The Euro in a World of Dollar Dominance

Between Strategic Autonomy and Structural Weakness

SWP Research Paper 2024/RP 02, 05.02.2024, 30 Seitendoi:10.18449/2024RP02

ForschungsgebieteDr Paweł Tokarski is a Senior Associate in the EU / Europe Research Division at SWP.

-

The inquiry into the global significance of the euro, which is the second most important currency in the international financial system after the US dollar (hereinafter, the dollar), should be treated as a priority in efforts to strengthen the EU’s strategic autonomy.

-

The main obstacles impeding the further internationalisation of the euro include the lack of a sovereign behind it and the heterogeneity and structural problems of the euro area member states.

-

The international status of the euro can be actively improved by strengthening its role in the green transformation as well as in the further deepening and integration of the financial markets in Europe – and by promoting the “digital euro” project.

-

The current trends of growing geopolitical rivalry, digitalisation, and the rise of platform companies in the global economy will steer the international financial system towards greater regionalisation.

Table of contents

2 The Euro in the Global Financial System

2.1 Factors favouring the internationalisation of a currency

2.2 The current international status of the euro

2.2.1 The euro as a reserve currency

2.2.2 The euro in the international debt markets

2.2.3 The euro in trade invoicing, on the foreign exchange market and in SWIFT payment transactions

2.2.4 Other indicators of internationalisation

3 Benefits, Costs and Risks of the Internationalisation of the Euro

4 Obstacles to the Internationalisation of the Euro Currency

4.1 The heterogeneity of the euro area

4.2 Structural problems of the eurozone member states and lack of convergence

4.3 The incomplete character of the monetary union

4.4 Political diversity and lack of statehood

5.3 The euro as a currency of green change

6 Outlook: The Euro and the Development of the International Monetary System of the Future

6.1 The future role of the dollar in the international monetary system

Issues and Recommendations

In the debate on strengthening the EU’s strategic autonomy, the question of how to give the euro more weight internationally cannot be ignored. Although the euro area is often seen in isolation from the EU as a whole, under the Treaties of the EU the euro is the currency of the entire European Union and is thus inextricably linked to the EU’s internal market. Moreover, monetary integration is one of the few areas where the EU has already managed to achieve a high degree of strategic autonomy.

The discussion on upgrading the role of the euro on the global stage is all the more necessary because the international financial system is currently undergoing dynamic changes attributable not only to the growing geopolitical rivalry between the USA and China but also to the acceleration of the digitalisation process, which will significantly impact the functioning of the international financial system in the future.

The aim of this study is to highlight the opportunities and constraints associated with the increasing internationalisation of the euro. The analysis is based on four research questions. First, what are the main factors favouring the international use of a currency and where does the euro currently stand in this respect compared to the dollar and other currencies in the international financial system? Second, what are the advantages and disadvantages of internationalising a currency? Third, what are the main obstacles impeding the further internationalisation of the euro? Fourth, how can the international use of the single currency be stimulated in light of these obstacles?

In the course of this analysis, the study arrives at the following findings:

-

The economic and political dimensions of European integration would benefit from an increase in the international relevance of the euro. Strengthening the significance of the single currency should be actively promoted – even if it comes with risks, including the increased necessity to stabilise the currency environment.

-

The main obstacle hindering an increase in the euro’s weight in the international financial system is the economic heterogeneity of the euro area countries and the lack of a sovereign behind the common currency. This heterogeneity inhibits economic integration, for example, in financial markets, which are crucial avenues for the international use of the currency. It is also exacerbated by diverging economic and political interests that complicate the stabilisation of the common currency, make economic and monetary union reforms challenging and hamper political integration.

-

Strengthening the international standing of the euro is a long-term process, the success of which depends not only on the stability of the common currency, but also on the fiscal stability and sustainability of the economic policies of all eurozone member states.

-

Equally important is the willingness of further deepening integration in the single market, because there is a symbiosis between this factor and the euro itself: European financial markets must be more harmonised and have their own financial infrastructure that is independent of companies outside the EU. The project seeking to introduce the digital euro could make an important contribution here. Moreover, the deepening of the financial markets would be a step towards financing a green transformation, which, if successful, will increase the international relevance of the euro.

-

Despite the problems the USA is facing domestically due to its fiscal policy framework and increasing political polarisation, the dollar is unlikely to lose its dominant position in the international monetary system in the near future. Nevertheless, increasing regionalisation in the global economy will gradually weaken the global dominance of the dollar.

-

Research on the development of the international monetary system should not only focus on state actors. For instance, given the increasing importance of platform companies in the global economy, it is necessary to analyse the consequences of their digital currency creation projects as well.

The Euro in the Global Financial System

The link between the role of currencies in the global financial system and the power of state actors has been one of the most debated topics in political economy for many years. Research in this area has essentially focused on the factors that influence the gain and loss of status of international currencies in the context of geopolitical rivalry or hegemony.1 The two key concepts here are monetary power, which is a component of economic power, and monetary statecraft whose elements include maintaining monetary autonomy, having the ability to manipulate the exchange rate, and promoting the use of one’s own currency beyond the issuer’s borders.2

Monetary integration within the EU and the creation of the euro currency lacked the statehood factor, with geopolitical considerations not the primary motive. Rather, it was to ensure the stability of an increasingly integrated single market, and to avoid future negotiations on exchange rates that would give Germany a politically dominant position. The emergence of potential competition from the euro against the dollar was seen by the European Commission as a positive side effect of the EMU project.3 However, after the introduction of the euro, its prominent position in the international monetary system and the negative aspects of the prevailing dominance of the dollar have led to a debate among economists on whether the international use of the euro should be actively promoted and if so how.4

Today, the single currency plays an important role worldwide. However, current debates on the strategic autonomy of the EU lack reference to the fact that an increased international role for the euro could strengthen these aspirations. This is all the more important as international financial relations have gained a new dynamic in the wake of geopolitical and technological changes that may challenge the international status of the single currency in the future.

Factors favouring the internationalisation of a currency

The starting point from which to analyse the international standing of a given currency is to identify the factors that determine whether it is used widely abroad and to determine the associated benefits and risks associated. The most important of these factors are summarised in Table 1.

Some of these determinants are interrelated. This is true, for example, of the strength and size of an economy, which usually correlates with the reserve currency status of the currency used in it, and with the liquidity and depth of the financial markets operating there. A large, efficient and deep financial market in the issuer’s location is widely considered to be crucial for the international use of a currency.5 Not all of these factors are always fulfilled at the same time, as shown by the example of Switzerland, whose currency enjoys international status despite being based on a relatively small economy.6

The dollar fulfils far more prerequisites for an international currency than the euro, which has a number of weaknesses, especially in terms of the depth and liquidity of its financial markets. The diversity of the euro area member states’ economies, as well as their political and legal systems, and the differences in their economic performance are also of great importance, as analysed later in this study (see chapter “Obstacles to the Internationalisation of the Euro Currency”, p. 17). The potential structural problems of an economic area also affect its future solvency.

The determinants of the international role of a currency are quantitative and qualitative by nature. However, some of these factors are difficult to assess or rank objectively. The hardest to rank are subjective variables such as confidence in a currency, which, for example, leads states to peg their monetary unit to that of another or even to adopt a foreign currency. Similarly incalculable is the factor of market habit, namely the degree to which institutions and market participants become accustomed to using certain currencies or buying certain assets pegged to them.

A lack of military power does not preclude the internationalisation of a currency.

