Turkey’s Industrial and Supply Chain Policy

Goals and Prospects for German-Turkish Economic Cooperation and Bilateral Relations

SWP Research Paper 2025/RP 02, 04.08.2025, 36 Pagesdoi:10.18449/2025RP02

Research AreasDr Yaşar Aydın is a researcher at SWP’s Centre for Applied Turkish Studies (CATS).

-

Turkey’s geopolitically motivated industrial and supply chain policy implies close ties to Germany as well as a security and economic policy orientation towards the EU.

-

Ankara wants to bring production and sales into line with EU standards and establish a green high-tech and services economy. However, its decarbonisation measures remain inadequate.

-

Turkish stakeholders see disruptions to global supply chains as creating the opportunity to relocate European production chains to Turkey (nearshoring). The government, the private sector and business organisations are all working to expand sustainable energy supplies.

-

Turkey’s authoritarian domestic policy – namely, the dismantling of democracy, repression and disregard for the rule of law – makes it extremely difficult to deepen bilateral cooperation.

-

Despite close economic ties, there are normative differences between Germany and Turkey and a consistent strategy to overcome them is lacking. Rather, the Turkish government is focused on using industrial policy to compensate for shortcomings in the rule of law.

-

Amid the geopolitical tensions between the United States and China, Turkey is performing a delicate balancing act: it is maintaining its ties to the West while at the same time expanding its technology partnership with China and energy cooperation with Russia.

-

German policy towards Turkey requires a strategic rethink. It should endeavour to promote economic stability, strengthen Turkey’s security policy integration into Europe and counteract Ankara’s strategic rapprochement with Moscow and Beijing. Going forward, cooperation should be made conditional on democracy, the rule of law and human rights.

Table of contents

2 Turkey: Geopolitical Repositioning and Diversification of Supply Chain Integration

2.2 Ankara’s calculation: More room for manoeuvre through multipolarity

2.3 Opportunities for Turkey through US‑China rivalry

3 German-Turkish Economic and Supply Chain Integration

3.2 Raw material and agricultural imports from Turkey

3.3 German investments in Turkey

3.4 Turkish companies in global value chains

3.5 Turkish companies in German value chains

4 Turkish Industrial Policy: Challenges and Opportunities

4.1 Restructuring supply chains

4.2 Goals of Turkish industrial policy

4.3 Goals of Turkish energy policy

4.3.1 Energy transition and decarbonisation

4.4 European Green Deal and CBAM: Blessing or curse?

4.4.1 Carbon Border Adjustment Mechanism

4.5 Economic policy and regional challenges

5 Turkish Supply Chain Policy: Shortcomings and Prospects

5.1 Turkey’s supply chain policy

5.2 German and European supply chain governance

5.3 Areas of cooperation: Energy, automotive and defence

5.3.1 The German-Turkish energy partnership

5.3.2 Automotive and defence industry

Issues and Conclusions

German-Turkish relations have been volatile in recent years, mainly owing to Turkey’s autocratisation and its transactional foreign policy. Ankara’s main foreign-policy goal is to reduce the country’s growing security dependence on the European Union (EU) and the United States (US). The guiding principles here are “diverse orientations”, “flexible alliances” and “issue-related cooperation”. It could be argued that these principles suggest Turkey is turning away from the West, especially the US and the EU. But this research paper argues that inherent in Turkey’s industrial and supply chain policy is a strong drive towards cooperation with the EU and Germany. Anchored in a geopolitically and geoeconomically motivated “Grand Strategy”, Turkey’s industrial and supply chain policy serves as a pull factor and keeps Turkey in NATO and within the orbit of the EU – and thus Germany. At the same time, economic cooperation with Russia and China as well as attempts to establish closer ties to the BRICS (Brazil, Russia, India, China and South Africa) are also part of Ankara’s foreign trade strategy. In accordance with this strategy, Turkey wants to diversify its export markets and leave various cooperation options open in a world characterised by multipolar interdependencies.

Turkey’s industrial policy is centred around a supply chain strategy and an energy policy that is oriented towards the EU. The aim is to transition to a green high-tech and services economy that is carbon-free and to achieve the closer integration of Turkish companies into European and German supply chains. But although Turkey is pursuing ambitious goals, there are considerable weaknesses in its implementation of decarbonisation measures.

Despite political tensions, German-Turkish economic relations have expanded and diversified in recent years. Germany is Turkey’s most important trading partner in the EU. However, the current trend can be expected to continue only if regulatory risks – such as those arising from supply-chain governance requirements and the European Green Deal (EGD) – are mitigated by the state and through entrepreneurial activity. These risks present a challenge for bilateral trade, for German direct investment in Turkey and for the integration of Turkish suppliers into German supply chains. If Turkish economic policy fails to develop suitable strategies and the private sector does not make the necessary adjustments, the economic ties between the two countries could weaken.

The answer to the central question of this research paper – whether the trend towards economic integration will continue or reverse – can be summarised as follows: the Turkish government, the private sector and business organisations are working closely together to ensure compliance with the EGD, accelerate the transition to sustainable energy supplies and strengthen Turkey’s position in Europe’s supply chains. Although Ankara is striving to improve the investment climate in the country, the effectiveness of purely economic policy initiatives is limited by democratic shortcomings and disregard for the rule of law.

While Turkey distancing itself strategically from the EU and Germany does not appear a rational prospect, it cannot be ruled out in the context of geopolitical and regional crises and Turkey’s intensified autocratisation. Ankara’s current efforts to deliberately weaken the opposition requires a new Turkey strategy – one that enables Germany and the EU to put their economic and political relations with Turkey on a sustainable footing without indirectly legitimising authoritarian tendencies.

Turkey: Geopolitical Repositioning and Diversification of Supply Chain Integration

In recent years,1 there have been a number of global developments that have necessitated the reorganisation of supply chains2: in particular, the “trade war” between the United States and China, the Covid-19 pandemic and the resulting disruption to supply chains, as well as the Russian invasion of Ukraine and the subsequent sanctions and export controls imposed on Russia. All these developments, together with the supply bottlenecks, production problems and rapidly rising transport costs, have increased awareness of just how vulnerable production is to disruptions in the supply of raw materials and energy and just how dependent it is on global supply chains.3

Representatives of the Turkish government and industry are campaigning for foreign companies to relocate production to Turkey.

For their part, Turkish decision-makers, entrepreneurs and economists believe that this vulnerability and dependency creates opportunities for Turkish industry: namely, European companies relocating their activities and supply chains to Turkey (nearshoring).4 According to the experts, this would also boost the resilience of German companies and their security of supply. Compared with the transport routes from countries currently being discussed in connection with the relocation of supply chains – such as Indonesia, Malaysia and Vietnam – those from Turkey would, in fact, mean less exposure to the risk of politically motivated blockades or bottlenecks in the Suez Canal. Turkish government officials and business representatives have repeatedly emphasised that the relocation of production to Turkey is highly welcome. But this stance is challenged by the geopolitical turbulence in the region, the erosion of the rule of law in Turkey, domestic political and economic dynamics and the uncertainty surrounding the country’s future geopolitical orientation. For its part, Berlin is concerned about the fact that Turkey is increasingly developing into an authoritarian state – one in which democratic efforts are depicted as a threat to state security.5 And there was also bilateral disagreement over Turkey’s confrontational foreign policy in Syria up to the fall of Assad and towards Israel. All these developments hamper the deepening of current economic ties and the interlinking of supply chains.

For some time now, Turkish foreign policy has been increasingly characterised by transactionalism,6 including vis-à-vis Germany. In this context, transactionalism refers to a situational foreign policy that is averse to value-based policymaking and unwilling to invest in an open, rules-based international system. “Diverse orientations”, “flexible alliances” and “issue-based cooperation” have been identified as the guiding principles of Turkish foreign policy.7 The pursuit of “strategic autonomy”,8 that is, striving for the strengthening of national sovereignty, the lessening of dependence on external actors and the positioning of the country as a regional power, has gone hand in hand with establishing closer ties to non-Western actors such as Russia and China. Russia’s war of aggression against Ukraine, the Gaza conflict, Israel’s attacks on Lebanon and the armed struggle between Iran (and its proxies) and Israel have had the effect of significantly enhancing Turkey’s geopolitical status as a regional power.9

Turkey’s ‘Grand Strategy’

Turkey’s “Grand Strategy”10 comprises three main objectives that serve as a guide for the country’s foreign, security and foreign economic policy: the pursuit of strategic autonomy, the enhancement of Turkey’s regional and global status and the achievement of sustainable economic growth.11 Strategic autonomy refers to the country’s ability to ensure its existence, sovereignty, territorial integrity and security largely through its own efforts. Status enhancement is related to the government's endeavours to establish Turkey as a regional power and elevate its status to that of “global player” (geopolitics12). At the same time, Ankara is aiming for sustainable economic growth in the long term in order to be able to support its foreign and security policy goals (geoeconomics13) and meet the growing population’s desire for prosperity. However, there is no national consensus on Turkey’s geopolitical positioning. The advocates of strategic autonomy are opposed by transatlanticists and Eurasianists, although the latter are politically marginalised and have only limited influence.

The Turkish Grand Strategy was drawn up in the wake of the global financial crisis of 2008, the United States’ gradual moves to withdraw from the Middle East at the end of the 2000s and the subsequent Arab uprisings. From a Turkish perspective, these developments signalled the shift from a unipolar to a multipolar world order.14 During the consolidation of its rule, the AKP government largely replaced the secular-national elite with an Islamic-conservative one.15 By abandoning the pursuit of pro-Western modernisation, Turkish foreign policy went from an institutional Western orientation to a pragmatic, transactional interaction with the West – i.e., the US, NATO and the EU. At the same time, Ankara promoted the narrative of the ‘Turkish century”, which served to keep competing domestic interest groups within a single power bloc and secure the consolidation of the AKP government’s rule. The authoritarian unilateralism of the second Trump administration will only reinforce transactionalism in Turkish foreign policy and could prove advantageous for Ankara in its relations with the US.

Ankara’s calculation: More room for manoeuvre through multipolarity

Most Turkish decision-makers and experts in international politics interpret the perceived emergence of a multipolar world order as an opportunity to increase foreign policy options. According to this interpretation, it is geostrategically advantageous for Turkey if Russia remains a strong “global player” in international politics and if China is an “alternative in reserve” to the US and Europe – a kind of “reinsurance” so as not to become completely dependent on the West and to have more room for manoeuvre. Thus, an unconditional foreign policy orientation towards the West is no longer a matter of course, even if Turkey’s anchoring in the transatlantic military alliance and the EU economic area is not up for discussion.16

Turkey favours a “more balanced distribution of power” and would like to play a role in the reorganisation of the regional order.17 In order to justify the global ambitions and regional claims of its foreign policy, Ankara points to the country’s geographically central location at the interface between Europe, Asia and Africa, its proximity to centres of conflict and its control over strategically important sea routes and access to the Mediterranean from the Black Sea. Moreover, Turkish foreign policymakers draw on the country’s historical and cultural links to the Balkans and the Islamic world.18 And it is in this context that Turkey’s demand to be more involved in the EU’s foreign and security policy is to be seen.19

Further, Ankara sees multipolarisation as a process that goes hand in hand with the dwindling dominance of the West. China’s rise as a great power and the refusal of the Global South to follow the West in strategic decision-making – as recently demonstrated in the case of the Russian war of aggression against Ukraine and the Gaza war – are perceived in Ankara less as a threat than as an opportunity. Against the backdrop of the BRICS’ criticism of the Western discourse on liberal democracy and human rights, Turkish decision-makers feel vindicated in their distanced stance towards liberal democracy and their authoritarian-majoritarian understanding of democracy. The demands of the BRICS members Brazil, India and South Africa for greater influence in international organisations such as the United Nations, the International Monetary Fund (IMF), the World Bank and the World Trade Organization are largely aligned with Ankara’s strategic interests.

