Loans for the President

External Debt and Power Consolidation in Egypt

SWP Research Paper 2022/RP 12, 14.12.2022, 33 Seitendoi:10.18449/2022RP12

Forschungsgebiete-

Egyptian President Abdel Fatah al-Sisi has consolidated his authoritarian regime in recent years. This has been accompanied by a significant increase in Cairo’s foreign debt, which more than tripled between June 2013 and March 2022.

-

The country’s debt policy was directly linked to the presidential centre of power. The government managed a well-choreographed mix of incentives, threats, and concealment that made it possible to take out more and more new loans.

-

The Egyptian military, on whose support President Sisi is dependent in order to assert his claim to power, is the main beneficiary of the debt policy. External debt helped to protect the revenues and assets of the armed forces, to finance major projects in which they could earn significant money, and to pursue an expansive military build-up.

-

The instrumentalisation of debt policy for power politics increases the risk that Egypt will no longer be able to service its liabilities in the future.

-

Above all, however, the misallocation of scarce financial resources undermines the socio-economic development of the country and promotes police-state repression. The latter, in turn, favours the political instrumentalisation of debt policy for power politics, as it prevents any control of government action.

-

In the future, Germany and its European partners should therefore tie bilateral lending as well as support for Egypt in its negotiations with international financial institutions to two conditions: firstly, the dismantling of military economic activities – whereby the assets of the armed forces must also be disclosed – and secondly, concrete steps towards ending police-state repression.

Table of contents

2 The challenge: Foreign debt to consolidate power

3 The actors: The president and his technocrats

4 The instruments: Carrots, sticks, and obfuscation

4.2 Investment incentives and government contracts

4.3 Linkage with other policy areas

4.4 Concealment of the actual debt situation

5 The profiteer: The military and its economic empire

5.1 Protection of revenues and assets of the armed forces

5.2 Loan-financed infrastructure projects

5.3 Loan-financed arms expenditure

Issues and Recommendations

Since the military took power in Cairo in summer 2013, former army chief and current president Abdel Fatah al-Sisi has successfully expanded his rule. The consolidation of his authoritarian regime has been accompanied by a significant increase in Egypt’s foreign debt. As a result of aid from international financial institutions, intergovernmental loans, and the issuance of government bonds on the international capital market, this has more than tripled between June 2013 and March 2022, raising the external debt-to-GDP ratio from 15 per cent to approximately more than 35 per cent. And there is no end in sight. Due to expected balance of payments problems, in March 2022 Egypt again had to ask the International Monetary Fund (IMF) for help – for the fourth time in six years. At the end of October, the IMF announced a staff-level agreement with the Egyptian government on a new reform programme to be supported by a 46‑month Extended Fund Facility Arrangement of US$3 billion.

This study examines the relationship between the consolidation of power and foreign debt policy. The question is raised of how the government of a highly indebted country such as Egypt was able to obtain loans on such a large scale and dispose of them largely at its own discretion. The answer can be found in the well-choreographed approach of the Egyptian government, which relied on a policy mix of incentives, threats, and concealment. This included partial economic reform concessions to international financial institutions as well as lucrative state contracts to foreign companies, the instrumentalisation of other policy fields, and the concealment of the actual debt situation. The operational prerequisite for this was the close connection of debt policy to the presidential power centre and the appointment of experienced technocrats with excellent international connections into important positions.

The Egyptian military, on whose support President Sisi was directly dependent to consolidate his power, was a main beneficiary of the borrowing. Thanks to external loans, the government did not have to access the assets of the armed forces to finance budget deficits. Moreover, the army benefited from public contracts for infrastructure projects, which were also enabled, at least in part, by loans. And finally, external borrowing facilitated the country’s excessive rearmament. Despite scarce state resources, Egypt has risen to become the third-largest arms importer worldwide in recent years.