The literature on monetary state power also refers to the importance of the military factor in the spread of a currency.7 The strength of a currency and the depth of the financial markets in which it is based, enable the mobilisation of capital to achieve political goals by military means.8 Military strength and alliance relations in turn influence asset allocation choices. Looking at foreign states’ holdings of US assets, almost three-quarters of them are in the hands of states that cooperate militarily with the USA in some way or another. Of these, about 50 to 60 per cent belong to countries that are “geopolitically aligned” to the USA.9 With increasing geopolitical polarisation, the importance of this factor could increase. Although Europe has considerable military strength, it is highly dependent on the military and technological potential of the USA. However, a lack of military power does not preclude the internationalisation of a currency. The examples of China and Switzerland show that military strength is not the most important variable for determining confidence in a currency.10

The current international status of the euro

There are several criteria according to which one can examine the international importance of a currency in the financial system: Its use as a reserve currency for central banks, as a means of accumulation and as a transaction currency are the main factors that determine the extent of its internationalisation its global role. Following these criteria, the euro comfortably occupies second place in the international monetary system after the dollar.

The euro as a reserve currency

The most important indicator of the international use of currencies is usually their use as reserve currencies by central banks. In this area, the global dominance of the dollar has been unquestionable for many years, albeit its position is steadily weakening. According to data from the end of 2023, the share of the dollar in all foreign exchange reserves stood at around 59 per cent.11 The share of the US currency now stands at one of its lowest levels since the introduction of the euro in 1999. At that time, the dollar’s share was 71 per cent and the euro’s 17.9 per cent (see Table 2).12 Thereafter, the euro’s share in global foreign exchange reserves gradually increased, before the onset of the eurozone crisis in 2009. With a share of 19.58 per cent as of Q4 2023, the euro is currently the second most important international currency, ahead of the Japanese yen (JPY), the British pound (GBP) and the Chinese renminbi (RMB).13

Changes in the composition of foreign exchange reserves are due to various factors, with exchange rate fluctuations considered one of the most important. Thus, a weakening of the exchange rate of one currency against another also leads to a reduction in its share of central bank reserves.14 On the other hand, national banks also adjust their reserve currency portfolios in response to exchange rate developments.15

|

||||||||||||||||||||||||||||||||||||||||

The widely predicted shift away from the dollar in reserves as a result of the sanctions imposed against Russia has not transpired, with IMF data from the end of 2023 showing that the dollar’s position in foreign exchange reserves has not changed.16 And while a slow downward trend of the dollar has been observed for many years, this can be generally explained by the growing share of smaller, non-traditional currencies in central bank reserves.17

The euro in the international debt markets

Another indicator of the international role of a currency is its use in debt issuance. The share of the euro in in foreign currency denominated bonds worldwide (i.e. excluding domestic issues) reflects the volatility of confidence in this currency: at the end of 2008, the share of debt issuance in euros was around 32 per cent, after which it declined significantly due to the eurozone crisis, only to rise again significantly between 2020 (21.8%) and 2022 (24.7%).18 In this respect, too, the dollar remains by far the world’s most dominant currency. According to the European Central Bank (ECB), its share of total bond issues denominated in foreign currency amounted to more than 57 per cent in 2022.19 The dollar was also far ahead in the stock of international debt at 65 per cent compared to the euro at 22 per cent in 2022.20

An important feature that distinguishes the European debt market from that of the USA is its fragmentation. This applies not only to the disparities in legal systems, but also to credit ratings. Apart from the European Stability Mechanism (ESM), only Germany, the Netherlands and Luxembourg have a so-called “triple-A rating,” the highest credit rating in the eurozone.21 This limits the possibility of issuing assets with the highest rating. Despite the significant increase in the issuance of EU common debt instruments in euros in recent years, the euro area still plays a much smaller role than the dollar in the global bond market. An important differentiator for the EU as a debt issuer compared to other markets is the target of issuing at least 30 per cent of bonds (up to €250 billion) as “green bonds”.22

The euro in trade invoicing, on the foreign exchange market and in SWIFT payment transactions

The importance of a currency is also measured by the extent to which it is used in international trade and financial transactions. Here, too, the available data confirm the dominance of the dollar in the invoicing of trade transactions, exceeding what the USA’s position in global trade might indicate. The euro also plays an important role in the invoicing of international transactions, for which it is second only to the dollar.23 Indeed, the dollar dominates over the euro in the invoicing of imports into the EU. According to the latest available Eurostat data, 49.6 per cent of imports into the EU in 2022 were invoiced in dollars, compared to 41.5 per cent in euros.24 There are also significant differences among the EU member states: the Netherlands, Finland, Cyprus, Greece, Bulgaria and Poland invoice more than 60 per cent of their total non-EU imports in dollars, while for Slovenia this indicator is less than 22 per cent.25

The foreign exchange market is also dominated by the dollar. According to the latest data, the dollar was used in more than 90 per cent of the world’s foreign exchange transactions, and its dominance in all foreign exchange instruments is indisputable.26 The euro’s share was only 31 per cent in 2022, according to the Bank for International Settlements (BIS), compared to 39 per cent in 2010, before the eurozone crisis.27

The dominance of the dollar in SWIFT payment transactions.

Another important indicator of how widespread a currency is in the international financial market is its share of SWIFT transactions. SWIFT is a messaging system that allows banks to send and receive messages about financial transactions. Scrutinising payments made via SWIFT shows how frequently currencies are used for international interbank payments. Here, the primacy of the dollar can once again be observed, as this currency was used in 46.5 per cent of cases in 2023 by the end of July. In the first decade of its existence, the euro managed to overtake the dollar, but as a result of the eurozone crisis its use declined significantly (Table 3). By the end of July 2023, the euro had a much lower share of SWIFT payments than in the previous year, at 24.4 per cent.28 This is likely due to the fact that in March 2023, Europe moved to the new ISO 20022 payment standard, which may have led to the under-reporting of European data compared to other regions.29 A change of invoicing currency for the purchase of energy commodities as a result of the cessation of energy commodity purchases in Russia following its aggression against Ukraine could also have had an impact on SWIFT payments. The majority of euro-currency transactions in this system are carried out in the EU. The available data do not indicate that any shift away from the dollar in SWIFT transactions has occurred since the imposition of sanctions against Russia. Rather, a contrary trend can be observed. From the end of April 2022 to the end of July 2023, there was an increase of almost five percentage points in SWIFT payment transactions made in dollars (see Table 3). The opposite trend is detectable for the euro.30 Other currencies (not included in the table) had a significantly lower share of SWIFT transactions in August 2023, for example, the pound had 7.14 per cent, the yen 3.68 per cent and the renminbi 3.47 per cent.31