Opportunities for Turkey through US‑China rivalry

The rivalry between the US and China – which manifests itself in a trade dispute and armaments buildup, among other things – poses a serious risk for the global economy, world trade and international peace. But in Turkish government circles, this rivalry, together with the rise of the BRICS+ group, is seen as an opportunity to upgrade the country’s role in European supply chains and diversify its export markets. As far as the technology rivalry between the US and China is concerned, Turkey is maintaining equidistance and exploring opportunities for a technology partnership with China, particularly in the area of 5G technology (the fifth-generation mobile communications standard).20 At the same time, the Turkish government is trying to position itself as the mouthpiece of the Global South and is considering joining BRICS+, which, it hopes, would improve its links to emerging economic areas.21 (The BRICS+ countries currently account for 45 per cent of the world’s population, generate 34 per cent of global economic output and are responsible for 50 per cent of global CO2 emissions.22) In the meantime, Ankara is increasingly orienting itself towards the Asia-Pacific region, which is capturing a growing share of the global economy. In this way, it wants to open up new export markets, attract foreign investment and secure more opportunities for cooperation. In particular, there is a focus on deepening economic relations with China.23

Turkish decision-makers regard their foreign policy course as vindicated by the divergence of interests within the Western world. In Ankara’s view, the US is less concerned about enforcing an international rules-based order than about containing China in the Indo-Pacific region and regaining hegemony in the “Western world”. However, it is seen to be repeatedly exempting itself from the rules of the “liberal order” that Washington itself developed. As a result, there has been a considerable loss of confidence worldwide – and not least in Turkey – in US-Western concepts such as multilateralism and a “values-based foreign policy”. In a keynote speech in Washington in spring 2023, Jake Sullivan, national security advisor to then US President Joe Biden, declared the rules-based trade order a failure and called for a paradigm shift: according to him, the world and trade order which the US created after World War II and of which it subsequently served as guarantor had become a disruptive factor in the containment of the “Chinese struggle for world domination”.24 For Turkish decision-makers, this only proves that the US is concerned primarily with securing its hegemony and will therefore decouple from China in the areas of trade policy and technology.25

Under the second Trump administration, the US will be less willing to provide global public goods26 such as security, free trade, functioning financial markets and stable currency systems. However, Washington is not expected to practise global political abstinence, as can be seen from Trump’s plans for Greenland, Canada, Mexico, the Panama Canal and the Gaza Strip. Thus, the EU will have to develop – independently of the US, not least in the context of the Ukraine war – the necessary capabilities to protect Europe. Key prerequisites for this are Turkey remaining in the European economic area and being more closely integrated into the European security architecture. The country’s geopolitical situation, its military capabilities, its growing defence industry and its connections and influence in the Balkans, the Caucasus and the Black Sea region all speak in favour of such an outcome.27

Deeper bilateral cooperation is made difficult by the dismantling of democracy and the restrictions on fundamental rights in Turkey.

However, there are limits to the intensification of Germany’s security and economic policy cooperation with Turkey – whether at the EU level or bilaterally. This is because of recent developments within Turkey or, more precisely, the two countries’ different ideas of about what constitutes legitimate rule. Bilateral cooperation is made difficult by the Turkish government’s pursuit of an authoritarian domestic policy that is accompanied by the dismantling of democracy, the weak rule of law and severe restrictions on fundamental rights. Turkey views any criticism of the above as an attack on its very existence.

Nevertheless, our analysis of the Turkish Grand Strategy reveals that Ankara is striving for closer cooperation with the EU and, in particular, with Germany – a thesis that is underpinned in this paper by a multi-stage analytical approach. First, the degree of economic interdependence between Turkey, the EU and Germany in particular is analysed. The focus here is on Turkey’s continued dependence on the EU and Germany as export markets and sources of transformative investment, technological expertise and high-tech products. Second, Turkey’s efforts to adapt to both the EGD and supply chain governance are analysed. Turkey’s current industrial policy is examined, including the implementation of the reforms needed to comply with European standards. Third, a risk analysis of Turkish-German cooperation takes a critical look at the political framework conditions in Turkey and developments in the areas of human rights and the rule of law. These are factors that pose significant challenges for a further deepening of economic relations.

German-Turkish Economic and Supply Chain Integration

German-Turkish economic relations – which, above all, encompass trade, investment, supply chain integration and technology transfer – form one pillar of the bilateral relationship (while the military alliance partnership within NATO forms another). The strong cohesiveness of these relations has so far withstood the political differences and diplomatic tensions. They continue to be a significant driver for the Turkish government and the export sector in the bid to further deepen economic cooperation and integration into global supply chains. Achieving these goals requires not only constructive political relations with the EU and Germany but also a stable and reliable investment climate. Bilateral trade and reciprocal investment are both a prerequisite and a benchmark for successful supply chain integration. Thus, this section looks at the economic fundamentals before analysing supply chain integration in more detail.

