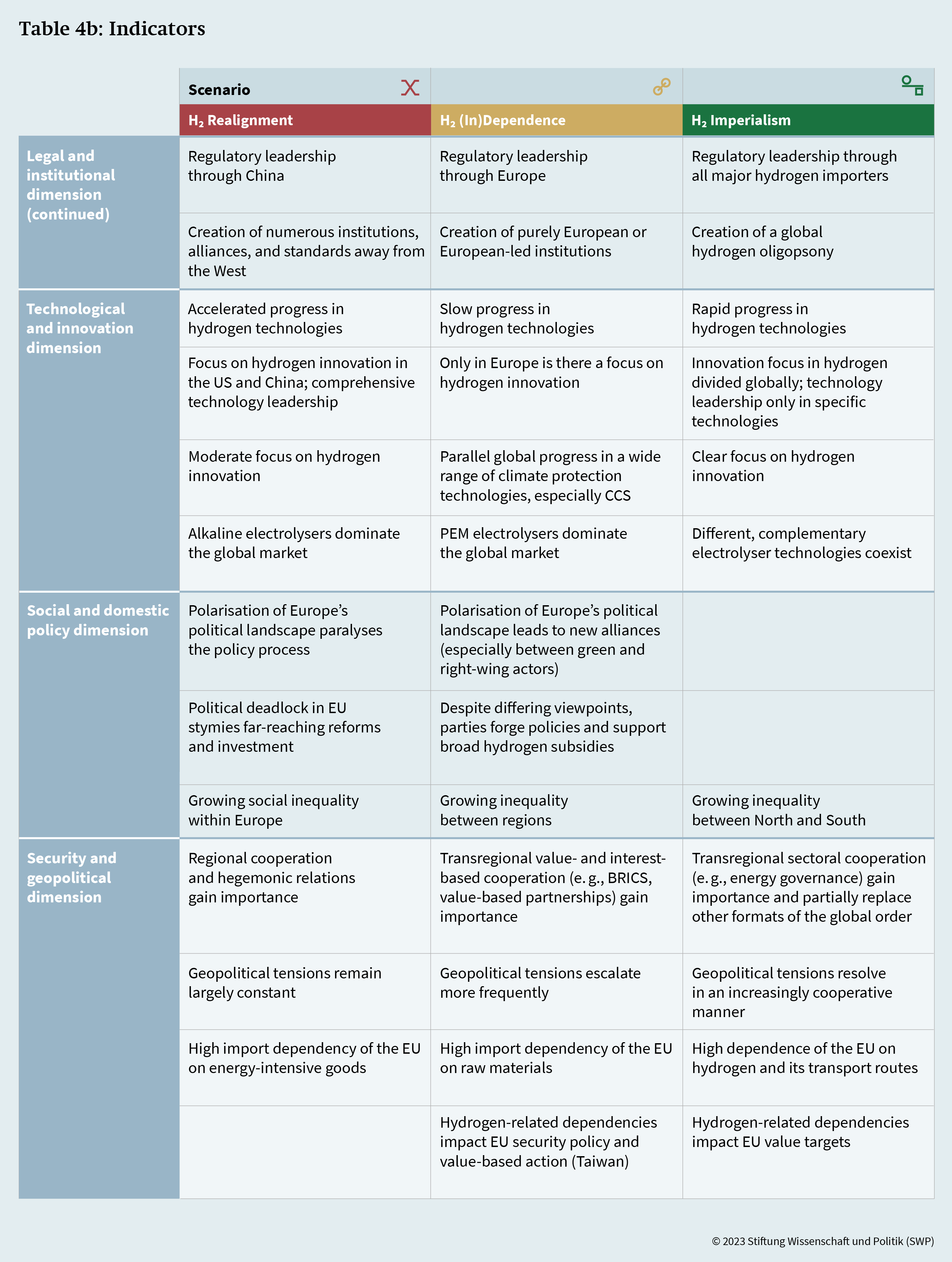

With diverse technologies, intertwined global value chains, and incompatible preferences embedded in geopolitics and path dependence, the emerging hydrogen economy is anything but simple. Here we present three global scenarios for how it will develop up to the year 2040: Hydrogen Realignment, Hydrogen (In)Dependence, and Hydrogen Imperialism (fig. 4). Recounted in the dramatic present tense, they sketch possible developments, risks, and options.