|

||||||||||||||||||||||||

Other indicators of internationalisation

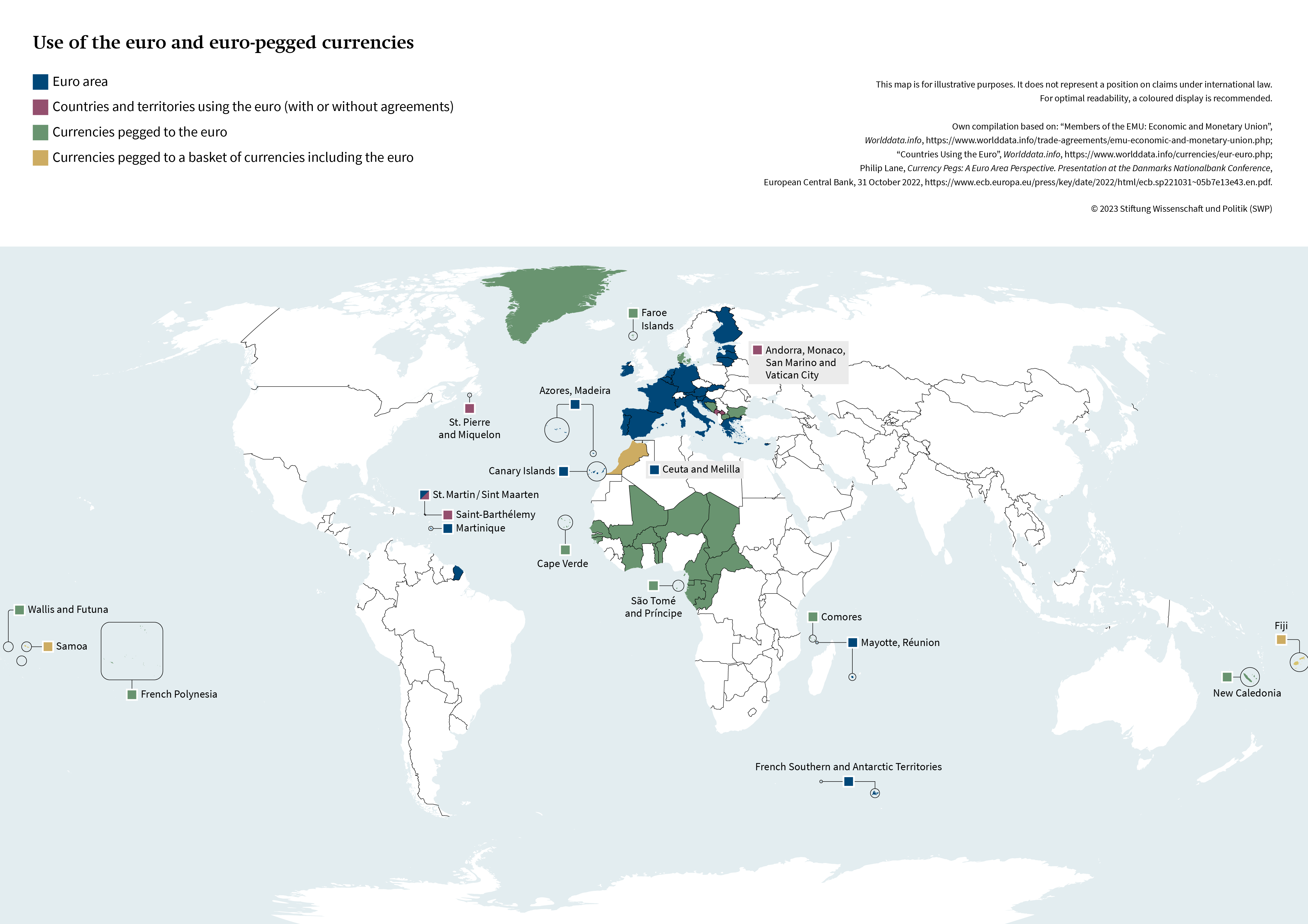

In addition to the indicators listed above, others are also used in the analysis of the international reach of a currency. One such is the amount of cash in a certain currency outside its country or currency area. The ECB estimates that between 30 and 50 per cent of euro banknotes circulate outside the euro area, which was equivalent to at least €167 billion at the end of December 2020.32 In practice, this figure could be much higher, as it is based only on data on transactions conducted by the largest global banks. The euro and related local currencies are used in countries that are not part of the EU or are even geographically distant from Europe (see Map 1). These include small non-EU countries such as San Marino, Vatican City, and Andorra, which use the euro on the basis of special agreements. In addition, Kosovo, Montenegro, and Albania have unilaterally opted for “euroization” (i.e. allowing the euro to be used as a means of payment without the approval of the ECB). The 14 African countries in the CFA franc zone use the Central African franc (BEAC franc) or the West African franc (BCEAO franc). Both currencies have a fixed exchange rate against the euro, although adherence to this system is controversial.33 The peg to the euro in these regions has little impact on international role of this currency. In the measure of use outside the issuing territory, the dollar’s lead remains overwhelming. According to estimates by Federal Reserve Board staff, by the end of 2022 there were more than US$1 trillion in dollar notes held by foreign users, accounting for about half of all dollar notes in circulation.34

In summary, the analysis of the most important macroeconomic indicators shows that the euro continues to be the second most important currency in the international financial system, while the dollar remains clearly the most dominant. Although the share of the euro is considerable in many market segments, for example, in payment transactions via SWIFT, it is still in many respects a currency with regional valence.

Benefits, Costs and Risks of the Internationalisation of the Euro

Strengthening the role of one’s currency in the international monetary system is often considered the most important element of monetary statecraft.35 The internationalisation of a currency brings economic and political benefits, but there are also risks attached.

Benefits

Economic benefits include the ability to raise cheaper capital for one’s own economy, the gains from money creation (seigniorage), the boost to national trade and reduced vulnerability to adverse regulatory actions taken by other countries. The appreciation and diffusion of one’s currency internationally not only increases the prestige of the issuer as an actor in the global economy, but also increases its monetary independence and expands its capability to influence others.

Possessing a currency with a strong international status increases the potential to influence other actors.

The most important advantage of an increased internationalisation of one’s own currency is the possibility to issue debt instruments at lower interest rates compared to other countries. This “exorbitant privilege” allows the U.S. government, for example, to finance budget deficits more easily and at lower cost.36 This increases the scope for fiscal policy and allows Washington to pursue more active international policies, for example, in financial, development or military aid. In this sense, the possession of a currency with strong international status increases the autonomy of one’s own actions and at the same time boosts the potential to influence others.37

One advantage of currency issuance is the so-called “seigniorage”. This refers to the difference between the cost of issuing a currency unit and its nominal value. An increase in international demand for a currency consequently leads to higher seigniorage profits. In the euro area, these profits benefit the individual central banks of the Eurosystem, which are passed on to the budgets of the eurozone member states.38 The seigniorage gains are at present relatively small and do not have a major impact on the budgetary situations of the member states. The proliferation of electronic payments and digital currencies will save central banks many of the costs associated with printing, transporting, protecting and storing physical money.

Another advantage of internationalising one’s own monetary unit is the expansion of trade in this currency.39 For example, the USA benefits greatly from the fact that many commodities, such as oil and gas, are sold mainly in dollars, which means that the country can eliminate exchange rate risk. Reducing the historical dominance of the dollar in the energy market in favour of the euro would bring similar positive effects to European countries. However, this is a very difficult process that requires a high degree of coordination, infrastructure development and consensus among market participants.

An enhanced circulation of one’s own currency at the global level is not only an instrument through which other international political actors can be influenced, but it also opens up the possibility of pursuing more autonomous economic and monetary policies in the sense of monetary statecraft.40 The most recent European example of this is the ECB’s relatively late interest rate hikes in 2022 compared to the Federal Reserve System, which kept more favourable credit conditions for the real economy for a longer period of time. The international standing of a currency is an important factor in monetary sovereignty. The system of international currencies is based on a hierarchy. As a result, the higher the rank a currency occupies, the better the issuer’s debt sustainability.41

The internationalisation of a currency is also linked to an increase in the issuer’s reputation, thus resulting in more soft power.

Increased recourse to the euro on a global scale could also help deepen European financial markets. This would not only lower the cost of raising capital, but also reduce dependence on international financial institutions and jurisdictions of states outside the currency area, thus also generating a geographical advantage.42 However, to fully benefit from autonomy in this area, the EU would need to develop a pan‑European card payment scheme, as, at present, the European market is largely dominated by US companies (i.e. Visa and Mastercard).

Finally, the internationalisation of a currency is also associated with an increase in the issuer’s reputation and thus also more soft power, which can be used to influence other states and institutions.43 One of the most noticeable effects here is an increase in the influence of one’s own financial institutions in international economic relations, especially in the form of financial sanctions. But the reputation of one’s own financial institutions, especially the central bank, is also of great importance. The key role of the ECB and the eurozone central banks in the Network for Greening the Financial System (NGFS) is a useful example of how European economic institutions have successfully built reputations on the global stage.44 For instance, the ECB is represented at meetings of international bodies such as the G7, the G20, the IMF, the BIS and the Financial Stability Board (FSB).