Growing bilateral trade

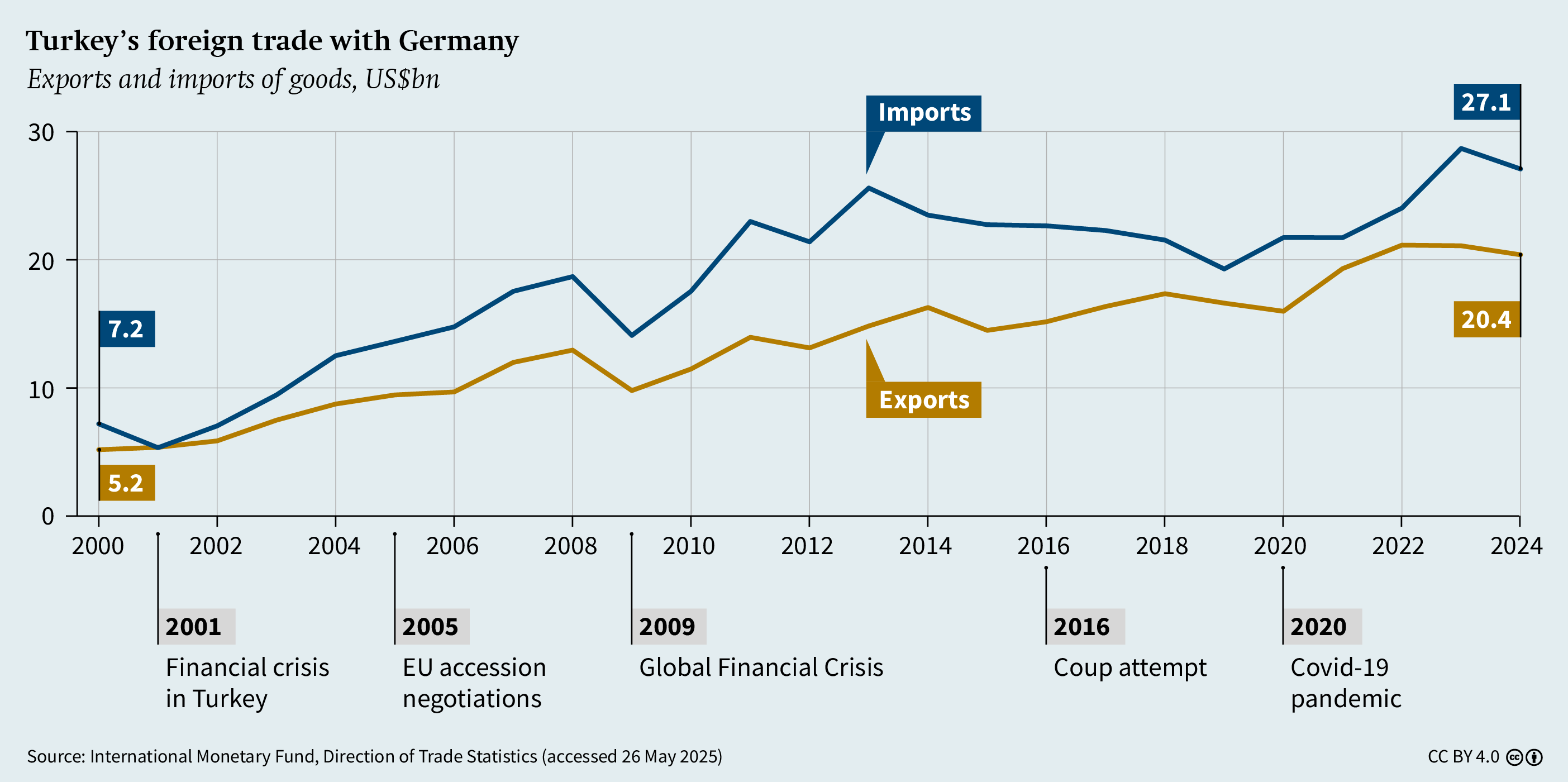

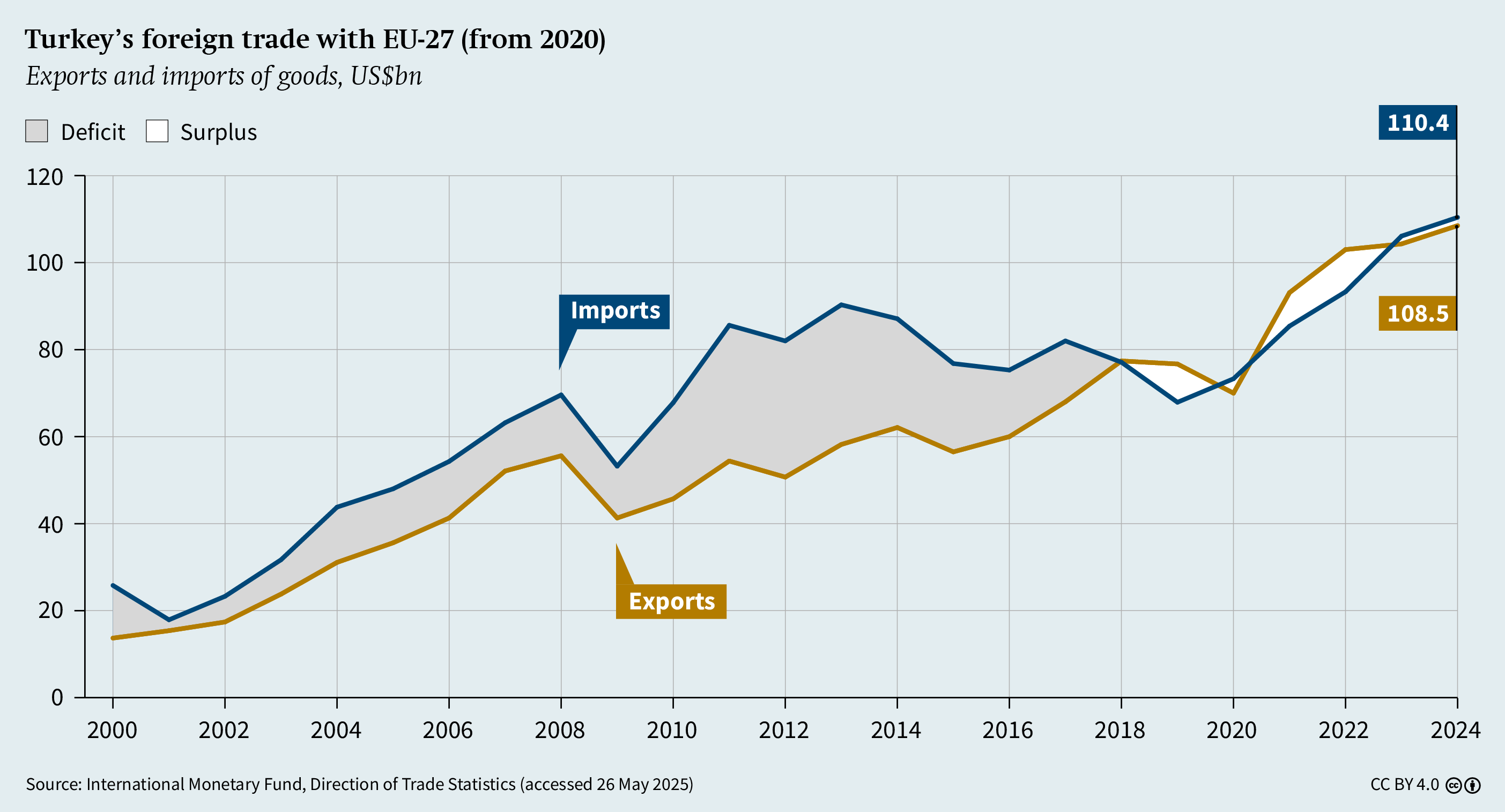

Despite not only the economic and legal challenges but also the political differences between Ankara and Berlin, bilateral trade is growing steadily. In 2024, it reached a record US$47.5 billion (see Figure 1, p. 13). Turkish exports to Germany have risen each year since the establishment of the EU-Turkey Customs Union. In 2023, Germany was Turkey’s largest export market, accounting for 8.7 per cent of total exports, and its third-largest import partner after Russia and China. Similarly, trade between the EU and Turkey rose to a record US$218.9 billion in 2024 (see Figure 2, p. 13). Around 41 per cent of Turkish exports were destined for the EU, while 32 per cent of the country’s imports were from EU member states. Compared with Turkey’s overall trade and its bilateral trade with Russia and China, Turkish-German and Turkish-European trade is more balanced, underscoring the importance for Turkey of both the EU and Germany as export markets that offer the potential for the country to offset its trade deficit.

In 2023, the main Turkish exports to Germany were vehicle parts, engine parts and motor accessories (worth US$1.63 billion) and cars (US&1.13 billion). This points to the significant forward integration of Turkish automotive suppliers into German supply chains. Turkish exports to Germany also include various types of machinery as well as plants and equipment for the construction, manufacturing, agriculture and transport sectors.28