For Germany and its European partners, this development is problematic for two reasons. On the one hand, the instrumentalisation of debt policy for the sake of power politics is economically unsustainable. The increasing risk that Egypt will no longer be able to service its liabilities in the medium and long term would also financially affect a number of European states. For Germany, Egypt is now the largest debtor among the developing countries, measured in terms of claims on development aid loans. Added to this are extensive budget support and, above all, a considerable indemnification risk that the federal government takes on when securing export credits. The latter could rise to a volume of up to €10 billion in the medium term, as Berlin is granting new loan guarantees to support the expansion of Egypt’s railway infrastructure by Siemens.

On the other hand, the flagrant misallocation of scarce financial resources hinders the socio-economic development of the most populous country on the Mediterranean with more than 100 million people. Available funds do not flow into productive investments for the future, but seep into economically questionable infrastructure projects and serve, at least indirectly, to finance police-state repression. This is not only problematic with regard to the human rights situation, but also with regard to Egypt’s long-term political stability. If the country collapses, there is the threat of increasing migration pressure and the export of terrorist violence.

The German government should therefore work – if possible together with its European partners – towards an end to the power politics instrumentalisation of Cairo’s debt policy. In doing so, it cannot rely on the IMF – on whose support Egypt will continue to depend in the future – to exert corresponding pressure on the Sisi administration. Instead, it should take a clear position and tie bilateral loans and debt conversions – as well as its support for Egypt in negotiations with international financial institutions, first and foremost the IMF – to two central conditions:

-

First, the Egyptian leadership must credibly begin to dismantle the military’s economic activities. This not only includes the privatisation of army companies in the civilian sector. It also requires disclosing the assets and financial flows of the armed forces. As long as the government cannot credibly show that the country’s funding needs cannot be covered by its own resources, the granting of new external loans does not seem to be very effective.

-

Second, concrete steps must be taken to end police-state repression in the country. This is not only a challenge for the values-based foreign policy propagated by the German government. Rather, without a minimum of separation of powers, an independent civil society, and a free press – in other words, at least a certain degree of checks and balances – it will not be possible to prevent Egypt’s debt policy from being instrumentalised for power politics in the future either.

The challenge: Foreign debt to consolidate power

On 3 July 2013, the military took power in Egypt. The coup was the starting point for the establishment of an authoritarian regime under the leadership of the former defence minister and current president Abdel Fatah al-Sisi. Through the violent suppression of protests,1 the imprisonment of thousands of opposition members,2 the extensive synchronisation of the media,3 and state-controlled, unfree elections,4 Sisi succeeded in consolidating his power in the following years. In terms of state finances, however, the conditions for this consolidation of power were extremely unfavourable. Egypt was on the verge of insolvency in 2013. In the spring of that year, the country’s foreign exchange reserves were not even sufficient to cover imports for three months – a critical value from the IMF’s point of view. In the end, the three Gulf monarchies Saudi Arabia, Kuwait, and the United Arab Emirates (UAE) provided decisive support. They pledged US$12 billion in financial and commodity aid, thus ensuring Egypt’s solvency for the time being5 and in effect sponsoring the military’s takeover of power. However, by 2014 at the latest, Sisi was faced with the question of how to meet the country’s financial needs in the medium and long term.

For the new president, it was not only a matter of covering existing budget deficits, which had been growing due to years of economic crisis. Rather, Sisi also needed financial resources to secure the loyalty of his supporters, first and foremost the armed forces. Since the founding of the Republic of Egypt in 1953, the army has been the centre of power in the country. It not only controlled a “state within the state”,6 it rested also “above the state”.7 Through its sheer size, its tight organisation, and its comparatively good equipment, it held the state monopoly on the use of force, and thus also controlled other institutions such as the Ministry of Interior and the judiciary. In order to consolidate his power, Sisi needed the support of the military leadership, the Supreme Council of the Armed Forces. In return, the generals expected Sisi to further expand the dominant position of the armed forces in politics and the economy and to secure it over the long term.8