Costs and risks

In the literature, the most frequently mentioned costs of internationalising one’s own currency include the obligation to stabilise parts of the global financial system, the risk of currency appreciation and external constraint.45

Above all, the increasing prevalence of a currency in global payments means that the issuer must assume more responsibility for its own currency environment. Volatility can not only be triggered by external shocks, but can also be a side effect of monetary policy decisions. The series of rate hikes implemented by the Fed in 2022 and 2023 is one example of how such decisions can significantly affect the financial stability of countries that are heavily indebted in the US currency. Therefore, in the event of external shocks, the Eurosystem often needs to participate in stabilisation efforts undertaken by non-euro area countries. The two instruments most commonly used in the course of such measures include currency swaps and repurchase lines.

In the literature, the duty to provide assistance in times of stress is also referred to as exorbitant duty.46 A typical example of a central bank’s intervention as an international lender of last resort is the Fed’s provision of dollar liquidity during the global financial crisis of 2007–2009.47 The ECB also has to fulfil such a duty, albeit on a relatively smaller scale. In addition to the foreign exchange swap agreements with central banks worldwide, the ECB has also concluded currency swaps with several national banks of states that are within the EU but outside the euro area, namely Denmark, Sweden, Poland, Hungary and Romania.48

Another unfavourable effect of an international increase in the status of the euro could be the risk of excessive appreciation caused by a rise in foreign demand for the common currency. This would have a negative impact on the competitiveness of export-oriented economies, especially Germany. However, taking into account the increase in international significance of the euro in its first ten years, such a trend was not observed. Moreover, the appreciation of the currency would have had a positive effect on the purchasing power of companies and households. The spread of a currency in international circulation is also associated with the risk of a restriction of its own monetary autonomy, described by Benjamin Cohen as an “external constraint”. This risk primarily takes the form of speculative attacks on the currency in question. Such constraints could impede the conduct of monetary policy or even make it vulnerable to external actors.49 However, the effectiveness of such attempts at interference and challenges from outside is unlikely in the case of a large currency area.

The potential benefits and costs of currency internationalisation discussed here are difficult to quantify precisely. The literature dealing with strengthening the international role of the euro lacks a concrete cost-benefit calculation, as it may differ not only for individual member states but also for individual sectors and market participants.50 However, it seems that further internationalisation of the common currency is beneficial for the economically highly developed euro area as a whole. In particular, the possibility of raising capital more cheaply would be an important factor in enhancing investments or stabilising public finances. This could also help in financing the costly green transformation.

Obstacles to the Internationalisation of the Euro Currency

The euro is a very nascent means of payment compared to the other major currencies of the international financial system, a point often overlooked especially when analysing currency integration in Europe. For greater context, the euro was introduced in 1999, whereas the dollar was officially introduced as early as 1792. In addition, the euro project has so far not been sufficiently accompanied by a deepening of economic integration in Europe or significant real convergence. The further internationalisation of the common currency brings with it various obstacles that also have a negative impact on the stability of the euro area. These concern the economic and political heterogeneity and structural problems of the member states, the incomplete character of the monetary union and a lack of statehood of the currency issuer. All these factors, in turn, contribute to varying attitudes among euro area countries regarding the deepening of monetary integration, especially regarding the fiscal dimension or the role that the common currency should play in the international financial system.

The heterogeneity of the euro area

One of the main challenges of the euro area relates to its heterogeneity, which is mainly due to the diversity of member states’ economies, which some interpret as an expression of different models of capitalism. This heterogeneity also manifests itself in uneven levels of resilience to external shocks, which is considered one of the main causes of the euro area crisis.51

European economies have very different structures, sizes, strengths and weaknesses, and currently seem to diverge more than converge. From the perspective of the typology of major economies, at least three groups can be distinguished in the euro area: CMEs (Coordinated Marked Economies), MMEs (Mediterranean Market Economies) and LMEs (Liberal Market Economies) (see Table 4 for characteristics and examples). This categorisation does not cover all euro area countries, but it does illustrate the extent of the heterogeneity within the European currency area. In the case of the economies of some countries, for example, France, such a classification is complicated by the fact that the characteristics of more than one system are fulfilled. CMEs, MMEs and LMEs place different emphases on the independence of institutions and the role of the state in the economy. In a CME, the state is defined as an “enabler”, as its role is not to mediate between economic actors but to facilitate their activities. In an MME, on the other hand, the state is seen as an “influencer”, intervening directly in the interactions and productive capacities of economic agents when it deems it appropriate.52

The different roles that states play in the economy can be seen in the level of public spending in relation to gross domestic product (GDP). In France, this amounted to 59 per cent in 2021, which was the highest value of all OECD countries.53 In the Netherlands, the ratio was 45.8 per cent in the same year, while in Ireland it was only 24.4 per cent.54 These enormous disparities in state participation in the economy are also reflected in other areas, such as taxation or the functioning of pension systems. There are also considerable divergences in the openness of economies, which can be seen in the share of exports in the GDP generated. The EU member states show considerable structural differences in many other areas, for example, in labour market institutions, education and social security systems.

|

||||||||||||

In some member states, there are also significant regional disparities. An extreme case is Italy, where there are very large differences between the northern and southern regions in terms of unemployment and per capita GDP. In 2021, according to Eurostat, the latter was only 56 per cent of the EU-27 average in Italy’s southern region of Calabria, while it was 128 per cent in Lombardy, nestled in the country’s far north.55

The economic heterogeneity among member states makes it very difficult to achieve real convergence in the euro area.

The heterogeneity of the euro area economies is not only due to the diversity of the economic systems, but also to their different sizes. The three largest economies in the euro area are Germany, France and Italy. Together they account for almost 65 per cent of the GDP of the currency area, which includes 17 other states. This disparity in absolute economic performance has an impact in the form of different business cycles and on other measures such as the inflation rate. This often leads to disputes between small and large member states, especially when the main economic policy of the euro area conflicts between member states in the North and member states in the South. The economic heterogeneity among member states makes it very difficult to achieve real convergence in the euro area. Efforts to stabilise the currency area are merely constricted to trying to limit the effects of the divergence described.56

Structural problems of the eurozone member states and lack of convergence

More than ten years after the start of the euro area crisis, many member states are still struggling with a number of structural problems concerning competitiveness, sustainability of public finances, the banking sector and the labour market.

The central challenge of many eurozone countries is the high level of public debt, which was a main driver of the eurozone crisis between 2009 and 2015, and which led to a strong loss of confidence in the common currency. In the first half of 2023, the rating agency Standard&Poor’s awarded the highest credit risk rating (AAA) to only three of the 20 eurozone countries, namely Germany, the Netherlands and Luxembourg. Difficulties in securing room for manoeuvre in budgetary policy, macroeconomic imbalances, negative demographic prospects, crisis situations on the labour market and high costs of the energy transition characterise many countries in the eurozone to varying degrees. Several of these problems also affect Germany.

When the Economic and Monetary Union (EMU) was created in Europe, it was assumed that convergence between member states would gradually increase. This convergence was understood mainly in nominal terms, as reflected in the securitised budget rules and the criteria for joining the euro area (see Article 140(1) TFEU). However, the objective has not been achieved. Differences in labour market regulations, especially in wage setting, led to diverging labour costs, which in turn affected real effective exchange rates. This made the competitiveness gap even more pronounced. The available research on the subject suggests that little progress has been made towards convergence in the EU-12, which consists of the original euro area member states.57

Monetary statecraft begins with sustainable economic policies and political stability at the national level.