The scenarios were developed during a multi-stage process with the input of an interdisciplinary group of international experts.53 Five motifs guided the scenario development process: raw materials, technological leadership, autonomy, system conflict (especially the US-China rivalry), and global order. The scenarios offer a European but not a Eurocentric perspective by emphasising global dynamics and the diverging preferences of various global actors.54 All three rest on the (significant) assumptions that 1) European and global climate policies will remain high-priority, 2) governments will remain the dominant actors in the hydrogen sector, and 3) global access to capital will remain in effect.

Hydrogen Realignment pictures a world in which the EU’s hydrogen ambitions dissipate, while the hydrogen economy, energy-intensive industries, and the world order shifts towards the East. Hydrogen (In)Dependence envisions a future in which Europe commits to the global hydrogen transition in order to promote its strategic autonomy; its latent dependence on supply chains for raw materials, however, ultimately diminishes its ability to respond to global power shifts. Hydrogen Imperialism presents a dystopian future: a global hydrogen economy in which hegemonic powers divvy up the value chain (and export countries) among themselves, while development projects become a pretext for propping up “hydrogen dictators” and authoritarian client states.

Those three futures explore the breadth of the “cone of uncertainty” (see again fig. 2). They are deliberately not probable but plausible; and by exploring three contrasting narratives, the scenarios allow us to navigate the broad spectrum of possible futures. Together, they encircle a “reference scenario” (rudimentarily sketched in Table 2 of the Appendix) that is the “most likely” future.

We emphasise that the scenarios presented here are deliberately extreme and entirely hypothetical; they do not reflect or extrapolate the current reality of any country. All countries mentioned in these scenarios are used merely to exemplify broadly conceivable developments and should not be interpreted as representing any assessments from us or the SWP. They should not be used as such.

Hydrogen Realignment

Europe on ice

In early 2024, meteorologists confirm that Europe’s current winter will be long and tough. After a period of deceptive calm, electricity and gas prices start to roar; this haunts the economy and feeds the far-right, which vies for political power with a still-strong environmentalist camp. Elections on all levels result in disarray. Political polarisation across the EU and within its member states produces enduring policy deadlock. (Rudimentary policies to shield low-income households are put in place, but political paralysis hinders thorough reform, infrastructure investment, and support for European industry – not least because the EU is still consumed by Russia’s ongoing war in the Ukraine.) Hydrogen remains a large part of the energy debate, but hardly any binding agreements or investment decisions follow. This is because deadlock has spread to institutions, which discourages the private sector from making commitments. EU states continue to grant a narrow majority to those favouring ambitious climate action – in early 2025 the European Commission’s president gives a powerful speech declaring Europe “the green continent” – but there is complete disagreement on how (or even whether) to manage those multiple crises. This stymies support for new technology and industry of all kinds.

This intensifies Europe’s (hitherto weak) deindustrialisation, bringing fundamental changes to Europe’s economy. In 2026, for example, BASF opts to close its biggest plant, in Ludwigshafen, Germany, and drastically scales back operations at its “Verbund site” in Antwerp, Belgium. The EU meanwhile finds itself needing to import more and more energy-intensive products from regions with lower energy prices, and significant sectors of European industry relocate to these places. They include various locations in Asia (where multinationals expand already existing clusters) and the Gulf States (where abundant natural gas and hydrogen meet abundant financial resources for developing prospective new industries). In 2028 – after a two-year delay – the EU finally implements its Carbon Border Adjustment Mechanism (CBAM) in an attempt to stem deindustrialisation. This yields little more than spiking import prices, however, since affordable clean energy allows the (new) industrial hotspots to decarbonise some of their exports to Europe.

Elsewhere, the US has managed (after the 2024 presidential election) to overcome its political stalemate of the early 2020s with a broad compromise that simultaneously supports domestic industry and combats climate change. This new US deal sustains trends initially launched with the IRA and consolidated during ongoing trade rows with China (manifest in an increasingly toothless WTO). Washington’s aggressive new green mercantilism prioritises technological autarky over openness because it sees low-carbon technologies as a prime way of decoupling from China and competing with it. In 2027, the US president proudly announces offshore wind power (“freedom power”) as a core component of its clean and self-reliant future. The US adopts significant financial support schemes and removes most red tape for wind projects in a nationwide movement (“A Strong and Clean America”) that strategically expands to hydrogen. With time, polymer electrolyte membrane (PEM) electrolysers become a top US industry.