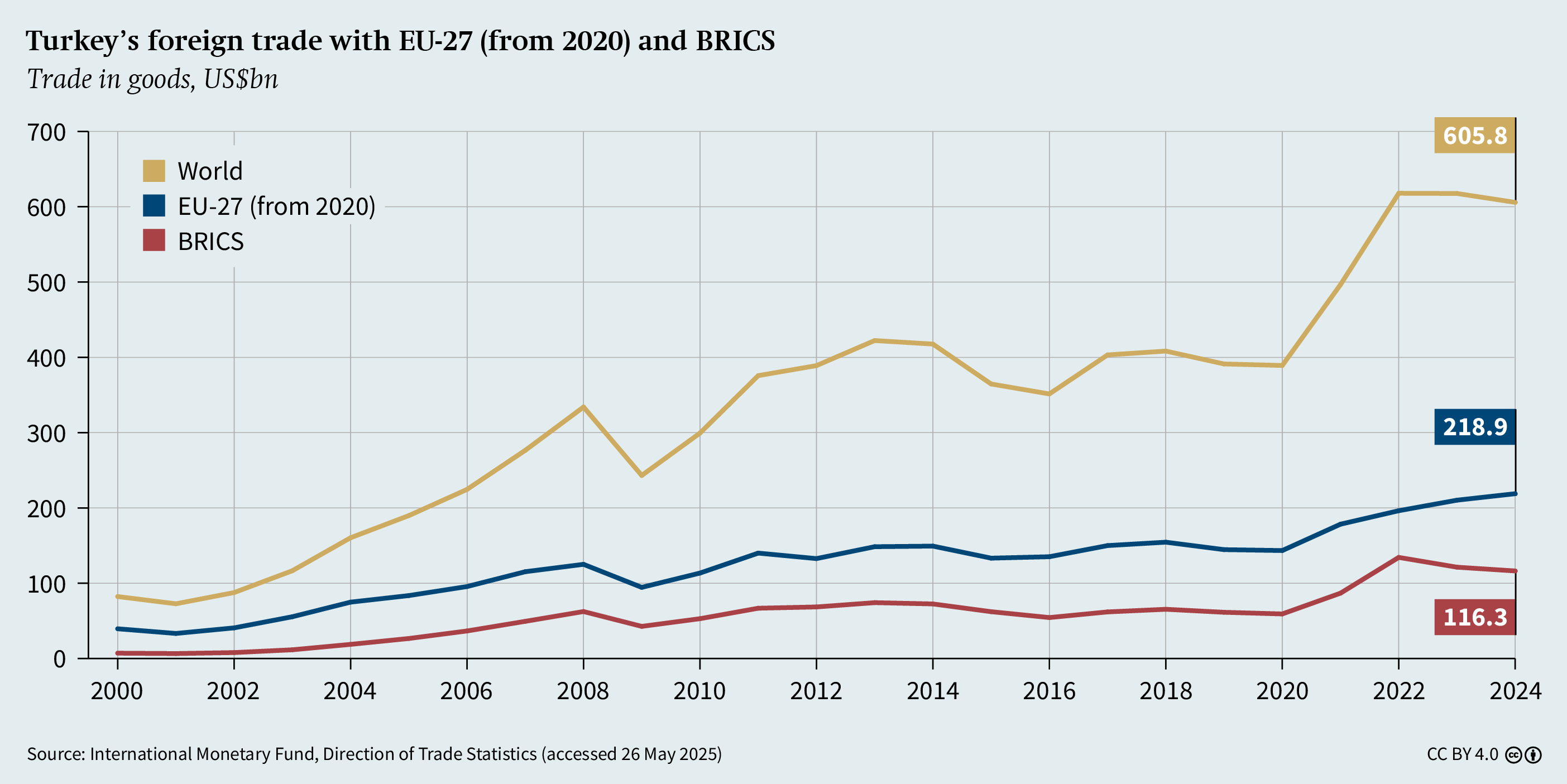

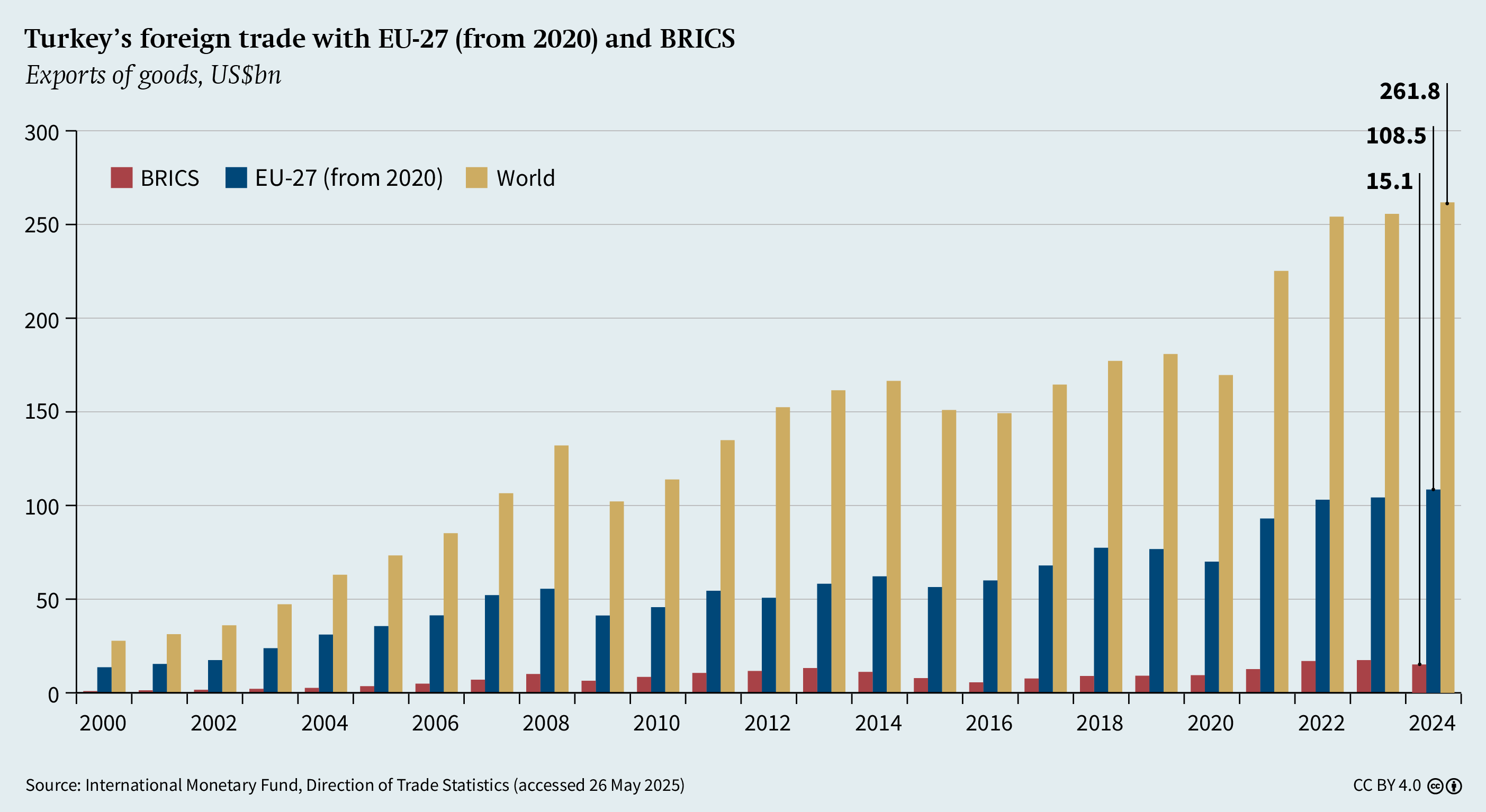

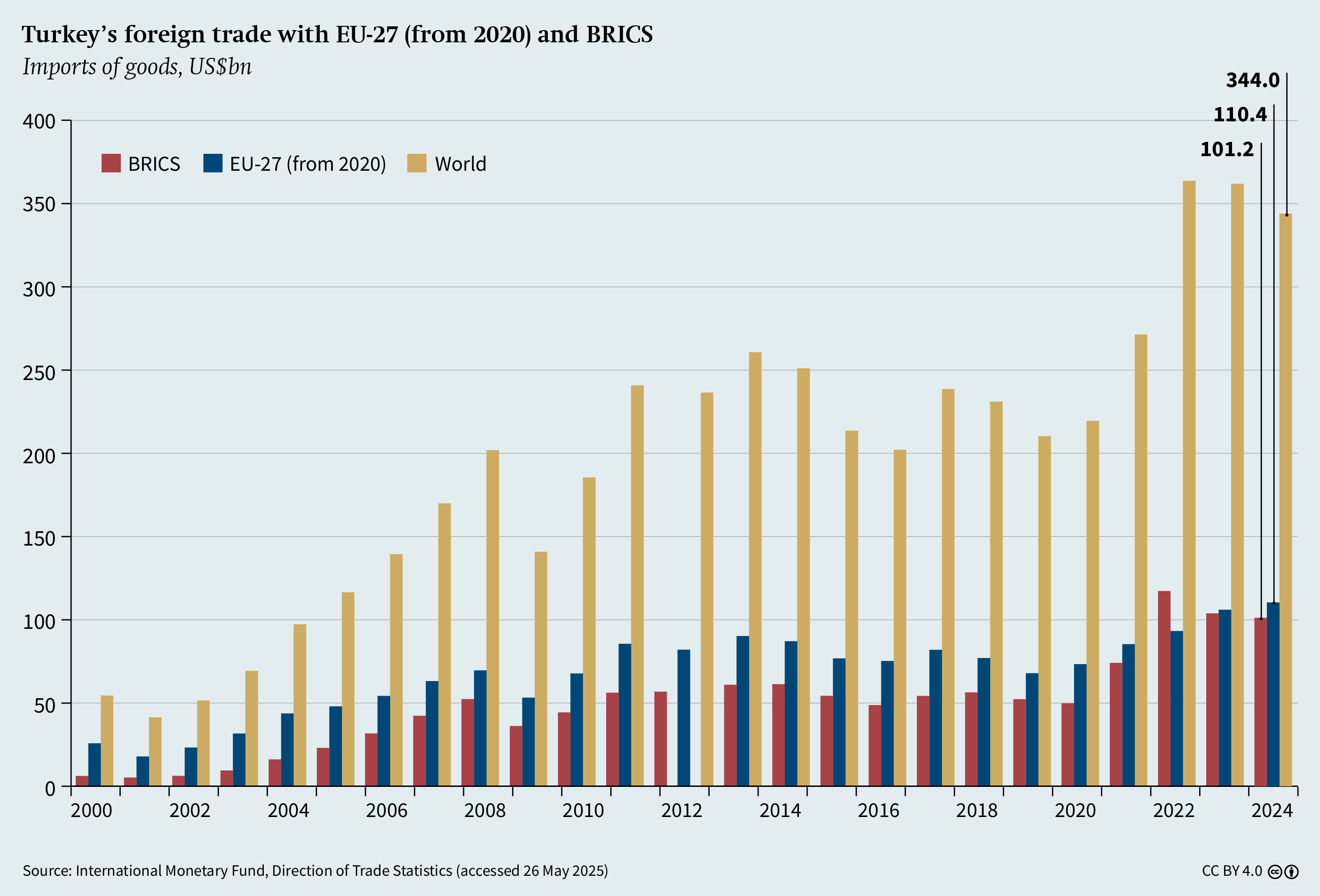

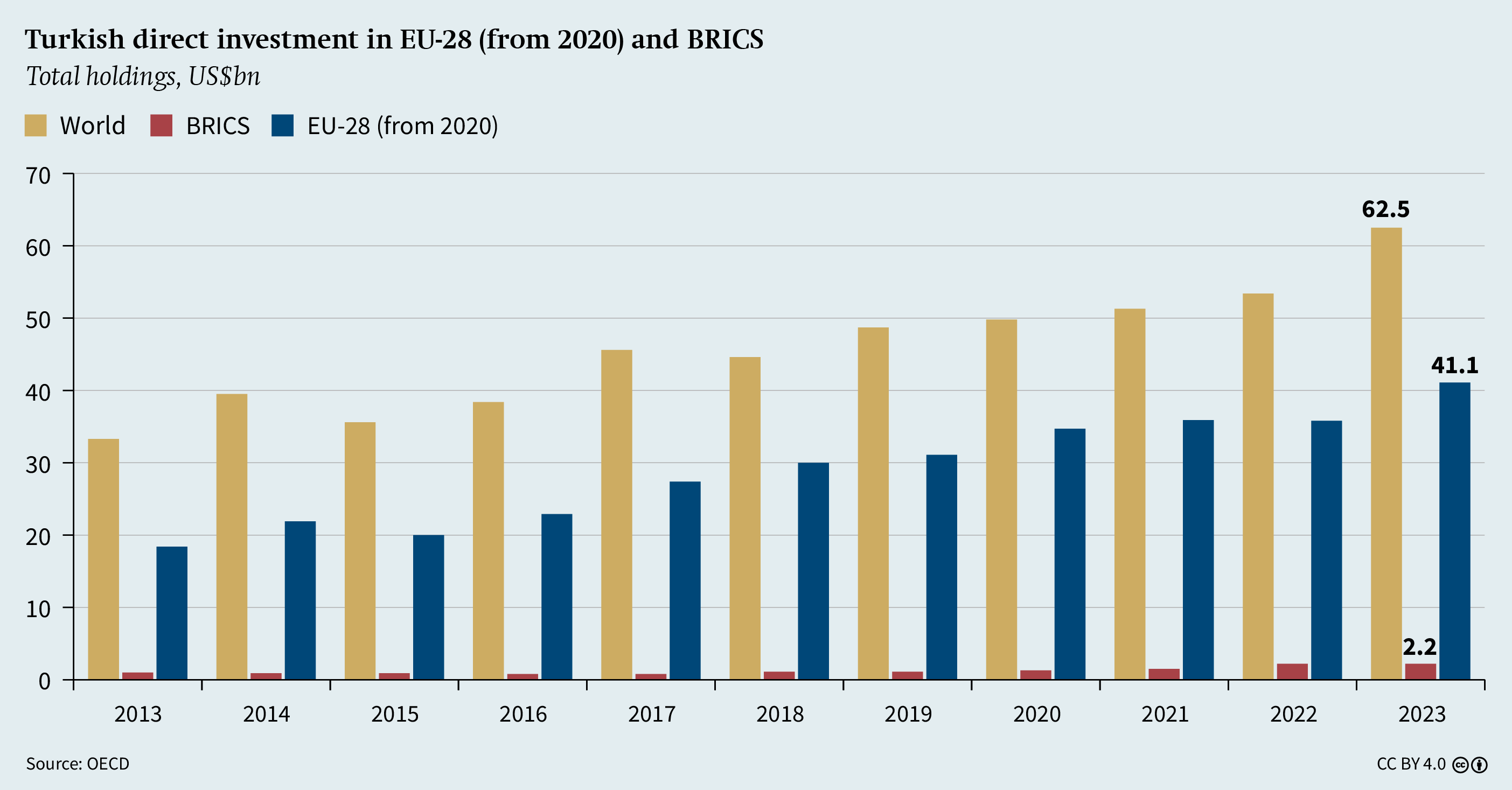

Trade with non-EU countries has increased significantly, too (see Figure 3, p. 15). According to official figures, the volume of trade between Turkey and the BRICS grew from US$74.3 billion in 2013 to US$121.3 billion in 2023, with Russia and China accounting for a lion’s share of US$105 billion – or 17 per cent of Turkey’s total foreign trade.29 But overall trade with the BRICS is unbalanced, with Turkish exports to those countries having stagnated (see Figure 4, p. 15 and Figure 5, p. 17).

Raw material and agricultural imports from Turkey

Turkey accounts for only a small share of German raw material imports but plays an important role in some segments. Germany obtains the bulk of its raw materials from a large number of countries and is therefore not overly dependent on Turkey for supplies

of most raw materials.30 However, Turkey is the main supplier of the critical raw material boron to the EU and Germany in particular: around 98 per cent of EU demand is met by Turkish production. Boron is strategically important because of its use in numerous key industries, including defence, aerospace and rocket fuels, specialised weapons as well as glass and ceramics, manufacturing, agriculture (for example, as a fertiliser), detergent production, nanotechnology, automotive engineering, energy technology, metallurgy and construction – in short, wherever hardness, chemical stability and heat resistance are required. Owing to its broad industrial use, boron is of considerable economic relevance; and security of supply is at high risk when there are delivery bottlenecks. In terms of reserves, Turkey is the global leader, with a share of around 73 per cent, ahead of Russia and the US.31

Turkey is also a supplier of agricultural products. In 2023, Germany imported agricultural products worth €1.8 billion from Turkey. That is the equivalent of 0.8 per cent of total German imports of agricultural and food products.32

German investments in Turkey

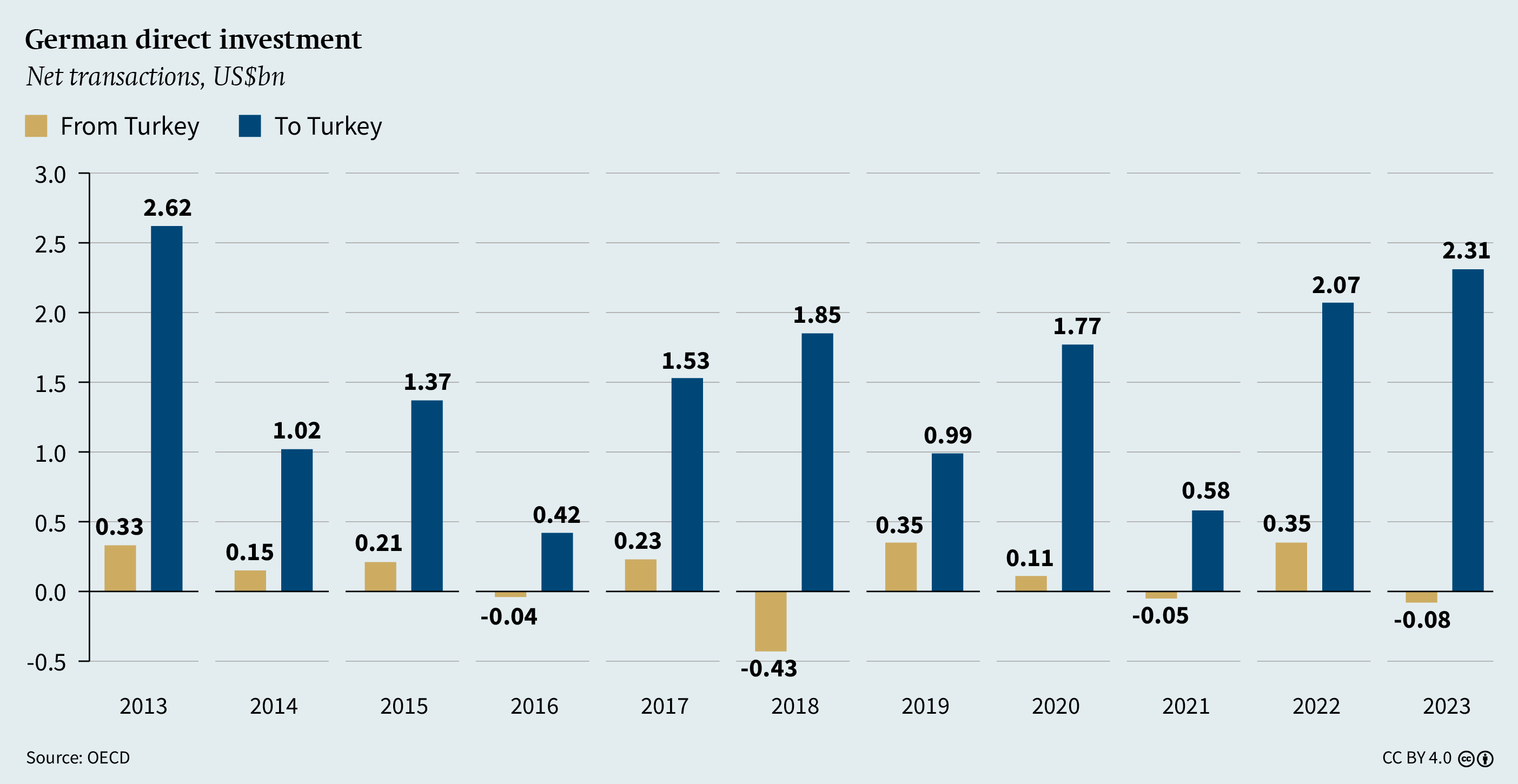

Germany is one of the most important countries of origin for foreign direct investment in Turkey – in terms of volume, duration of presence and number of companies (see Figure 6, p. 17). As of late 2024, German direct investment in Turkey since 1980 stood at almost US$14.5 billion.33 In 2023 alone, some US$687 million was invested by German firms (compared with US$972 million the previous year). As of August 2023, more than 8,000 companies with German capital investment were registered in Turkey, providing employment for more than 100,000 people. Most German direct investments in Turkey are transformative investments that have contributed to the creation of a large number of jobs.