The past has shown that convergence has not increased sustainably despite the measures taken to strengthen the institutions of economic governance in the euro area, for example, through the creation of the so-called Macroeconomic Imbalance Procedure (MIP), and the further development of the fiscal framework. On the contrary, the enduring presence of numerous structural differences, which are crucial for the efficiency of fiscal transfers and thus for the pace of recovery, increases the risk of further divergence in the euro area.58 The ability to exert external influence and defend one’s monetary interests starts with building a certain margin of policy independence at home.59 The European Commission also pointed out in its 2018 Communication that strengthening the international role of the euro depends to a large extent on member states and their fiscal policies, as well as on adequate supervision of the financial sector.60 The eurozone, where many member states have serious structural problems, does not meet this requirement. To enhance the euro’s international importance, it is therefore considered far more important to eliminate deep-rooted systemic deficits than to expand the monetary union. In fact, the latter could even exacerbate the current divergence.61

The incomplete character of the monetary union

There is a broad consensus that the Economic and Monetary Union in Europe is incomplete.62 The 20 EU countries that have so far joined the third stage of the EMU share have a common currency while and the ECB is responsible for monetary policy. Economic and fiscal policy, on the other hand, is simply coordinated. Diverging political interests and structural problems of some countries hamper efforts towards fiscal integration, even at such a basic level as the establishment of common fiscal policy rules. There is a lack of trust among member states which stems from the fear of uncontrollable risks arising from the disproportionately higher potential of public finances in some of the larger euro area countries.

The euro area also does not have its own stability budget (fiscal capacity). The restrictions on the option to issue common EU and euro area debt instruments mean that there is little scope for the issuance of “safe assets”, usually cited as an essential factor in strengthening a currency’s international role. Instead, the debt market in the euro area is fragmented where there exists a crowding out of foreign investors by domestic players, as in the case of Italy. A major impetus for the pooling of debt was the COVID-19 pandemic, which forced the EU member states to create a special fund based on the EU budget. The key element here is the Recovery and Resilience Facility (RRF), a special lending and grant instrument of up to €723.8 billion (in 2022 prices). However, this mechanism was adopted as a temporary and one-off measure.

The European Stability Mechanism, which was launched in 2012 and has a lending capacity of up to €500 billion, currently plays a subordinate role in stabilising the euro area, as the potential recipients of this assistance are not willing to accept the associated conditions. For these reasons, the eurozone’s consolidation efforts rely mainly on interventions by the Eurosystem (the ECB and central banks). The ECB’s measures remain crucial for stabilising the euro area debt market. The incompleteness of the monetary union also applies to the banking sector. Despite the creation of a common system of banking supervision, there is still no deposit guarantee scheme. Efforts to increase the global use of the euro are also hampered by the incomplete nature of the EU single market, especially in the area of capital markets.63

Political diversity and lack of statehood

The political diversity within the euro area is a key feature that distinguishes it from other currency areas. The euro area currently comprises 20 countries of varying sizes. The lack of a single sovereign behind the common currency is seen as one of the main reasons for the failure to create a serious alternative to the dollar.64 For example, the coexistence of different political cycles within the euro area presents a major challenge to its cohesion. In the member states, elections and election campaigns (at the national or regional level) follow different calendars, often leaving little time to reach supranational compromises on issues related to the further direction of monetary integration in Europe.

Another problem is that some EU states are members of the eurozone, while others are not. This complicates the functioning of EU institutions in economic policy matters and poses a major challenge for further fiscal integration. For example, in order to provide financial support to euro area countries, the ESM had to be installed outside the EU legal system. Although the number of participants in the monetary union is steadily increasing, it still does not match that of the EU members. It is possible that in the future, other countries besides Denmark and Bulgaria will decide to peg their exchange rate to the euro under ERM-II (Exchange Rate Mechanism II). However, a renewed enlargement of the euro area to include Hungary, the Czech Republic, Denmark and Sweden seems unlikely as things currently stand. The accession of Poland, Bulgaria or Romania also seems uncertain. The format of the eurozone will likely remain distinct from that of the EU for an extended period, posing challenges to deeper economic integration and hindering the emergence of an effective supranational political representation for the common currency. What is more, previous attempts to establish such representation have proven unsuccessful.

The International Monetary Fund is the most glaring example of the lack of unified representation of the euro.

The lack of a unified external representation of the euro area in international economic and financial organisations is one expression of this institutional deficit. Proposals for a common representation of the euro area have been on the European policy agenda several times, but have not been realised.65 As early as 1998, the European Commission proposed a joint mission of the Council, the Commission and the ECB to various international bodies such as the G7, the OECD or the IMF.66 The necessity for a single representation of the euro area has been emphasised raised on many occasions.67 The most glaring example of the lack of such representation is the International Monetary Fund, whose membership is limited to states. In addition to the USA, China, Japan, Saudi Arabia and the United Kingdom, France and Germany also have a permanent seat on the Executive Board. The other euro states are part of different voting groups, which are represented by a chairperson in this body. On 21 October 2015, the European Commission presented a proposal to gradually establish a single representation of the euro area in the IMF by 2025.68 However, it has not been possible to overcome the mistrust between the member states and between the EU institutions regarding the role that the common currency should play in the international monetary system. Years of discussions on this issue have not yet produced any results in the form of institutional changes.

For France, currency integration in Europe was a step to counteract the supremacy of the dollar.

Particularly relevant here are the divergences of interest between France and Germany. France has a long tradition of resisting the dominance of the dollar. For Paris, currency integration in Europe was a step to oppose this supremacy.69 In Germany, the traditional view was that wider internationalisation of the currency should be the result of market decisions based on confidence in the stable economic fundamentals of the euro area, rather than a specific goal to be achieved.70 There was also a fear in Germany that strengthening the international role of the euro would lead to its appreciation, which would be detrimental to the German export-oriented economic model.71

At present, there is little evidence that the above challenges are being adequately addressed. This suggests that the euro area will remain one with a relatively high degree of economic divergence, fiscal decentralisation and a relatively low degree of political integration.

Capital Markets Union, Digitisation and Greening as Ways to Strengthen the International Role of the Euro

Despite the serious shortcomings and impairments that are holding back the development of the euro area, there are certain processes through which the international role of the euro can be potentiated: a deepening of the financial market in the EU (Capital Markets Union project, CMU), digitalisation and “greening”. In all these areas, however, specific obstacles are building up that need to be overcome both at the community level and at the level of the individual member states.

Capital Markets Union

The liquidity and the degree of integration of the financial markets are important prerequisites for strengthening the international impact of a currency. With the “Capital Markets Union” project, the EU is striving to unify selected areas of the capital market in Europe. The project formally concerns all 27 EU countries. However, it is of utmost importance for the overall stability of the euro area, for the introduction of a digital euro and for the transformation to a low-carbon economy. Financial markets in the EU and euro area – unlike in the USA – remain highly fragmented. The inability to mobilise private capital on a larger scale is a strategic weakness of Europe compared to the US, for example, where the private sector contributes much more to financing the green transition.

The inability to mobilise private capital on a larger scale is a strategic weakness of Europe compared to the US

The free movement of capital is one of the cornerstones of the single market. In the past, there have been numerous initiatives designed to integrate capital markets in Europe more closely. In 1988, capital controls were abolished. In 1999, the Financial Services Action Plan (FSAP) set out guidelines to further harmonise financial markets in the following years.72 The main impetus given to this process in the last decade was part of the effort to stimulate recovery after the eurozone crisis.

This also applies to the Capital Markets Union project, which was launched by the European Commission in 2015.73 It aims to deepen and unify the capital markets of the member states of the EU in order to improve financing options for companies and also give private individuals greater scope for investment.74 It also intends to increase the private sector’s contribution to cushioning economic shocks, especially in the euro area. In September 2020, the European Commission published a new action plan for the Financial Markets Union. With this, it wanted to give new impetus to the Capital Markets Union project. The Commission hoped to assist the acceleration of the economic recovery from the COVID-19 pandemic. The document proposes 16 legislative and non-legislative measures – such as EU-wide access to market data – to further integrate national capital markets. These measures include the establishment of a single access point for company and investment product data, rules to increase investment protection and monitor the adequacy of pensions, the harmonisation of national insolvency procedures and the establishment of greater convergence in the functioning of national supervisory authorities.75 In November 2021, the Commission presented four legislative proposals, which were in various stages of legislative work until mid-2023.