Building on its hydrogen ambitions of the early 2020s, China decides in 2024 to ramp up its hydrogen ambitions.

While most US-made PEM electrolysers target the domestic market and selected outlets (such as Canada, Chile, Australia, and Brazil), Chinese alkaline electrolysers dominate the rest of the globe. Building on its hydrogen ambitions of the early 2020s, China decides in 2024 to ramp up its hydrogen ambitions. The holistic technology ecosystem it strives for rests on three pillars: 1) control over its own energy sector; 2) a prosperous emerging export industry with geopolitical leverage; 3) and the ability to quickly dominate the global climate agenda. China throws its weight behind hydrogen-affiliated technologies, especially alkaline electrolysers, which appear to be more efficient for large-scale applications and easier to scale up than PEMs. For its part, the US government is relying on targeted innovation funding, the presence on its soil of former European PEM champions (manufacturers who relocated to the US when it became clear that the EU’s own hydrogen transformation had stalled), and a freshly brokered exclusive US-South African partnership for necessary raw material supply chains. By 2028, however, Chinese manufacturers have managed to drive prices below 100 US dollars per kW in 2028. China’s growing hydrogen market push gains even more momentum with the influx of ex-EU energy-intensive industries into China. This motivates the Communist Party to formally adopt the dual policy of net-zero industrial leadership in 2029. And it builds significantly on China’s domestic use of hydrogen – also in reaction to the EU’s CBAM tariff system.

The age of the dragon

As the US and Europe become more introverted, global power shifts towards the Indo-Pacific accelerate a transition that began in the early 21st century. A Gulf-China axis now becomes the region’s most significant trade and power corridor. Not only do the Gulf States share with China a pragmatic approach to politics, but both actors are zealous about expanding their (geo-)economic reach. In addition to (informal) multilateral agreements that govern how these nations distribute their ever-growing presence in East Africa and the Middle East, in 2028 China and the Gulf States form an accord on the preferential supply of Chinese electrolysers in exchange for hydrogen, minerals, and petrochemicals. The Gulf has become an emerging hub for services, raw materials, and heavy industry – alongside its continued (albeit slightly lower) hydrocarbon exports to the Indo-Pacific region. Notably, in 2031, Saudi Arabia inaugurates the world’s largest “green steel” facility in Neom, which is powered by green hydrogen initially earmarked for EU export. Similarly, a broad industry-research consortium of Omani and UAE actors announces that their two countries have successfully developed the ports of Jabal Ali and Duqm into the world’s most influential hubs for clean marine fuel.

Meanwhile in East Asia, in 2030, Japan and Korea introduce a structure similar resembling the EU’s CBAM to push decarbonisation. While they manage to maintain most of their domestic industries, they begin to draw hydrogen supplies (or LNG to be converted to hydrogen) from the Gulf, Australia, and closer neighbours such as Thailand and Chile.

China’s trade corridor with Africa has gained importance, with China trading infrastructural support (including energy) for raw materials from the continent. These are needed for a range of elements like batteries in China’s low-carbon tech sector. In 2031, the African Union and China finally inaugurate the China-Africa Cooperation Organisation. Within two years, the hundredth country signs on to China’s Dragon Accord. Signatories benefit from cheap electrolysers financed with affordable Chinese loans, while (partially) subscribing to China’s regulatory framework for hydrogen; poorer parties to the accord in particular expect Chinese infrastructure investment and deepening trade relations in return. Such investments enable Kenya and Tanzania for instance to leapfrog straight to hydrogen for their industrialisation and then benefit from selling both hydrogen to China and green industrial products to the EU. Meanwhile, Southeast Asian nations, by producing hydrogen domestically, gain the ability to substitute some of their oil and gas deliveries from the Gulf; the latter has developed into the second-largest supplier to the EU of goods, including not only raw materials but also steel and even cars.

Russia for its part, whose relationship with China is built on cautious pragmatism, has also become a supplier of critical mineral resources like nickel for China’s new industries. Its broader economic ties with China have not however compensated for its continued isolation from the West. Moscow’s attempts to create an integrated energy market and foster a Eurasian Hydrogen Union fails to attract Central Asia. Vladimir Putin’s exit from office in 2032 (for health reasons) furthermore increases political instability and economic stagnation, which extends to the region. But this ultimately only deepens Russia’s ties to the Gulf States and China. Both players have invested significantly in Central Asia to acquire an aspiring new target market (and tourism destination), gain critical raw materials, and expand their reach into a region they believe to be more relevant as new power dynamics unfold. Two years later, Russia, Kazakhstan, and Uzbekistan sign on to China’s “Low-Carbon Hydrogen Standards” and begin to provide additional supply bases for critical mineral resources and energy production.