German companies are represented in many sectors: industrial production, marketing, services and retail. For example, the North Rhine-Westphalian family business EJOT, which specialises in joining and fastening technology, invested €25 million in a new plant.34

Mercedes-Benz Türk has a bus plant in Istanbul and a lorry plant in Aksaray. While neither BMW nor Audi has its own production facilities in Turkey, both companies work with Turkish suppliers. As Europe’s fourth-largest car-manufacturing country, Turkey is an important procurement and supplier market35 for German car manufacturers.

Other major German companies in Turkey include the consumer goods and adhesives manufacturer Henkel, which has been operating in Gebze since 1963 and employs 750 people at three sites. The Bosch Group has a strong presence, too, with five subsidiaries and around 17,500 employees. And Deutsche Post has been active in Turkey for almost 40 years and plans to invest €135 million in a modern operations centre at Istanbul Airport.

All in all, Turkey is an attractive economic partner for Germany and a popular location for German companies. Cost advantages, a large sales market and good export prospects – for example, in automotive production – make the country interesting for major global companies like Mercedes-Benz.

Turkey’s other advantages include its geographical location at the crossroads of Europe, Asia and Africa, its relatively young population of 84 million, as well as its growing purchasing power, modern transport infrastructure, efficient logistics and dynamic and competitive private sector. Combined, all these factors offer German companies considerable growth opportunities.

Turkish companies in global value chains

Integration into global value chains has a significant impact on a country’s economic strength and prosperity, not least because it paves the way for efficiency gains and technology transfers. There are two pillars on which participation in global value chains rests, namely:

-

The import of input products (raw materials, intermediate products, expertise) and services that are used in production – both for the domestic market and for export (backward integration); and

-

The export of input goods and finished products as well as services that are consumed in the export destination country or go into production and are intended either for the domestic market or for export (forward integration).36

Countries participate in value chains directly via their own finished products and/or the export of input goods or indirectly via supplies for export companies on their own territory or abroad. Small and medium-sized enterprises (SMEs) are often indirectly involved in global value chains as suppliers.37 Participation in global value chains is determined by several factors, including the infrastructure and connectivity of a country or sector, the regulatory and business environment, the available factors of production and the size of the domestic market.

The involvement of Turkish manufacturing companies in global value chains has evolved over the years from limited participation through simple manufacturing products to an advanced role that can be measured by exports of input and intermediate goods. Between 1990 and 2015, Turkey’s participation in global value chains increased by 7 per cent.38 The year 2011 marked a turning point. Until then, backward linkage had dominated, with imported intermediate goods playing a central role in both production and exports; forward integration – whereby domestically produced intermediate goods account for a growing share of exports– became more important from 2011 onwards. Nevertheless, backward integration has remained high and followed a steep growth trajectory in recent years: in 2015, imported intermediate goods accounted for 30 per cent of total imports,39 while in 2022, imported intermediate goods represented no less than 80.4 per cent of total imports, capital goods 11.1 per cent and consumer goods 8.4 per cent.40

Turkey plays a significant role in several global value chains.

Turkey, accounts for around 1 per cent of global exports of goods and services, plays a significant role in several global value chains. Since around the mid-2010s, the growing importance of forward integration and the strong focus on manufacturing exports have helped Turkey move up from “basic manufacturing” country to “advanced manufacturing and services sector” country in the World Bank's classification. Thanks to its geographical location, Turkey has enormous growth potential within the framework of global value chains. Turkish companies have access to the EU’s internal market as well as to markets in Europe, Africa and Central Asia. However, gaining access to markets such as the US, Japan, China and Indonesia, which are protected by above-average tariffs, is more difficult.41

Turkish companies in German value chains

Turkish companies are integrated into German value chains in a range of sectors – from the procurement of raw materials through manufacturing and processing to design, marketing and sales.42 They are particularly well represented in the automotive, clothing, textile

|

Figure 7

|

Since around 2010, the participation of Turkish companies in German value chains in the textile industry has increased significantly. For example, Hugo Boss Textil, which employs around 4,000 people, and the clothing manufacturer s.Oliver have production facilities in Turkey. Turkish companies in the clothing industry are successfully integrated into both global and German value chains and cover all stages of production – from local procurement (of 70 per cent of raw materials) to final production. In 2022, the Turkish apparel industry recorded exports worth US$21.2 billion, with goods worth US$3.6 billion going to Germany.43

The forward integration of Turkish manufacturers into German supply chains is evident from the following list of exports from Turkey to Germany in 2023: parts and accessories for tractors (worth US$1.65 billion); motor vehicles for the transport of ten or more persons, parts and accessories, vehicles (excluding rail vehicles) and parts and accessories for those vehicles (US$4.99 billion); and electrical machinery, apparatus and appliances and parts thereof, sound recording and reproducing apparatus, televisions (US$1.35 billion).44

Turkish Industrial Policy: Challenges and Opportunities

Turkey’s industrial policy,45 which comprises a supply chain strategy and a decarbonisation strategy, integrates both horizontal and vertical measures. The horizontal measures include stabilising macroeconomic conditions, reducing macroeconomic imbalances, securing a competitive exchange rate, expanding human capital and improving the business environment. The vertical measures focus on the targeted promotion of selected sectors, in which the state intervenes by providing tax incentives, subsidies, trade policy protection and subsidised loans in order to strengthen the country’s strategically relevant industries.

Restructuring supply chains

The globalisation of economic cycles has led to companies relocating numerous stages of production to faraway countries. As a result, global value and supply chains have expanded significantly. Today, around 80 percent of global trade is based on such chains, providing for the livelihood of more than 450 million people.46 No later than since 2020 and the outbreak of the Covid-19 pandemic, this close international interdependence has been increasingly perceived as a risk; and there is now an acute awareness of the high susceptibility of the globalised economic system to disruption. Thus, cost efficiency is no longer the only guiding principle of entrepreneurial activity and economic policy strategies. Factors such as security, resilience and strategic autonomy are becoming markedly more important. And when business partners are being selected, it is political and normative criteria – such as reliability, stability and value-orientation – that are increasingly taken into account, alongside economic criteria.

Today’s extensive trade linkages have created dependencies that pose a security risk for the West – including the EU and Germany. As a result, there is now more focus on the diversification of supply chains, not least with regard to China. Accordingly, in Germany’s National Security Strategy, China is described as a “partner, competitor and systemic rival”.47 Major events such as the trade dispute with China, the Covid pandemic and Russia’s war of aggression against Ukraine have not only exposed the vulnerability of global supply chains; they have also raised questions about the supply of critical raw materials and energy dependency. Until recently, Russia was an important supplier of raw materials such as nickel, titanium and aluminium, all of which are central to Germany’s energy transition. For this reason, Germany and the EU have increasingly taken measures over the past few years to reduce their dependence on Russia.48

Among the top priorities of Germany and Europe are the reorganisation of supply chains and the security of supply for raw materials. The German government has resolved to expand existing partnerships in order to “build sustainable value and supply chains”, to “provide the necessary transport infrastructure for functioning supply chains” and to “make these [supply chains] more resilient in cooperation with the countries concerned”.49 With its industrial strategy – the EGD – the EU is pursuing not only the digitisation and decarbonisation of business locations but also the goal of strengthening of economic resilience through the reduction of dependence on imports of critical raw materials.50

In addition to disruptions in supply chains, rising freight costs51 are frequently cited as a reason for reorganising existing supply chains. In Germany’s automotive, pharmaceutical and aerospace sectors, the focus is on resilience and the reduction of dependencies on other countries,52 not least China and other authoritarian states. Companies in the chemical, information technology and automotive branches are endeavouring to relocate part of their production and investment away from China. This is where Turkey sees nearshoring opportunities for its industrial sector – something that is also in Germany’s interest.

In industrial policy, there are clear overlaps between Europe, Germany and Turkey.

Participation in global value chains is crucial for sustainable economic growth in Turkey. The Turkish government is pursuing an active industrial, trade, location and supply chain policy in order to benefit from the reorganisation of value and supply chains. The advantages offered by Turkey as a business location – such as infrastructure, an innovative industrial base and a variety of logistical options for trade with Europe – have helped form the country’s new industrial policy self-image.

It is important to point out that there are clear overlaps between European, German and Turkish industrial policy,53 mainly in the areas of promoting sustainable technologies and reducing CO2 emissions. Other overlaps can be identified in the integration of digital technologies into industry and the securing of market access for raw materials and primary products. Against this background, the German government and German companies are stepping up the search for partners to secure supply chains, while Turkey, for its part, sees opportunities for industry in its own country.

Goals of Turkish industrial policy

The long-term goal of Turkey’s industrial policy is the transition to a sustainable high-tech and services economy that is carbon-free. Both the Turkish government and Turkish companies are working to fulfil the requirements of the EGD and supply chain governance while driving forward the green energy transition. Although the decarbonisation strategies of Turkey and Germany are not fully aligned, there are many common goals. Turkey’s industrial policy prioritises economic stability, the promotion of innovation in key technologies and industries of the future (e.g., automotive, defence and energy) and the advancement of manufacturing and exports to strengthen competitiveness. A main concern here is the stabilisation of the macroeconomic base.

In this context, three separate sets of measures can be identified. First, Turkey has been pursuing a restrictive monetary and fiscal policy since June 2023 in a bid to curb inflation and currency depreciation. Under former Central Bank Governor Hafize Gaye Erkan and her successor, Yaşar Fatih Karahan, key interest rates have been gradually raised, while Finance Minister Mehmet Şimşek initiated the return to an orthodox economic policy. That policy includes prioritising monetary stability, limiting exchange rate interventions and abolishing currency-protected savings deposits. However, there has been only limited success so far: inflation remains high and the sustained confidence of international investors has not been regained.54 Second, Turkey is focusing on import substitution, export promotion and structural adjustments. Third, it plans to improve the general conditions for companies and promote research and development (R&D) through subsidies.