The integration of capital markets in the EU is a complex process that still faces elementary obstacles. The greatest barrier to cross-border capital flows remains the diversity of legal systems regulating financial markets in the individual EU countries.76 Among other things, different national insolvency regulations or the problem of double taxation continue to present challenges. The lack of standardisation of accounting and reporting rules severely limits market transparency. Language barriers make access to information difficult. Many of the activities of the Capital Markets Union require interaction with or support from member states.77

A factor that has also hinders the integration of European capital markets has been the United Kingdom’s exit from the European Union. Although many financial institutions have moved their offices and staff from London to continental Europe, the EU has lost its most important financial centre. This has reduced the size of the EU’s financial market compared to other global financial centres. The UK has many years of experience in the functioning of international financial markets. The loss of this knowledge makes it more difficult to draft and implement common EU legislation. Moreover, the UK has strengthened its competitiveness in the financial services sector after Brexit, among other things by lowering regulatory standards. The exit of the hitherto largest financial centre from the single market has intensified rivalry between European financial markets, which has a negative impact on integration efforts in this area.

The complexity of the legislative process within the EU is also a challenge for the realisation of the Capital Markets Union (CMU). Now that the EU has announced its major “flagship” projects in the area of financial services, the difficult task is to translate the agenda into appropriate legislation. However, this does not receive enough public attention. Instead, the effort is largely exposed to lobbying by representative market participants who resist change.78 Since the adoption of the CMU Action Plan in 2015, some progress has been made in integrating financial markets. For example, the European Commission monitors what is happening there on the basis of selected indicators such as the market funding ratio, the breadth of the listed equity market and the country-specific differences in selected market segments.79 However, the European Court of Auditors’ 2020 report was highly critical about how the CMU project was implemented and accused the Commission of lacking a clear strategy and priorities.80

The fragmentation of EU capital markets will continue for many years. The measures being taken in the EU to integrate financial markets more closely are making slow progress. However, the problem is not only at the EU level, but also at the national level. Although the Commission has given high priority to the CMU since it was first announced, the potential for capital market development in Europe by mid-2023 has unfortunately still remained largely untapped.

The digital euro

Digitisation is having a significant impact on international currencies, changing the way they are used, exchanged and managed. It has led to an explosive growth of electronic means of payment and cross-border money transfers, while at the same time posing a challenge to financial market institutions in terms of regulation and stability.

The process of digitalisation within the euro area was significantly accelerated when several international social media companies and sales platforms announced plans to create their own para-currencies.81 This raised fears that such projects could threaten not only traditional currencies but also the status of central banks. This is because the emergence of alternative money and payment systems would have a negative impact on the stringent implementability of monetary policy. Central banks have a special task in maintaining the stability of the financial system, which is called into question by the spread of digital currencies and alternative payment systems. Such systems, characterised by high liquidity, are vulnerable to sudden changes in customer preferences, which can lead to rapid capital outflows. These risks need to be further investigated in order to take appropriate regulatory countermeasures.

The ECB seems to be one of the more advanced central banks along the path to digital currency.

Central banks have pioneered research into digital currencies because of the threat to the efficiency of their operations and because they have the necessary technical and professional know-how to do so. The aim is to exploit the advantages of cryptocurrencies while giving them greater stability. The first central bank to start experimenting with a digital currency was the Central Bank of Ecuador. In 2014, it introduced a new digital currency called “Dinero Electrónico”.82 One of the main reasons for this project was to promote the use of an electronic payment system for everyday activities, such as purchases and transfers between individuals. Other state banks that started experimenting with digital currencies were include the Bank of Canada, the People’s Bank of China, the Bank of England and the National Bank of Sweden. Currently, it is estimated that more than 90 central banks around the world are exploring the introduction of digital currencies.83

In October 2023, the Governing Council of the ECB decided to launch a new two-year preparatory phase for the digital euro project.84 The preparatory phase will focus on drawing up the regulations and selecting the providers who will develop the platform and infrastructure.85 This work will pave the way for a potential future issuance of the digital euro. Despite advanced work on the digital euro, the ECB remains rather in progressing towards its introduction which will not happen until 2026 at the earliest and most likely only during the term of Christine Lagarde’s successor.

The digital euro could bring several benefits, for example, lower transaction costs, and faster, cheaper and more secure payments. The digital euro project is potentially relevant for the further internationalisation of the single currency. It could facilitate access to the euro outside the currency area, where there is no access to banking services denominated in euros or to a physical form of the currency, and where traditional payment units are weak and untrustworthy. It would therefore be especially important for those potential users who are not in euro area countries or in the EU single market to have access to the digital euro.

One criticism of the plans to introduce a digital euro is that its advantages compared to modern payment systems are not significant. Furthermore, there are fears that the digital euro could pose a threat to traditional bank deposits, which, given the incompleteness of the banking union, could lead to a flight of capital from these forms of investment.86 Finally, there are those who suggest that the project is an attempt by technocratic institutions to increase their control over citizens. In fact, the EU is the most developed economic area in terms of personal data protection. Therefore, the development of a European version of a digital currency would undoubtedly be an advantage for those countries where personal data are insufficiently protected from the interests of large economic platforms (USA) or where digitalisation is even seen as an instrument to strengthen state control over citizens (China).

Research on digital currencies also enables the improvement of existing payment systems. In this area, the internal market is characterised by great diversity due to the high number of card payment systems existing in Europe and the dependence on US companies. In some EU countries, for example, Ireland, the Netherlands, Sweden, Finland and Poland, credit card providers Visa and Mastercard serve almost 100 per cent of the market.87 The introduction of the digital euro could foster the development of a single European payment system, which would strengthen the autonomy of the EU single market in this area.88

Scientific studies on the digitalisation of currencies also provide insights into the impact of new electronic payment systems on the traditional role of money in the economy. One of these is the aforementioned risk to financial stability and the welfare of citizens, as the digital cryptocurrencies currently on the market are characterised by a high degree of speculation. The EU has therefore made efforts to regulate the use of digital currencies in the single market. For instance, the Regulation on Markets in Crypto-Assets (MiCA) was adopted in May 2023.89 The EU’s ability to shape its own regulatory environment for digital assets and ensure its effective enforcement will strengthen the stability of the European financial system and thus the EU’s autonomy and independence from other jurisdictions. The European Union has also taken the lead in regulating this market and is the first major jurisdiction in the world to subject digital assets and transactions involving them to a legal framework.

The digitisation of the monetary system is a multi-layered process that is not limited to experiments with currencies or payment systems. The process must also be inclusive, meaning that the potential benefits should be shared among society to the largest extent possible. This includes educating citizens about how the financial system works, the dangers of speculating with digital assets and the security of online payments.

The euro as a currency of green change

The increasing risks of climate change and the transition to low-carbon economies are currently among the most important challenges for European institutions and member states. This involves changing economic growth models, the functioning of market-based institutions (e.g. banking regulators) and financing the enormous costs of the transition. These expenses are a major burden for European economies, especially for those countries already struggling with excessive debt.

On the other hand, a properly programmed shift towards a low-carbon economy can also be an opportunity to create or unlock new potential for economic growth. The common currency and the institutions of the eurozone can play an important role in this process.

In 2022 forty-two per cent of global green bonds were issued in euros.

Eurozone institutions have made climate risk management and the green transition their top priorities. This is particularly evident in the example of the European Central Bank, which was the first bank in the world to include climate issues in its strategic review and to take concrete measures to green its monetary policy instruments. Together with other Eurosystem banks, it is active in international forums, including the Network for Greening the Financial System, in attempt to mitigate climate risks.90 Such activities and a prominent position in this area can have a positive impact on the ECB’s standing in the international financial system.