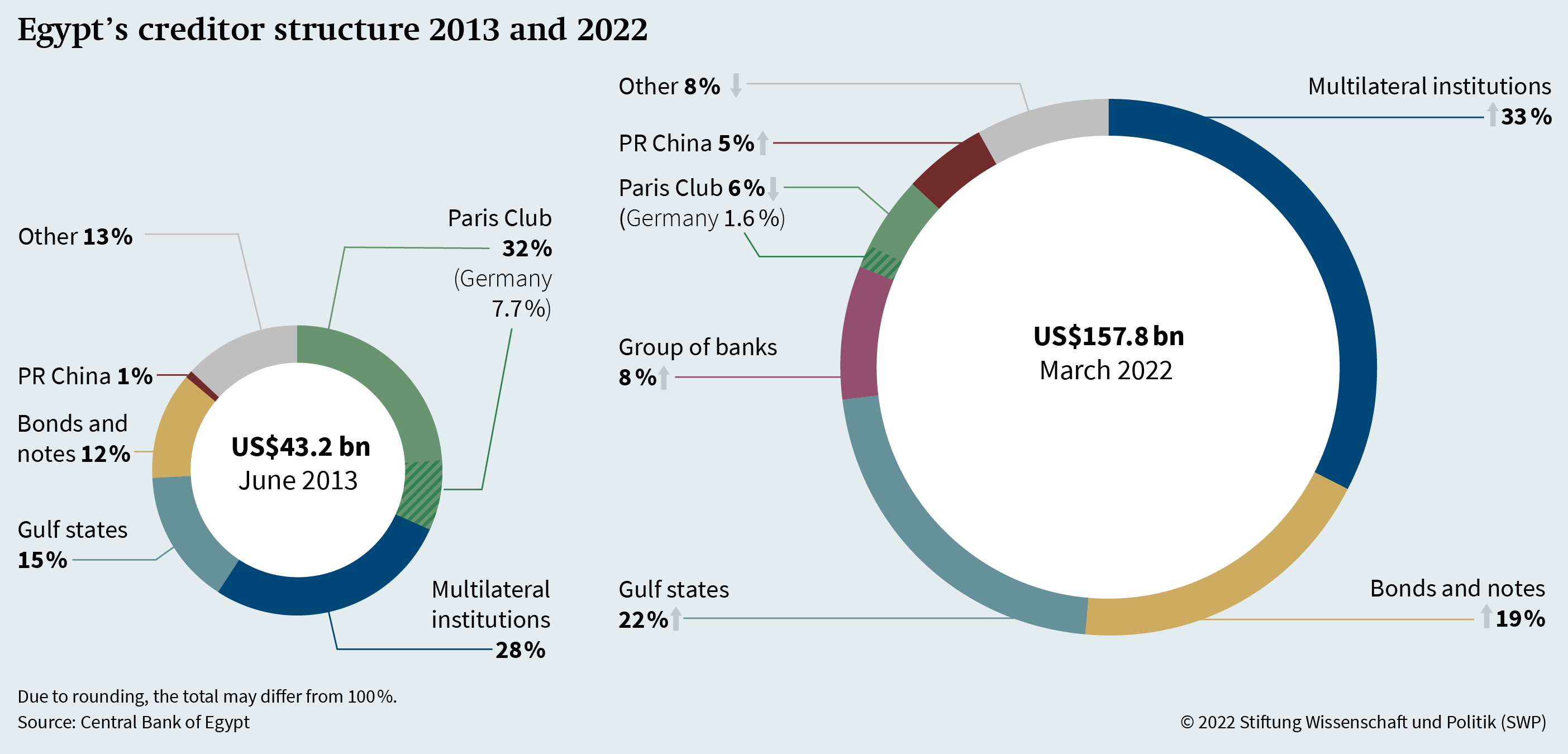

As a response to this challenge, Sisi initiated a paradigm shift by starting to increase Egypt’s foreign debt, which had been kept at a low level since 1991. At that time, the heavily indebted country had benefited from extensive debt relief in return for Cairo’s participation in the US-led military coalition against Iraq in the wake of the Second Gulf War.9 After that, President Husni Mubarak (1981 to 2011) relied primarily on domestic loans to prevent Egypt from becoming dependent on external lenders.10 Under Sisi’s leadership, on the other hand, there has been a significant increase in external borrowing. Between June 2013 and March 2022, Cairo’s external debt increased from around US$43 billion to more than US$157 billion, or, in relation to GDP, from 15 per cent to approximately more than 35 per cent. Excluding foreign exchange reserves, external debt-to-GDP ratio had more than tripled. And its share of total debt has also increased noticeably since then – from just under 18 per cent in 2013 to more than 40 per cent in 2022 (see Figure 1).

In light of more recent political economy research, this development is by no means surprising. Debt allows a non-democratically legitimised government to generate revenue in the short term without having to tax its citizens11 – a favourable situation especially in the process of consolidating power. Although it is usually difficult, due to institutional hurdles, for governments in democratic systems to use credit for their personal political survival, there are no such restrictions in authoritarian systems.12 Accordingly, authoritarian leaders more often resort to the instrument of foreign debt13 to consolidate the loyalty of their coalition of supporters, to buy new allegiance from previous opponents, or to finance police-state repression against opposition groups and dissidents.14

Less attention has been paid in research, however, to the question of how authoritarian regimes conduct debt policy. Especially for the leaderships of poorer countries, two concrete challenges arise here, which become very apparent in the example of Egypt. First, it was by no means easy for Cairo to obtain new external loans. With a national debt (domestic and external) of 84 per cent of its GDP, Egypt was already heavily indebted at the time of the military takeover in July 2013.15 The country was unable to refinance itself easily on the international capital market. Rather, the confidence of portfolio investors was exhausted.