The long-term goal of Turkey’s industrial policy is that the country plays a role in what has been dubbed the “Fifth Industrial Revolution”. Industry 5.0 stands for a new way of production based on technologies such as artificial intelligence (AI), the 5G mobile communications standard, voice control systems and digital reality, which paves the way for developments such as autonomous vehicles and smart homes and cities. In Turkey, the National Technology Movement and the Industry and Technology Strategy 2023 provide guidance for a progressive technology policy in the context of the Fifth Industrial Revolution.55 Moreover, an Industry 5.0 centre has been established to promote technological development in Turkey. There are also plans to intensify cooperation between the public and private sectors to develop and advance technological innovations. Experimental workshops have been set up in 30 provinces so that these plans can be implemented in various regions of the country.

Also important is the need to prepare the 68,000 or so factories in Turkey for industrial modernisation in the short, medium and long term. In this context, the restructuring of the 353 organised industrial zones appears promising. The technological renewal and redesign of production facilities, industrial parks and urban areas will play a central role, especially for technical colleges and universities as centres of knowledge and innovation. And it will create opportunities for German and European companies to cooperate and sell their products. Forecasts by the IMF and the auditing firm PricewaterhouseCoopers for the years 2030 and 2050 suggest that in future, Turkish industry will account for a much larger share of global production than it does today.56

In its medium-term economic programme for the period 2024–26, Turkey is focusing on technology-intensive production with high added value. Other goals include increasing industrial investment, reducing import dependency and promoting technology partnerships. At the same time, the green and digital transformation is to be advanced, domestic production capacities expanded and R&D supported as part of the effort to ensure sustainable growth. Moreover, the programme aims to promote high-quality and large-scale investments and increase export capacities in order to strengthen Turkey’s global competitiveness. Finally, the strategic objectives also include improving the investment climate and facilitating access to finance for industry.

Goals of Turkish energy policy

In its energy policy, the Turkish government is increasingly pursuing new approaches. The goal is to establish itself as a reliable energy partner for Europe; and to this end, it is making targeted investments in clean energy technologies. The gradual move away from fossil fuels not only has economic benefits but also strengthens the country’s rapprochement with Europe in the area of energy policy; however, establishing a sustainable energy partnership with Europe presents formidable challenges for Ankara. Turkey’s high dependence on gas imports from Russia, Iran and Azerbaijan pushes up the current account deficit and makes the country vulnerable to external shocks and price fluctuations on the energy markets. Overall, Turkey’s energy policy is shaped by both domestic- and foreign-policy considerations and is increasingly reactive to geopolitical dynamics. From a foreign-policy perspective, Ankara is focusing on three main goals: meeting the growing demand for energy, diversifying energy sources and reducing CO2 emissions.57

In its bid for greater energy sovereignty, Turkey is expanding wind and solar energy and investing in nuclear and coal power.

For decades now, Turkish governments have been seeking to diversify the country’s energy portfolio in order to secure affordable and reliable energy supplies. Among other things, Ankara has invested heavily in locally produced energy, including the development of natural gas fields in the Black Sea. It also wants to establish itself as a natural gas hub between producer and consumer countries – a project that is geostrategically plausible but could clash with the international decarbonisation agenda over the long term.58 The drive to diversify energy sources is also evident from investments not only in locally generated energy sources such as wind and solar energy but also in the expansion of nuclear and coal-fired power plants. The latter, however, are clearly at odds with the aforementioned decarbonisation agenda as they cause high CO2 emissions and delay the transition to a low-carbon energy system.59 Turkey’s foreign-policy strategy of diversification has led to numerous international partnerships: the country maintains close relations with Western buyers of its energy exports as well as with major energy suppliers such as Russia and other energy providers such as Azerbaijan, Iran and Iraq.

In the current political discussion, a less transactional relationship between the EU and Turkey is being sought. For its part, the EU has identified the energy sector as a potential area for closer cooperation. To date, EU-Turkish energy cooperation has focused primarily on natural gas trading. With increased EU demand for natural gas and the discontinuation of the Russian gas trade, Turkey is a potential alternative source of the fossil fuel. Since 2020, the country has contributed to Europe’s energy supply security through the Southern Gas Corridor. The backbone of this project is formed by the Trans-Anatolian Gas Pipeline (TANAP) and the TurkStream natural gas pipeline, which have a combined capacity of 31.5 billion cubic metres. (Natural gas reaches Turkey via the first pipeline and European countries are supplied via the second.) Moreover, the Turkish Straits are important for global energy security, as around 3 per cent of the world’s oil demand is transported via this route.60

In the medium to long term, the natural gas trade is expected to become less relevant – a development that would be compatible with the goals of the EGD and the international decarbonisation agenda. Low-carbon energy sources and carbon-free electricity could be the mainstay of future energy relations between Turkey, the EU and Germany. Going forward, the energy partnership between Germany and Turkey will gain in importance. However, this does not mean that the current political obstacles will have been removed.

Energy transition and decarbonisation

The EU directives on green foreign direct investment are contributing to the decarbonisation of the Turkish economy in two ways: by encouraging investment in renewable energy and by bringing Turkey into line with European green investment standards. Since more than 40 per cent of Turkish exports are bound for the EU, both the EGD regulations and guidelines are expected to have a transformative effect on Turkey’s industry. In addition to investing in clean energy, emission-intensive sectors such as construction, heavy chemicals and textiles will have to green their production and logistical operations if they want to maintain or expand their trade relations with EU countries.61

There are four Turkish programmes that are particularly relevant for the harmonisation of the country’s legislation with that of the EU:

-

The medium-term economic programme for the period 2025–27 focuses on reforms in the public finances, combating informality (the shadow economy), promoting research, development and innovation, pushing ahead with the transition to a green and digital economy and improving the business and investment climate. Among other things, the financial reform aims at increasing the efficiency of public spending, enforcing budgetary discipline and reducing the public debt in order to achieve long-term economic stability.62

-

The Turkish government’s action plan on the EGD, published at the end of 2021, has enabled the country to adapt to international climate-protection policies. The plan also aims to promote Turkey’s integration into global supply chains and attract green investments.63

-

Until now, Turkey’s climate targets have been criticised as weak and non-binding. But the planned introduction from 2026 of an emissions trading system (ETS) in Turkey promises a turnaround. Ankara has transferred responsibility for climate protection to the Ministry of the Environment and set up its own climate department. The ETS project is supported by the World Bank.64

-

Turkey aims to replace its gas imports with domestic renewable energies. The National Energy Plan for Renewable Energies,65 together with the Hydrogen Strategy, provides an initial insight into how this might be achieved. The goal is to increasingly meet energy demand from domestic sources and reduce dependence on gas and coal. The government is focusing on hydropower and wind power, the expansion of nuclear power and the further exploration of oil and gas fields.

The energy transition in Turkey is being driven mainly by investments in renewable energies and decentralised energy systems, with sustained economic growth and rising demand for energy as supporting factors.66 But despite the progress already made, the measures taken so far have had only a limited impact: greenhouse gas emissions have risen by around 157 per cent over the past three decades. This is due primarily to the expansion of the energy, industry and transport sectors as well as climate-related factors such as drought and high temperatures. Turkey’s electricity generation is still based largely on fossil fuels: in 2022, the combined share of coal and natural gas was some 58 per cent (35 per cent and 23 per cent, respectively) while the share of renewable energies was around 38 per cent.

In general, Turkish entrepreneurs and experts are positive about the planned expansion of nuclear power as a contributing factor to decarbonisation. However, the withdrawal from fossil fuels has been slow so far. All in all, these developments show that while the transformation towards a sustainable energy system is under way, the structural dependence on fossil fuels remains a key challenge for Turkey’s energy and climate policy.67

Another point of criticism is the lack of clarity over the roadmap for the net-zero emissions target. Investors often demand a concrete plan. In particular, the transport sector, which is responsible for a large proportion of CO2 emissions, has come under scrutiny. Experts argue that more transport should take place by rail.

Meanwhile, the Energy Plan 2035 is generally regarded as positive by experts and economic actors alike, even if some have expressed doubts about its feasibility and financing. For their part, company representatives regard the hydrogen targets and decarbonisation plans through electrification and hydrogen use as not yet sufficiently concrete.

|

Figure 8

|

In accordance with the 2022 amendment of Article 88 of the Turkish Commercial Code, the Public Supervision, Accounting and Auditing Standards Authority was tasked with drawing up standards for sustainability reporting. On 1 January 2024, the legal obligation to report on sustainability was introduced. This applies to companies that have a balance-sheet total of more than 500 million Turkish lira, an annual net turnover of more than 1 billion Turkish lira or more than 250 employees. There are no thresholds for banks, all of which are obliged to report. The provision of climate and sustainability information must be oriented towards the period of annual financial reporting and the company’s future financial adequacy. In addition, general framework conditions, such as sustainability practices, objectives and implementation strategies, must be taken into account, along with climate- and environment-related disclosures and financial data related to sustainability and its impact. Finally, the management and control system needs to be reviewed, particularly with regard to the management of sustainability processes and the quality of reporting.68

According to Turkey’s hydrogen strategy, the share of that gas in the energy mix is to be increased by 2053 so that the net zero emissions target can be met by then. Within the same time frame, the production costs for green hydrogen are to be significantly reduced.69