For example, the European Investment Bank was the first global issuer in the green bond market. The early promotion of this fast-growing market has resulted in about half of all global issuers being based in Europe and 42 per cent of the global green bond market being denominated in euros in 2022.91

The international role of the euro in greening is closely linked to financial market integration in the context of the Capital Markets Union, which – as described above – is, however, progressing very slowly. An expansion of the green segment of the European capital market would not only reduce transition risks, but could also accelerate the integration of the entire market in the future. However, there are still many challenges along the way. For example, a framework needs to be established for the disclosure of the climate compliance of companies’ business models, and EU standards for green bonds need to be set. Harmonisation of market regulation and supervision is also still pending.

The EU is currently working on the introduction of a classification system for ‘green’ activities, under which there will be an EU-regulated standard for green bonds. In the absence of such a recognised and harmonised classification of green assets, the risk of greenwashing, i.e. offering pseudo-green assets, increases. This could have a negative impact on the credibility of the entire market and ultimately on the image of the euro currency.

The greening of monetary policy, the issuance of green bonds and the new “green regulation” of the financial market can be seen as the beginning of the creation of a sustainable governance project.92 The announcement by the president of the Eurogroup,93 that the euro will become the currency of the green transition in 2021 is not merely rhetoric; rather, pursuing this goal can actually help to strengthen the role of the euro in the international financial system.

Outlook: The Euro and the Development of the International Monetary System of the Future

The future role of the dollar in the international monetary system

The end of the dollar’s hegemony has long been subject of debate. However, after sanctions were imposed on Russia following its aggression against Ukraine, this discussion has once again gained new impetus.94

Some authors have hypothesised that the extension of punitive measures to Russia’s dollar reserves will reduce the willingness worldwide to hold reserves in this currency. For instance, some states, especially non-democratic ones, may develop concerns about becoming too dependent on the US currency.95 On the other hand, as mentioned in the first chapter, interest in the dollar is also driven by geopolitical considerations.96 In other words, as the global situation becomes more uncertain, the tendency to accumulate safe assets linked to economies with converging political interests increases. Consequently, states that maintain close relations with the USA are unlikely to be interested in any change in the dollar’s status as a world’s dominant currency.

This also applies to a large segment of European countries, which are increasingly dependent on the military power of the USA. On the other hand, political change in the USA in 2024 could lead to greater divergence on both sides of the Atlantic. With this in mind, it is important for the EU to achieve greater autonomy in its monetary relations with the USA, as well as with regard to payment infrastructures. The dollar will continue to hold a key place in the global economy for a long time to come, as it fulfils most of the determinants of a leading currency, such as the rule of law, liquid and deep financial markets, currency convertibility, economic power and military strength of the issuer.97 Even the obvious weaknesses of the US political-economic system, such as polarisation, dysfunctionality in the area of fiscal policy and problems in banking supervision, are not enough to shake confidence in the dollar.

The rivalry between the USA and China will also gradually shift to currency issues and payment systems, as total domination of the dollar is uncomfortable for Beijing. As far as the internationalisation of the renminbi is concerned, China has done a lot in this direction in the last decade, for example, by invoicing trade transactions in RMB, concluding numerous swap agreements, establishing a convertible offshore RMB market in Hong Kong and gradually building its own payment infrastructure (CIPS, Cross-Border Interbank Payment System). However, despite the geopolitically ambitious infrastructure investment programme (Belt and Road Initiative) and the fact that the IMF officially declared the RMB a reserve currency in 2016 and included it in the Special Drawing Rights (SDR) system, Chinese efforts have not yet translated into a significant strengthening of the RMB’s international role.98 The stance of other countries comes into play here, especially that of India, which sees the settlement of trade agreements in RMB as disadvantageous because of its political rivalry with China.99

The biggest obstacle to increasing the RMB’s international role, however, is the fact that the Chinese Communist Party leadership is seeking greater consolidation of power and control over the economy, which contradicts this objective. In economic terms, this course manifests itself, among other things, in the intensification of surveillance of foreign company branches in China and the restriction of access to reliable company information.100 An uncertain regulatory environment, including doubts about respect for private property, prevents the RMB from further internationalisation. Against this backdrop, Western countries with their strong legal culture, access to market information and respect for civil liberties will retain a competitive advantage in the global monetary system. On the other hand, the RMB is likely to gain importance as international currency in the coming years simply because of China’s importance in finance and trade, and because of Beijing’s active policy of internationalisation of the RMB, including bilateral currency swaps and the development of digital money. The intensification of ideological, economic and military external expansion and open rivalry with the USA is unlikely to foster confidence in the Chinese currency among external users. The RMB could therefore become more widespread internationally, but not to the point of threatening the status of the US currency or the euro.101

In other parts of the world, there is little sign of a currency integration dynamic that could lead to serious competition with Western currencies. In early 2023, there were plans in Brazil and Argentina to create a new common currency. The main impetus for thinking about currency integration in the region is the negative impact of dollarisation for these economies. But without a strong fiscal framework and political stability, it will be difficult to move forward on this path.102

In the most important indicators for the internationalisation of currencies, such as trade and foreign exchange reserves, the dollar was still far ahead of the other major currencies in 2023. And there were no signs that this would change decisively.103 As for the eurozone, the decisive factor that will determine the future global role of its currency will be whether its largest member states will be able to address their structural weaknesses. Data from the last two decades show that a growing popularity of the US currency in many market sectors is leading to a decline in the use of the euro, and vice versa. The development of an alternative payment infrastructure is also an important aspect that will have an impact on the monetary system.

Gradual regionalisation

Trends towards the emergence of regional currency areas (including the euro area) are symptomatic of the fragmentation or regionalisation of the global financial system. This means that regional financial architectures are being created to accompany local efforts to deepen economic integration or to ensure macroeconomic and financial stability. This development manifests itself in many areas: in the development of payment infrastructures, in the establishment of regional financial supervisors and financial institutions, and in the form of the increasing importance of regional currencies. The most important trend that will shape the global economy in the future is the declining share of the EU and the USA in global GDP and the growing share of Asia.104 Since the size of a currency area correlates with the international importance of the currency, it will also be a challenge for the euro area to maintain the role of the euro in the global financial system.105 For this reason, the eurozone member states and the EU institutions must actively increase the international attractiveness of the common currency by advancing the Capital Markets Union project.

Another factor potentially driving the regionalisation of the international financial system is the geopolitical tensions and sanctions imposed on Russia, especially those affecting the banking sector. The freezing of foreign exchange reserves and the blocking of Russian banks’ access to the SWIFT interbank communication system has accelerated work on developing replacement structures that are independent of the punitive measures imposed by the USA and Europe. Since 2014, when there were calls for Russian banks to be excluded from SWIFT, Russia has been engaged in building its own SPFS (System of Transfer of Financial Messages). So far, however, the practical significance of this system outside Russia is marginal. China and India have also started to develop alternative interbank communication systems (China with the CIPS and India with the Structuring Financial Messaging System, SFMS).106 However, building such systems is a lengthy process, as the example of SWIFT shows, which started in 1973 and now covers more than 200 countries. Despite the installation of competing blockchain systems, SWIFT will continue to dominate interbank traffic for a long time to come thanks to its reach. Moreover, in the future, SWIFT could be the solution to the problem of blockchain platform fragmentation and serve as a hub for them.107

An important question is whether the progressive regionalisation of the international monetary system will lead to more stability or destabilisation. Theoretically, the dominance of a single currency has a consolidating effect on the global monetary system, as competition between two or more currency blocs can lead to political manipulation of the exchange rate and thus to a disruption and weakening of the system. On the other hand, the supremacy of one currency also carries the risk of negative chain reactions. A recent example is the Fed’s interest rate hikes in 2022 and 2023, which created major problems for developing countries in repaying their debts issued in dollar.