Second, not every loan could be used for power-political purposes. Project-linked loans, for example, were less attractive from this perspective, unless they were used to finance projects that primarily served political purposes. Budget support, on the other hand, had to be free of too strict conditions that would have endangered the consolidation of power. Moreover, it was important to avoid creating strong political dependencies on external actors. Borrowing abroad thus became a balancing act that required tight control by the political decision centre.

The actors: The president and his technocrats

Even before the military coup of 2013, the institutional framework to instrumentalise the state’s debt policy for power politics were largely in place in Egypt. In the 1970s, the regime had developed a complex legislative framework that significantly limited the formal budgetary rights of the legislature, and thus its say in borrowing.16 Under President Sisi, these obstacles to parliament remained and were even strengthened in some cases. Because there was a lack of impact assessment of the long-term financial effects of legislative initiatives, the legislature had little insight into the development of public debt.17 A series of shadow budgets remained essentially outside parliamentary control.18 And the right of parliament to modify the government’s draft budget, introduced under President Mubarak in 2007, was made subject to the proviso in the 2014 constitutional amendment that such interventions should not burden citizens. This condition made it impossible for parliamentarians to introduce an adjustment of taxes or levies as an alternative to borrowing.19

Above all, Sisi ensured that the Egyptian parliament could not become an independent player in the country’s political power structure. The parliamentary elections held in 2015 and 2020 were “neither free nor fair”.20 In the run-up to the elections, domestic intelligence services appeared to be heavily involved in nominating candidates and drawing up electoral lists.21 Despite considerable state mobilisation, the elections were not taken seriously by much of the population.22 As a result, parliament remained “largely a rubber-stamp institution without the competencies and/or willingness to monitor the executive”.23