Ultimately, in 2034, China concludes the “Hydrogen and Raw Minerals Alliance” with Indonesia, the Philippines, and Australia as part of enhanced regional trade agreements. Within this new, transregional global order, China’s influence in Europe and the US has diminished considerably. Both are less dependent on Chinese goods than they were in 2023 – except that the EU still relies on Chinese solar panels as well as some other energy-intensive imports. In 2036, the Chinese mining and chemical giant Sinopec buys BASF and Norilsk Nickel. A year later Sinopec rebrands as SinoHy after producing 500 GW of electrolysers for international markets.

Throughout this time, India has pursued a more agnostic approach to climate issues, balancing carbon-intensive growth with clean tech. Some first hydrogen applications exist, but India is more of a cautious “fast follower” – hence not (yet) a major player in this geoeconomic landscape. It is not willing to enter into deeper agreements with China (or the US) but instead keeps a certain distance from all but the GCC countries. By 2035, India and its immediate neighbours have long since outpaced China as the primary importer of oil and gas from the Gulf. (India’s relations with the GCC, though imbalanced, have deepened substantially after major Gulf investments in India combined with a codification of the “right-to-stay” for Indian expats in the UAE, Qatar, and Saudi Arabia.) An Indian-Russian oil and gas pipeline is still on the table, but GCC influence in the region has kept it at bay. The use of pipelines for the transport of hydrogen is rare, with shipping – mostly methanol and ammonia – dominating the sector.

In 2040, hydrogen accounts for more than 25 per cent of China’s energy mix; other East Asian nations also have large shares of hydrogen in their systems. In addition to Chinese aviation and shipping, where hydrogen is becoming the standard, Chinese research is giving new momentum to hydrogen-powered vehicles, especially trucks. (Passenger cars and other small vehicles are by now mainly electric.) China’s leadership in clean technology – indeed, China sets the technological standards everywhere but Europe and the US – allows it to expand its reach far beyond its borders, making it the de facto arbiter of all disagreements in the eastern hemisphere.

The GCC has an implicit power sharing agreement with China and exercises hegemony from Pakistan to Libya.

The GCC – now a source of energy exports, manufacturing, and the world’s highest paying services industry – has an implicit power sharing agreement with China and exercises hegemony from Pakistan to Libya. Türkiye and parts of Europe are increasingly coming under its sway as well. The latter continues to host a carbon-free services industry, but its overall economic power has contracted by nearly 20 per cent since 2024 (especially after the financial industry followed Europe’s manufacturing sector in moving abroad). Even major research institutions have relocated eastwards, with universities from China, India, and the Gulf together accounting for 14 of the world’s 20 top-ranked schools in the QS World University Rankings. Only Europe’s tourism sector continues to thrive and has grown over the past decade, driven by demand within the expanding middle class in China and the Middle East.

There is a silver lining to the EU’s economic and geopolitical weakening, however: in December 2040, as the continent’s first facilities for direct air capture of carbon dioxide go online, the president of the European Commission announces that the EU has managed to reach its net-zero goal, 10 years ahead of target.

Hydrogen (In)Dependence

Fortress Europe

In 2024, a wave of droughts and storms sweeps Europe, inflicting more than 20 billion euros in economic damages and causing substantial loss of life. One such event is the flooding of villages along the river Danube in northern Austria, a catastrophe, in which nearly 3,500 people die, and the industrial port of Linz is destroyed. From this point on, no political party can afford to downplay climate change. But the war in Ukraine is still raging, and Russian troops are en route to Kiev; refugees to the EU receive a cooler welcome than in previous years. Across Europe, security, autonomy, and nationalist sentiment are cemented as major themes.

The resulting landscape pushes green nationalism and political bargains that demand both a “strong Europe” and decisive climate action.

These supposedly conflicting trends fuel support for both green and right-wing parties in 2024’s EU parliamentary and member state elections. The resulting landscape pushes green nationalism and political bargains that demand both a “strong Europe” and decisive climate action. Analysts point out what this will mean in the years to come: curbing migration; strategizing trade; and relying on homegrown renewable energy, with hydrogen the king. The clean gas emerges as the smallest common denominator – as something on which both greens and nationalists can agree, provided it is sourced within Europe.