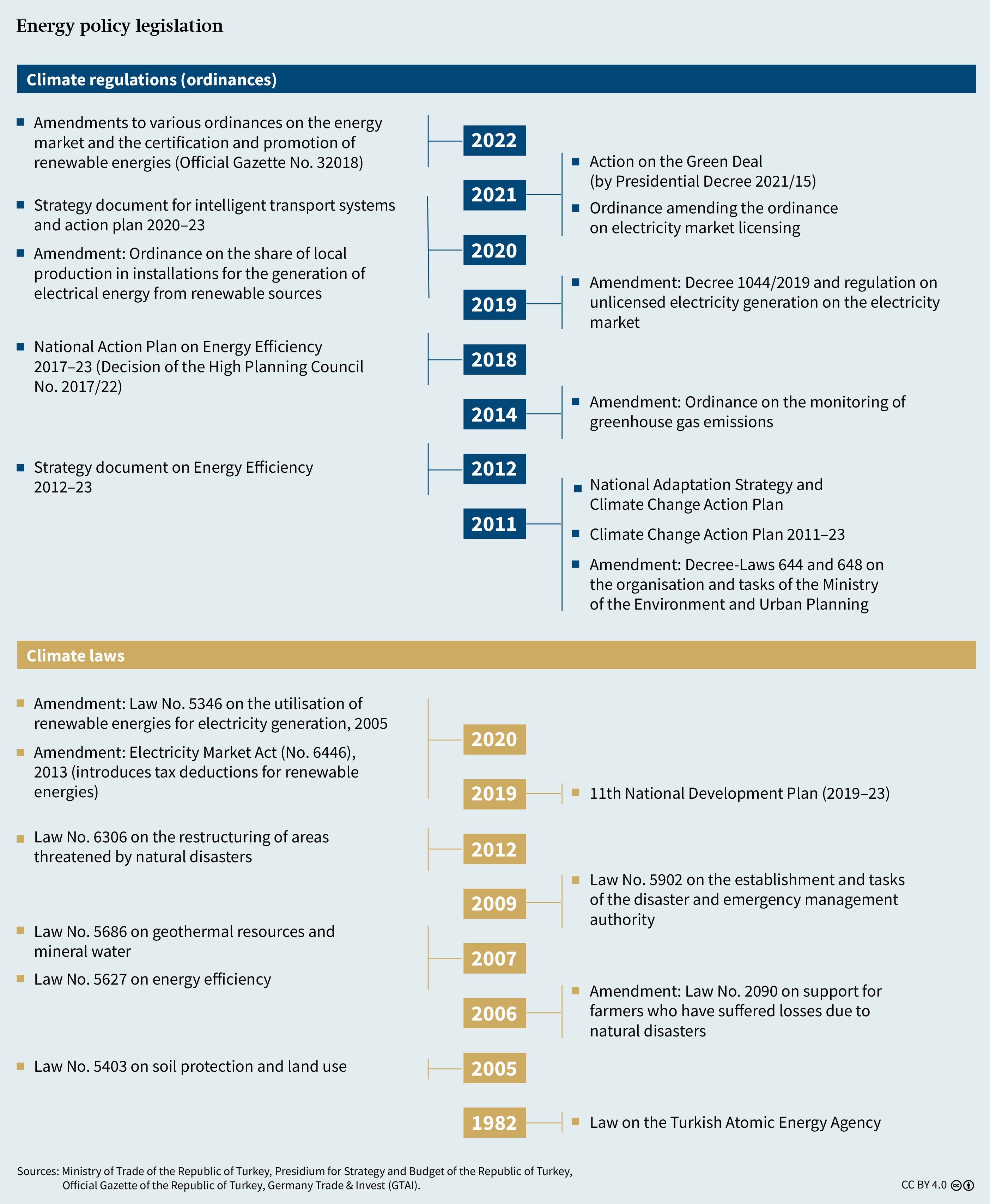

Meanwhile, Turkey has already enacted legislation and regulations on climate change, including the Renewable Energy Law (No. 5346) and the Green Deal Action Plan. In November 2022, amendments to the renewable energy regulations on energy storage went into force. Act No. 5627 of 2007 forms the basis for measures in the area of energy efficiency.

European Green Deal and CBAM: Blessing or curse?

Through the EGD, the EU wants to play a pioneering role in climate protection worldwide – an ambition that has a material impact on its trading partners. Adopted by the European Commission in 2020, the EGD aims for a 55 per cent reduction in greenhouse gas emissions by 2030 and the establishment of climate neutrality by 2050. Earlier, the Paris Climate Agreement, which was signed by 195 countries, stipulated that climate change is to be mitigated through targeted measures and the global economy reorganised in a climate-friendly way. The agreement identifies three main goals: limiting the rise in the global average temperature, reducing emissions and adapting to climate change while channelling financial resources in line with climate protection goals.

The goal of curbing climate change by 2050 involves limiting global warming to a maximum of 1.5 or 2.0 degrees Celsius compared with pre-industrial times. In order to achieve that goal, a balance needs to be established between emissions of climate-damaging gases and the amount of carbon removed from the atmosphere in carbon sinks. This means the global economy must be decarbonised quickly and consistently over the next quarter of a century. At the 27th UN Conference of the Parties (COP27) in Egypt in 2022, Turkey tightened its emissions reduction target for 2030 from 21 per cent to 41 per cent compared with a business-as-usual scenario – which, in effect, still means an emissions increase of around 34 per cent compared with 2020. Specifically, emissions in Turkey are expected to rise from 523.9 million tonnes of CO2e (in 2020) to 700 million tonnes in 2030. Ankara does not expect emissions to peak until 2038.70

Under the EGD, Turkish companies must harmonise their standards with European ones.

The need to adapt to European environmental and climate-protection standards and supply chain due-diligence requirements is acknowledged in Turkish business and political circles. In this context, a high-ranking Turkish diplomat emphasised the strategic importance of deeper economic integration with the EU, particularly through the modernisation of the customs union and the resumption of accession negotiations. The EU can play a dual role here: as an external “disciplining agent” and as a transformative force that initiates institutional reforms in Turkey. In the diplomat's view, compliance with the Copenhagen criteria is hardly possible without external support. For Turkey, the EGD is not only an environmental challenge but also a structural one. Turkish companies feel increasingly obliged to harmonise their production and supply chain standards with European ones. The same diplomat warns of the negative consequences of economic exclusion: if Turkey were to be excluded from the EU’s €800 billion economic stimulus programme NextGenerationEU – which aims to promote climate-neutral and sustainable economic structures – it would suffer serious structural disadvantages.

|

In June 2023, Orhan Turan, the president of the Turkish Business Association TÜSİAD, stressed the importance of close cooperation between Turkey and the EU in the effort to achieve net zero targets. In view of the growing geopolitical and geoeconomic uncertainties, he called for a joint roadmap to establish a stable, resilient and sustainable international order. He emphasised the need to modernise the customs union71 and the crucial importance of the rule of law and democracy for the deepening of bilateral relations. 72 TÜSİAD Vice-President Ozan Diren spoke out in favour of reviving the integration partnership and modernising the customs union. And in interviews conducted for this research paper, TÜSİAD representatives Dilek Aydın (Brussels office) and Alper Üçok (Berlin office) emphasised the importance of a strategic reorientation of relations between Ankara and Brussels; above all, they pointed to the need to resume political talks and, like Turan and Diren, called for modernising and expanding the customs union. As for the EGD, experts and economic actors recognise that its requirements with regard to standards could affect the competitiveness of Turkish industry in the short term. However, in the long term, the EGD is seen as a catalyst for comprehensive economic transformation and sustainable development.

The EGD has been fleshed out with a series of laws and guidelines that form the regulatory framework of the deal. Within that framework, German companies are obliged to systematically review the environmental and sustainability practices of their Turkish trading partners and suppliers.73

Carbon Border Adjustment Mechanism

The Carbon Border Adjustment Mechanism (CBAM) is part of the EU’s “Fit for 55” package.74 It obliges companies that import emission-intensive goods into the EU to purchase CBAM emission allowances, which offset the difference between the CO2 price in the country of origin and that in the EU emissions trading system. The mechanism, which affects a wide range of industrial and commercial companies, is being gradually introduced as of October 2023 so that enterprises within and outside the EU can be brought into line with the emissions reporting obligations and calculation methods of the EU ETS. In this initial stage, the mechanism covers electricity, cement, iron and steel, aluminium, fertilisers and hydrogen – all sectors with particularly CO2-intensive production processes, which pose a high risk of carbon leakage. Turkey will be severely affected by this EU policy. As mentioned above, more than 40 per cent of its exports go to the EU, especially energy-intensive goods such as aluminium and iron and steel, which are subject to the CBAM regulation. According to modelling, if the CBAM is applied to Turkish exports at a carbon price of €150, the growth rate of the Turkish economy would decrease by 0.04 per cent until 2032, while it would be boosted by 1 per cent at a carbon price of €50.75 This means that energy-intensive sectors of the Turkish economy will be the first to have to push ahead with CO2 savings and a green transition.76

Turkish steel exports are particularly affected by the introduction of the CBAM, as around one third are bound for EU countries. In 2023, Turkey exported steel, iron and other metal products worth US$2.82 billion to Germany. Because Turkish exporters of such products will have to reduce their CO2 emissions in order to remain competitive, there will be new business opportunities for German suppliers of emission-reduction solutions – for example, through the use of new technologies or production processes. Furthermore, alternative materials could contribute to decarbonisation by reducing the use of energy-intensive metals. The next stage of phasing in the CBAM could have an impact on other Turkish industries, such as the automotive and supplier industry (exports to Germany worth US$1.63 billion in 2023), mechanical engineering (exports to Germany worth US$4.5 billion in 2023) and the construction industry.77

Economic policy and regional challenges

Combined with the political and economic instability in Turkey, regional events such as Russia’s war of aggression against Ukraine, the conflict in the Middle East, regime change in Syria and the growing confrontation between Israel and Iran pose enormous challenges for German-Turkish trade and supply chain integration.

Cooperation with Russia and China is fuelling speculation about Turkey’s geopolitical orientation.

The drastic devaluation of the Turkish lira and persistently high inflation make day-to-day business difficult for German companies and their Turkish partners. Rapidly changing prices of goods and services are risk factors that require the constant adjustment of business strategies – for example, hiking wages to keep pace with inflation – in order to ensure business resilience.78 Moreover, controversies over Turkey’s geopolitical orientation weigh on the investment climate. German companies operating in Turkey note that speculation about Ankara turning away from the EU has triggered uncertainty and is having a negative impact on their investment decisions.79

The current speculation about Turkey’s geopolitical realignment is being fuelled by the country’s rapprochement with Russia and China. Turkey is dependent on Russian natural gas while the construction of Turkey’s first nuclear power plant in cooperation with the Russian state-owned company Rosatom is creating a new structural dependency on Moscow. At the same time, China is gaining economic influence: Turkey is dependent on cheap imports from China and the plans of Chinese electric car and battery manufacturer BYD to build an automobile plant on Turkish soil by the end of 2026 could lead to the growing dependence of Turkish industry on China. Nevertheless, Europe – as a sales market and source of investment – remains a central pillar of Turkey’s macroeconomic stabilisation.

Modernising the customs union could help clarify Turkey’s geopolitical and security policy orientation and send an important signal to German companies. Potential investors would be encouraged to become involved in Turkey and new impetus would be given to existing trade relations and cooperation. Expanding the customs union to cover agricultural products and services – including e-commerce – would generate additional trading profits, increase economic prosperity and create diverse opportunities for German and Turkish companies to cooperate.80 In Germany, there is currently reluctance to modernise the customs union, not least owing to the Turkish government's latest moves against the opposition. Although Turkey is recognised as an “important trade and economic partner”, it is accused of not fully enforcing the customs union regulations. As long as this is the case, further steps to modernise the customs union appear to make little sense, according to a German government representative. Ankara’s persistent refusal to implement the customs union regulations with regard to Cyprus is seen as the biggest obstacle. From the perspective of many German economic players, there is no “urgent need” for an extended free-trade agreement with Turkey right now.81

The legal and planning uncertainty, together with restricted market access, is slowing down investment.

Jürgen Schulz, the German ambassador to Ankara from 2020 to 2024, explained in a 2024 interview with the Turkish business newspaper Ekonomim that German companies in Turkey are largely satisfied with the current situation but newcomers are hesitant to make investment decisions. The main reasons cited were the unattractive investment conditions – above all, the lack of legal, planning and financing security. German entrepreneurs in Turkey also note barriers to trade and investment.82

In late 2024, TÜSİAD President Turan emphasised the shortcomings of the Turkish legal system and highlighted the need – including with regard to the economy – for the rule of law to remain intact and for an effective judicial system and a functioning democracy. He also noted that in order to keep pace with change, it is essential to guarantee legal certainty, abide by market economy principles and strengthen the independence of institutions.83 Scepticism among German economic actors towards Turkey is prompting companies to seek new suppliers, for example, in Bulgaria or Romania.84 Further challenges arise from the EGD and CBAM as well as from European and German supply chain governance, which is discussed below.