The digitisation and development of platform companies

The future development of the international monetary system will be greatly influenced by digitalisation. This – in conjunction with the increasing importance of platform companies in the economy – will work towards a gradual regionalisation of the financial system.

Europe’s weakness is that it has no player among the world’s largest companies, especially in information and communication technology, a sphere that is dominated by US firms. Among the ten largest corporations worldwide with the highest capitalisation are five platform companies that focus on online commerce by creating dedicated internet sales spaces (Table 5).

These platform companies currently play a key role in the global economy, especially in the areas of innovation, trade facilitation and job creation. They also have a strong influence on the functioning of the foreign exchange market whose impact is likely to extend to the international monetary system. Facebook, for example, has announced plans to create its own currency (Libra, later renamed Diem). In the future, it cannot be ruled out that social media or e-commerce platforms will create new digital currency spaces in which digital money becomes the official unit of payment. The implementation of these projects will come with enormous regulatory challenges, have an impact on exchange rates and put the enforceability of monetary policy to the test. The further development of virtual platforms such as cryptocurrency exchanges, blockchain and decentralised finance (Defi) bring both benefits and challenges compared to traditional system of financial intermediation. The monetary system is also on the cusp of the next big leap, known as tokenisation. This is the process of digitally encoding claims, which could significantly increase the capacity of the monetary and financial system in the future. The challenge for the EU and the euro will be to keep pace with these changes.108

|

||||||||||||||||||||||||

Digitisation generally affects all elements of the financial system, but in monetary terms it will manifest itself in the development of a market for digital currencies, payment methods and cross-border transactions. It may contribute to easier access to financial infrastructure; but it could also bring more volatility. Given the risk of sudden capital outflows, it will be important to keep an eye on the progress of market regulation by regulators and central banks and the impact of alternative currency projects on social behaviour and the traditional banking sector.

Abbreviations

|

BIS |

Bank for International Settlements |

|

BRICS |

Brazil, Russia, India, China, and South Africa |

|

CEPR |

Centre for Economic Policy Research |

|

CIPS |

Cross-Border Interbank Payment System |

|

CMU |

Capital Markets Union |

|

EBA |

European Banking Authority |

|

ECB |

European Central Bank |

|

EP |

European Parliament |

|

ESM |

European Stability Mechanism |

|

Fed |

Federal Reserve System |

|

FSAP |

Financial Services Action Plan |

|

G7 |

International forum comprising the most important industrialised countries at the time of its founding. |

|

G20 |

International forum comprising 19 states and the European Union |

|

GBP |

Pound Sterling |

|

GDP |

Gross Domestic Product |

|

ICT |

Information and Communications Technology |

|

IMF |

International Monetary Fund |

|

JPY |

Japanese Yen |

|

MIP |

Macroeconomic Imbalance Procedure |

|

NGFS |

Network for Greening the Financial System |

|

OECD |

Organisation for Economic Co-operation and Development |

|

OMFIF |

Official Monetary and Financial Institutions Forum |

|

PBoC |

People’s Bank of China |

|

RMB |

Renminbi |

|

RRF |

Recovery and Resilience Facility |

|

SDR |

Special Drawing Right |

|

SFMS |

Structuring Financial Messaging System |

|

SSM |

Single Supervisory Mechanism |

|

TEU |

Treaty on European Union |

|

TFEU |

Treaty on the Functioning of the European Union |

|

USD |

US dollar |

Endnotes

- 1

-

Susan Strange, Sterling and British Policy. A Political Study of an International Currency in Decline (R.I.I.A.) (Oxford: Oxford University Press, 1971).

- 2

-

David M. Andrews, ed., International Monetary Power (Ithaca, NY: Cornell University Press, 2006), 20–22.

- 3

-

See, e.g., European Commission, One Market, One Money. An Evaluation of the Potential Benefits and Costs of Forming an Economic and Monetary Union, European Economy 44 (Brussels, October 1990).

- 4

-

Marcel Fratzscher and Arnaud Mehl, eds., China’s Dominance Hypothesis and the Emergence of a Tri-polar Global Currency System, CEPR Press Discussion Paper 8671 (London: Centre for Economic Policy Research [CEPR], 1 November 2011); Richard Portes, “The Rise of the Euro”, CEPR, Voxeu Column (online), 14 June 2007.

- 5

-

See, e.g., Barry Eichengreen, Arnaud Mehl and Livia Chitu, How Global Currencies Work. Past, Present and Future (Princeton, NJ: Princeton University Press, 2018), 174.

- 6

-

Marek Dąbrowski, Increasing the International Role of the Euro: A Long Way to Go, CASE Reports 502 (Warsaw: CASE – Center for Social and Economic Research, 2020), 21.

- 7

-

Tomasz G. Grosse, Monetary Power in Transatlantic Relations. Study of the Relationship between Economic Policy and Geopolitics in the European Union (Warsaw: Natolin European Centre, 2009), 87.

- 8

-

Ibid.

- 9

-

Colin Weiss, Geopolitics and the U.S. Dollar’s Future as a Reserve Currency, International Finance Discussion Papers 1359 (Washington, D.C.: Board of Governors of the Federal Reserve System, 2022), 2, doi: 10.17016/IFDP.2022.1359.

- 10

-

Dąbrowski, Increasing the International Role of the Euro (see note 6).

- 11

-

International Monetary Fund (IMF), Currency Composition of Official Foreign Exchange Reserves (COFER), https://data.imf.org/ ?sk=e6a5f467-c14b-4aa8-9f6d-5a09ec4e62a4 (accessed 2 February 2024).

- 12

-

European Central Bank (ECB), The International Role of the Euro (Frankfurt, July 2009), Statistical Annex, p. 9.

- 13

-

IMF, Currency Composition of Official Foreign Exchange Reserves (see note 11).

- 14

-

Serkan Arslanalp and Chima Simpson-Bell, “US Dollar Share of Global Foreign Exchange Reserves Drops to 25-Year Low”, IMF Blog, 5 May 2021, https://www.imf.org/en/Blogs/ Articles/2021/05/05/blog-us-dollar-share-of-global-foreign-exchange-reserves-drops-to-25-year-low (accessed 5 September 2023).

- 15

-

Barry Eichengreen, “Is De-dollarisation Happening?” CEPR, Voxeu Column (online), 12 May 2023, https://cepr.org/ voxeu/columns/de-dollarisation-happening?utm_source= dlvr.it&utm_medium=twitter (accessed 5 September 2023).

- 16

-

International Monetary Fund (IMF), Currency Composition of Official Foreign Exchange Reserves (COFER), https://data.imf.org/ ?sk=e6a5f467-c14b-4aa8-9f6d-5a09ec4e62a4 (accessed 2 February 2024).

- 17

-

Eichengreen, “Is De-dollarisation Happening?” (see note 15); Serkan Arslanalp, Barry Eichengreen, and Chima Simpson-Bell, “Dollar Dominance and the Rise of Nontraditional Reserve Currencies”, IMF Blog, 1 June 2022, https://www.imf. org/en/ Blogs/Articles/2022/06/01/blog-dollar-dominance-and-the-rise-of-nontraditional-reserve-currencies (accessed 27 November 2023).

- 18

-

ECB, The International Role of the Euro, July 2009 (see note 12), 58; ECB, The International Role of the Euro (Frankfurt, June 2023), 8, https://www.ecb.europa.eu/pub/pdf/ire/ecb.ire202306~d334007ede.en.pdf (accessed 5 September 2023).

- 19

-

ECB, The International Role of the Euro, June 2023 (see note 12), 27.

- 20

-

Ibid.

- 21

-