Across the Atlantic, the 2024 US presidential elections bring a Republican hard-liner to power, yet another voice calling for “America First”. The president works to decouple the US from China and pushes mercantilist policies. The global (economic) order starts to erode at a faster pace, and trust in global governance and cooperation wanes broadly and quickly. In a push for “friendshoring” — i.e., focussing trade on (presumed) allies — the US begins to negotiate a free trade agreement with the EU, but this is stymied by bickering over the US approach to climate issues, its industrial investments, and the EU’s focus on (energy) sovereignty (even at the expense of US LNG and hydrogen).

By 2025, it is apparent that “Fortress Europe” has become operational. In addition to new agreements with Morocco, Tunisia, Libya, and Türkiye to secure Europe’s borders through policing and refugee internment camps, the EU agenda seeks to disassociate itself from any “undesired” (i.e., non-Western or democratic) trade partners. It also pushes energy from hydrogen and renewables. The EU streamlines the permitting process for renewable energy and passes strategic regulations on hydrogen, including the launch of the European Hydrogen Union. It aims to facilitate domestic hydrogen production and make European industry “H2-ready.” The EU does not officially outlaw hydrogen imports, but its Hydrogen Union features CBAM along with draconic non-tariff barriers, which effectively make hydrogen exports to the EU (deemed hostile to energy self-sufficiency) uncompetitive. The European Commission commits to its electrolyser industry with broad support policies, including an innovation fund and direct subsidies. Action focusses almost entirely on PEM electrolysers (with some research grants for less mature technologies as well), since the Commission considers the battle for alkaline electrolysers lost. The necessary raw materials are sourced from democratic South Africa. By now, the US and Canada have both banned exports of their own supplies of platinum group metals; this makes South Africa the EU’s only significant choice, but the EU deems it a “safe” trading partner. In 2026, the European Commission proudly announces the Democracy Trade Channel, a formalised agreement giving it preferential access to (and guaranteed purchase of) platinum group metals and other critical raw materials from South Africa. EU decision-makers hope to extend the agreement to other (democratic) countries later, creating a secure trade union among allies.

Elsewhere, the momentum for hydrogen seems to have largely dissipated. The year 2026 finds Korea and Japan still running a few pilot projects they had commissioned earlier in the Gulf States, but there are virtually no new initiatives. Decision-makers in the Asia-Pacific region and elsewhere consider hydrogen to be impractical: expensive to produce and complicated to transport or handle. (Fresh research on the direct use of ammonia as an energy carrier yields dismal results.) China’s electrolyser industry continues to grow, albeit at a slower pace and without industrial policy support for any significant scaling up. Instead, investment in clean technologies diversifies. In 2027, Japan, Korea, China, Singapore, and the GCC states found the “Global Carbon Alliance” to bundle and fast-track research and development in CC(U)S technology, which numerous countries increasingly consider “the way forward”. In this context, hydrogen is eventually used, but in the form of LNG that is converted locally, for instance in Singapore and Japan. In the US, too, natural gas is the main answer to climate concerns; a renewed commitment to the domestic oil and gas industry bridges the national political divide, along with a moratorium on phasing out coal.

False friends

In spite (or because) of these developments, the EU reinforces its lonely commitment to hydrogen. By 2028, the first large-scale electrolysers in Spain are operational and supply local industry clusters; 25,000 km of the “Hydrogen Backbone” are completed. That same year the European Hydrogen Bank is finally established and receives the first tranche of 3 billion euros to finance “Cost of Difference Schemes” to establish lead markets around steel and petrochemicals. The EU announces a plan to implement in steps a renewable hydrogen use quota in steel and chemical industries and to reach 80 per cent by 2038. Investments (mostly private) into hydrogen transport infrastructure increase, and hydrogen clusters also develop in northwest Europe.

The fast-tracked transition is entirely domestic. It targets self-reliance but hungers for foreign solar panels (the EU had briefly invested in reviving its domestic PV industry, but the project was ultimately deemed too expensive, and tensions with China were considered sufficiently “balanced”) and critical raw materials. It particularly needs electrolysers, the manufacturing of which becomes the lynchpin of the EU’s industrial policy.