To sum up, it is evident that there are numerous overlaps between the industrial policies of the EU, Germany and Turkey, particularly in the areas of sustainable technologies, CO2 reduction and digital transformation. Moreover, there is a shared goal of securing access to raw materials and primary products. Turkey sees this as an opportunity to strengthen its industrial sector through stable and reliable partnerships within global supply chains. From both official strategy/position papers published by ministries and business organisations and discussions involving political and economic actors, it can be seen that there is growing awareness of what seizing this opportunity entails.85 Also, there is a broad consensus that sustainable economic development in Turkey is possible only if Turkish industry meets European environmental and sustainability standards, especially those stipulated by the EGD and the governance requirements of German and European supply chain legislation.86 Nevertheless, some main goals of Turkish industrial policy have still not been achieved.

Since June 2023, Finance Minister Mehmet Şimşek has been pursuing an orthodox, restrictive monetary policy, primarily in order to curb persistently high inflation. This move has been largely welcomed by economic actors, as it is seen as a necessary correction to the earlier highly expansionary and unconventional economic policy. But there are significant doubts about the sustainability of this monetary policy course, not least because of the suspected intervention of President Erdoğan. Moreover, it has not yet been possible to build up the trust of international investors and domestic economic players. Nor has there been any significant correction of the serious macroeconomic imbalances – including the high inflation rate, the persistent current account and trade deficits and the fragile monetary-policy environment overall, high key interest rates notwithstanding.

Furthermore, despite legislative initiatives such as the planned introduction of an ETS, independent assessments show that Turkey has so far failed to meet its self-imposed climate targets. The continued expansion of coal-fired power plants is clearly at odds with achieving those targets. Because of their high CO2 emissions, Turkey’s power plants are a major obstacle to its transition to a low-carbon energy system. The Climate Action Tracker rates the measures taken by Ankara to meet its net-zero target for 2053 as “insufficient” – those implemented to date, along with the emission reductions planned by 2030, do not suffice to fulfil the requirements of the Paris Climate Agreement, even though climate policy is becoming more important at the institutional level. According to international analyses, significant improvements are necessary for the net-zero target to be achieved by 2053.

Turkish Supply Chain Policy: Shortcomings and Prospects

In this paper, supply chain policy is understood to comprise the strategies, measures and national legislation implemented by the government as well as their alignment with international agreements and global standards. The focus here is on the promotion of the export economy, compliance with international trade standards and the creation of favourable framework conditions for foreign investors.

Turkey’s supply chain policy

The two main pillars of Turkey’s supply chain policy are the economic framework conditions and export orientation. The country pursues an export-oriented economic policy in a bid to establish itself as a production centre and supplier of industrial goods in Europe, Asia and the Middle East. The establishment of industrial and free trade zones to promote trade and production activities plays a key role. Companies operating in these zones receive tax concessions and are subject to fewer regulations. The zones themselves are not only attractive locations for enterprises but also important hubs in global supply chains.

Labour and environmental protection laws are essential for setting standards. Turkey has enacted national laws on occupational health and safety and on labour rights compliance that are based on the standards of the International Labour Organization of the United Nations. But violations are frequently documented, especially in the textile and agricultural industries.87 Turkey also has an environmental code that regulates waste disposal, emissions and the protection of natural resources. However, shortcomings in the rule of law as well as political dependencies and inefficiencies in the Turkish judiciary are hampering supply chain integration.

The EU-Turkey Customs Union, which facilitates the movement of industrial products, went into effect in 1996. As part of the EU accession negotiations, Ankara has committed to implementing EU standards in areas such as labour protection and environmental protection.88 This has consequences for supply chain requirements and production conditions in Turkey. Companies in Turkey’s export-oriented sectors face demands from international customers that due diligence obligations are met along the supply chain. Some Turkish companies that export to Europe have voluntarily signed up to international standards such as the ISO standards and social accountability certification (e.g., SA8000 or BSCI), which boosts their competitiveness in international supply chains. Turkey complies with the above-named standards as well as the labour and environmental norms, particularly in sectors with international clients.89

German and European supply chain governance

Supply chain governance refers to a regulatory framework of national and supranational binding requirements for companies to comply with human rights and environmental due diligence obligations along the entire length of global supply chains. Germany’s Supply Chain Due Diligence Act (LkSG), which has been in force since 1 January 2023, provides the relevant legal framework at the national level and the Corporate Sustainability Due Diligence Directive (CSDDD), which the European Parliament voted initially to adopt in June 2023, will do so at the European level. After a temporary setback, the latter was adopted by a qualified majority in the EU Council in a second vote in March 2024 and was finally adopted by the European Parliament and Council in May 2024. The deadline for implementation is June 2028. Because of the primacy of EU law over national law, Germany is obliged to transpose the CSDDD into national law within two years of its entering into force. Both the German and the European directives are under scrutiny: while the LkSG is the subject of controversial debate, particularly with regard to the issues of implementation, bureaucratic outlay and the burden on SMEs, the CSDDD must now be implemented in the member states in a standardised and effective manner and its practical application determined.90

Supply chain governance requires companies to uphold human rights and environmental standards. They must demonstrate that they are actively identifying risks and taking measures to minimise them.91 In accordance with the CSDDD, European companies must also ensure that human rights, biodiversity and the environment are protected.92 Germany’s Federal Office of Economic Affairs and Export Control (BAFA) monitors implementation and imposes fines and sanctions in the event of violations. While the German law applies mainly to sites in Germany and direct suppliers, the European law extends to upstream and downstream activities, including indirect suppliers. Further, the EU directive imposes a duty of care on companies throughout the entire length of the supply chain; this also applies to transport, storage and disposal carried out by the business partners, whereby sellers and consumers are not taken into account.93 By contrast, the LkSG provides only for the proactive scrutiny of direct suppliers and the reactive scrutiny of indirect suppliers. Lastly, the new EU regulation introduces civil liability for companies; under certain conditions, trade unions and non-governmental organisations can assert claims on behalf of injured parties within five years.

Turkish economic players – including entrepreneurs and representatives of leading associations such as TÜSİAD and the Union of Chambers and Commodity Exchanges of Turkey (TOBB) – regard German supply chain governance as part of the overall European architecture of supply chain legislation, industrial policy and the EGD. This “regulatory package” is seen as providing a strategic framework that requires significant adjustments to be made but at the same time opens up opportunities for the deeper integration of Turkey into European value chains. Because of the carbon-intensive structure of the Turkish economy, companies anticipate rising costs owing to the CBAM; therefore, comprehensive integration into green value chains – for example, wind and solar energy – is considered essential. Moreover, TÜSİAD and TOBB believe the EGD offers the chance to increase the competitiveness of Turkish products on the EU market. Turkey has comparative advantages in several industrial sectors that could be utilised to cushion the negative impact of the CBAM and initiate structural reform processes.94

Areas of cooperation: Energy, automotive and defence

Cooperation with Germany is particularly important in three areas of the Turkish economy: the energy, automotive and defence industries. Against the backdrop of climate policy objectives – especially decarbonisation – cooperation in the first two areas is most promising. In the automotive sector, there is more forward than backward integration into German supply chains and in the energy sector the two are more or less balanced. However, in the defence industry, backward integration predominates: Turkey is still dependent on input goods and technological expertise from abroad, including Germany. Closer cooperation in the energy and automotive sectors could strengthen Germany’s security of supply, while in the area of defence, Turkey would benefit from technology transfer.

The German-Turkish energy partnership

The German-Turkish Energy Forum has been held regularly since 2011. The sixth such event, which took place in Berlin in November 2024, was attended by then German Minister of Economic Affairs Robert Habeck and Turkish Minister of Energy and Natural Resources Alparslan Bayraktar. The highlight was the signing of a declaration of intent to intensify bilateral cooperation, along with a cooperation agreement between the Turkish energy company Enerjisa and Hamburg University of Applied Sciences on research projects in the areas of green hydrogen and renewable energies.95

Hydrogen production, which offers promising investment opportunities in Turkey, could turn the country into a major green-energy hub. This would not only reduce dependence on Russian natural gas but also contribute to Europe’s energy security. At the same time, the EU would come closer to achieving its climate targets as part of the energy transition. Moreover, green hydrogen plays a key role in German industry’s effort to achieve climate neutrality; and hydrogen imports from Turkey could make an important contribution here. Germany is already supporting Turkey to the tune of €200 million to promote renewable energies and develop a hydrogen economy.96 And as part of the International Climate Initiative, €20 million have been made available to Turkey for innovative climate-protection measures, whereby the focus is on increasing energy efficiency.

Automotive and defence industry

Turkey continues to be an important automotive market for the EU. The Turkish automotive industry is highly integrated into German and European supply chains. China is unlikely to overtake Europe as the most important market for Turkish cars and car parts; however, as noted above, the People’s Republic will play an increasing role in the Turkish automotive market. The Chinese car manufacturer BYD’s plans97 to open a production facility in Turkey by the end of 2026 is aimed at circumventing EU tariffs on electric vehicles and gaining duty-free access to the EU. Meanwhile, the launch of the sale of China-made electric vehicles in Turkey – BYD planned to sell 10,000 electric vehicles in Turkey in 2024 – could help boost the sales of the Turkish electric car manufacturer Togg and lead to the expansion of the charging and servicing network in Turkey. On the other hand, there is the risk that Turkish car production will be negatively affected and Togg’s market share reduced. Moreover, the closer integration of the Turkey’s automotive industry with that of China threatens putting further strain on Turkish-European relations. Above all, closer economic ties could result in trade deficits and greater dependence on China. And a strategic reorientation of the Turkish automotive industry towards China could have a considerable negative impact on the competitiveness of the European industry.

Amid the tech rivalry between the US and China, Turkey is pursuing a balancing strategy.

Amid the technical and political rivalry between the US and China, Turkey is performing a balancing act in its relations with the two superpowers. Although Turkey is allied with the West, it also maintains strategic relations with China and has entered into technology partnerships, including in the area of 5G. Turkey’s stance is to be seen against the background of the technology transfer and export restrictions that the US and some EU states have imposed on Turkey. These include a regulation introduced by the Biden administration in the field of AI stipulating that Turkey (along with many other countries around the world) is to receive only limited access to advanced AI technology. At the same time, Turkey fears that the second Trump administration ceasing to abide by World Trade Organization rules would create an unpredictable international trade environment that would also affect it.

As noted above, the defence industry is integrated into German supply chains mainly via the import of inputs and technology (backward integration). After decades of investments and reforms, the Turkish defence industry has developed into a serious player on the international defence market; however, the participation of Turkish defence companies in international programmes is limited owing to the volatile nature of Turkish politics. The war in Ukraine further limits Turkey’s options: previously, there was the option of cooperation with Russia in the area of defence, but that is no longer possible since Russia launched its war of aggression on Ukraine.

In recent years, Turkey’s interest in defence industry cooperation and involvement in arms programmes under the auspices of NATO has increased. At the same time, Ankara is seeking to improve its foreign policy and defence industry relations with its Western partners amid financial constraints. The Turkish defence industry, particularly in the field of drones, is closely coordinated with the US and NATO. The Turkish defence company Baykar, which manufactures the Bayraktar TB2 combat and reconnaissance drone, ensures its technology meets NATO standards. If Turkey and Europe were able to redefine their relations by adapting to the new geopolitical landscape, enormous potential for mutually beneficial defence-industrial cooperation could be unlocked.98

Conclusions and Recommendations