Meanwhile in South Africa, the country’s political system has been fairly stable since the mid 2020s. Smaller regional parties have settled within the country’s political landscape, and the “experiment” of coalition governments did an unexpectedly good job enriching, stabilising, and reviving the country’s democracy. Even while it maintains positive relations with Europe, however, South Africa’s government is increasingly seeing its role within BRICS, which is becoming increasingly institutionalised; that said, it still retains flexible forms of collaboration. While the idea of a common BRICS currency never materialised, in 2027 the bloc founded its own payment infrastructure (as an alternative to the US-backed SWIFT) in cooperation with the Eurasian Economic Union. The BRICS summit has evolved into a semi-institutionalised cooperation body that is widely considered a crucial power beyond the West and a de-facto element of global governance in a fragmented order.

By 2032, clashes in Ukraine have for years been levelling off, although major parts of the country are occupied by Russia. The EU sticks to its stance of “interference without confrontation” by integrating Ukraine economically and militarily. (Along with Türkiye and the UK, Ukraine is now part of the European Hydrogen Alliance and supplies hydrogen from its nuclear power plants to the European grid.) The cornerstone of the EU’s activity is a vast air defence shield set to be installed in 2034 in non-occupied areas of Ukraine. In reaction, Russia proposes a BRICS “Customs and Security Union” (CSU) that builds on existing economic ties and military relations between some of the countries. In China in particular, the idea finds resonance for its political value.

South Africa is only peripherally interested in trade with Russia, but existing security ties between the two countries are long-standing and valued by the ANC. The proposal also fits with quiet but growing anti-EU sentiment within South African society; the EU’s Democracy Trade Channel’s strict regulations (especially its high social and environmental standards) have increased the cost of mining, leading companies to replace workers with machines; this in turn fuels the narrative of “white European neocolonialism”. Meanwhile, demand for South African platinum group metals continues to grow both inside and outside BRICS, which clashes with South Africa’s previous policy of giving preferential access to the EU. As a result, the ANC-led government – and indeed society as a whole – begins to distance itself from Europe in order to exercise more power (and enjoy renewed loyalty) within BRICS. In 2034, China, Russia, Brazil, and South Africa sign the framework agreement. (India, demonstrating autonomy from China, chooses not to join and instead deepens its partnership with the US.) In this new geopolitical configuration, plans for South African mining projects designed for EU export are put on hold. The government makes further extraction rights indirectly but unequivocally conditional on the EU dropping its aforementioned plans for an air defence system over parts of Ukraine.

These developments roil an EU energy and trade doctrine that had previously sought to evade exactly such situations.

These developments roil an EU energy and trade doctrine that had previously sought to evade exactly such situations. A cut-off from critical South African materials would certainly cripple EU green industry, most notably electrolyser manufacturing. While the EU is undoubtedly committed to protecting Ukraine, worries about halting the energy transition – or sliding into energy shortages – gain the upper hand. The EU drops its plans for the missile shield. Once again European authorities scramble to diversify, but the stakes have been raised. Major parts of European industry have already switched over (or are in the process of switching) to hydrogen, and no other producers can come to the EU’s aid. Efforts such as repurposing gas pipelines from North Africa or building domestic CCS facilities for producing hydrogen from natural gas are launched, but it will be years before they are finished.

Building on these experiences, in 2037, China seizes the opportunity and seeks to annex Taiwan by military force. The EU faces a dilemma: accept China’s actions or risk economic and military escalation with the entire CSU (that most BRICS members had signed a few years before). In only a few short years, this union has become a counterweight to NATO. The US, whose administration had already significantly reduced trade with China in the 2020s, condemns the aggression against Taiwan, breaks off diplomatic relations with China, and urges Europe to join it in taking decisive action. However, the EU ultimately chooses to be only “deeply concerned” about the situation. Not only is the military risk too great; the EU’s dependence on solar panels and raw materials from the CSU countries is too deep. Other regional powers, such as the Gulf States, Chile, and rapidly industrialising Kenya officially stay neutral, but their sympathies have long been closer with the BRICS than with the EU.

In 2040, a newly built CCS facility in Norway and a repurposed Maghreb–Europe pipeline feed hydrogen from natural gas into the by-now completed Hydrogen Backbone. Europe breathes a sigh of relief, but it also faces a permanently altered landscape. Its desire to use hydrogen to decrease other forms of energy dependence put the continent at the mercy of outside suppliers of material and equipment; this merely shifted dependence and geopolitical complexities. At the same time, Europe has cut its emissions significantly without losing many of its industries. As its long-time approach of overregulating technologies, standards, and trade routes collapses – and as the first supply of “blue” hydrogen arrives from North Africa – new geopolitical challenges as well as new opportunities emerge.

Hydrogen Imperialism

Harder, better, faster, stronger

2024’s COP29 concludes with powerful momentum: the EU, the US, Japan, South Korea, and China agree to mandate that most energy-intensive industries achieve (almost) net-zero emissions by 2033. All signatories see hydrogen as key to this transformation. Four parallel developments lead up to this milestone. First, weather extremes – a staccato of wildfires, droughts, floods, cold snaps, and heat-waves – had again pummelled the globe, making climate change a dominant theme in nearly all the major economies. Second, the G7 reaffirmed at its summit in Italy the commitment to decrease dependence on China; at the same time it commits to rebuilding constructive relations with Beijing to prevent a new Cold War. By now the countries of the G7 view hydrogen with a certain ambivalence: on one hand it supports global collaboration (because it requires it); on the other it could be the key to one country or region’s sustained industrial dominance. Third, political efforts notwithstanding, the global geopolitical divide has deepened further. (The lack of reaction to Russia’s ongoing invasion of Ukraine has shown Europe how much its position, diplomatic ties, and leverage have eroded over the years.) The fourth development is that peaking energy prices and the aftermath of Covid-19 have led to a mild yet noticeable global recession; meaning that economic slowdown requires fiscal stimuli, while budgets still allow for this.

Therefore, signatory countries to COP29’s hydrogen milestone want three things from the hydrogen transition: that it happen as fast as possible; that it build bridges while allowing each country to demonstrate autonomy; and that it boost their respective economies (meaning that the price tag hardly matters). Looking at previous green stimulus packages like the IRA in the US and the European Green Deal, governments now begin putting forward comprehensive support packages to advance their own hydrogen economies. They grant vast financial support to mandated key industries – to incentivise offtake and make them “H2-ready” by 2033. And they set up massive financing mechanisms to push research and development in hydrogen and scale up its production and transport.

Following the geopolitical doctrine of balancing collaboration with autonomy, countries set out on diverse innovation pathways.

Following the geopolitical doctrine of balancing collaboration with autonomy, countries set out on diverse innovation pathways. Hydrogen players begin to specialise in individual niches along the value chain that will make them indispensable; this leads to quick advances in development and production as well as significant cost reductions in each individual technology. Japan and Korea expand their focus on freighters for hydrogen derivatives and start supplying shipping companies in 2027. In addition to manufacturing pipelines and PEM electrolysers, the EU focusses on hydrogen-powered trains and airplanes and successfully demonstrates the first hydrogen-powered transatlantic flight in 2029. Boeing in the US has similar ambitions; the US also makes advances in end-use products and methane pyrolysis. China for its part engages primarily with alkaline electrolysers with solar and fuel cell technology and develops novel applications in the private sector as well as in heavy transport. The GCC countries continue their advances in CC(U)S technology, but their stake in hydrogen is fading, apart from straight export. (Because they did sign the milestone COP29 agreement, signatory governments now tend to keep them out of the loop.) The globalised hydrogen value chain that results from this overall process has no single hydrogen technology leader; rather it is characterised by “distributed leadership”. By 2030, with no one country able to dominate hydrogen geoeconomically, the global order is stable for the moment.

This is not to say that the geopolitical climate is not tense, however. Quarrels surrounding patents and alleged abuses of market power erupt frequently. Imports are an even more obvious locus of rivalry. By now, all signatory countries to the COP29 milestone have realised that their plans require a substantial share of imported hydrogen, and most governments actually care very little about what “colour” that hydrogen has. Throughout the 2020s, importers expand into key regions: Japan and South Korea deepen their ties with the GCC (which continues to provide fossil fuels to the hungry markets of India and developing Asia); the US, taking its first imports from Latin America, prepares for a future spike in demand for hydrogen that it is not willing to supply on its own; China piggybacks on its existing relations with East Africa and Central Asia to set up its own hydrogen imports; and the EU invests heavily in North Africa. But tensions are already growing by 2030. For instance, when Japan and Korea approach Kenya and Chile respectively in order to diversify import sources, trade rows flare up with both the US and China.