Parliamentary negotiations on the budget were correspondingly inconsequential. In the past, there had always been loud protests against the government’s draft budgets and its debt policy.24 In the end, however, the budget was always passed, not infrequently in a fast-track procedure, and even critics often voted for it in the end.25 Demands from various parliamentary committees to create a debt ceiling remained inconsequential.26

|

With Tarek Amer and Mahmoud Mohieldin, two old acquaintances gained significant influence over Egypt’s debt policy between 2015 and 2022. Both had worked closely together during the last decade of Husni Mubarak’s presidency and played a major role in steering the country’s economic and financial policy. Amer was deputy governor of the Central Bank of Egypt (CBE) between 2003 and 2008, responsible for the design and implementation of financial-sector reforms; he then took over the leadership of Egypt’s largest state bank, the National Bank of Egypt (NBE). Mohieldin coordinated the government’s economic liberalisation policy as Minister of Investment between 2004 and 2010.a Mohieldin’s good relations with the political power centre at that time were particularly obvious. As a close confidant of the president’s son Gamal Mubarak, he not only became chairman of the influential economic committee of the then all-powerful National Democratic Party (NDP), he was also a member of the ruling party’s politburo.b Amer, on the other hand, was sponsored by CBE chief Farouq al-Okdah, who, because of his military background, was considered a close confidant of Husni Mubarak.c With the political upheaval in 2011, both officials initially lost their political influence. Amer remained at the head of the NBE until 2013, but his access to the centre of power seemed limited until he became head of the CBE in 2015 – a position he kept until August 2022. During this time, he may have had the best contacts with the political leadership, not only because |

of his own position, but also thanks to his wife, Dalia Khorshid. According to press reports, Khorshid had been managing the numerous investments of Egypt’s foreign intelligence service in the country’s media sector since 2017.d Mohieldin, in turn, moved to the World Bank as Managing Director shortly before the start of the uprising in Cairo. In 2013 he became Senior Vice President and was responsible, among other things, for the development programme “2030 Development Agenda”. After other ministers of the last cabinet under Mubarak were accused of corruption, he apparently initially avoided entering Egypt.e Only after Amer’s appointment as head of the CBE was he again regularly present in his home country. Finally, in 2020, he was elected IMF Executive Director at the instigation of the Egyptian government. The fact that President Sisi chose two top officials of the Mubarak era to implement his debt policy can be explained not only by their many years of experience and international networks, but also by another thing the two have in common. Both Amer and Mohieldin are nephews of well-known members of the so-called Free Officers – the small group of military officers that not only deposed the king in 1952, and thus enabled the emergence of today’s Republic of Egypt, but also established the role of the military as a state within the state. In the country’s military establishment, the families of these officers are still held in high esteem today. For Sisi, who is considered extremely distrustful of actors outside the security apparatus, this factor may well be of significance. |

|

|

a On the work of Amer and Mohieldin in the Mubarak era, see Stephan Roll, Geld und Macht, Finanzsektorreformen und politische Bedeutungszunahme der Unternehmer- und Finanzelite in Ägypten (Berlin: Hans Schiler, 2010). b Rutherford, Egypt after Mubarak (see note 9), 220. c See Roll, Geld und Macht (see note a), 236. d Hossam Bahgat, “Looking into the Latest Acquisition of Egyptian Media Companies by General Intelligence”, Mada, 21 December 2017, https://www.madamasr.com/en/2017/ 12/21/feature/politics/looking-into-the-latest-acquisition-of-egyptian-media-companies-by-general-intelligence/. |

e Emad Mekay, “World Bank Unmoved As Allegations Build around Official”, Inter Press Service, 9 August 2011, http://www. ipsnews.net/2011/08/world-bank-unmoved-as-allegations-build-around-official/. Mohieldin was accused of such allegations after 2011, but they did not lead to him being charged in Egypt. See also “World Bank Managing Director Mahmoud Mohieldin Facing Corruption Allegations” (Washington, D.C.: Government Accountability Project, 27 April 2011), https://whistleblower.org/ uncategorized/world-bank-managing-director-mahmoud-mohieldin-facing-corruption-allegations/. |

|

As a result, debt policy was thus completely controlled by the executive, which in the country’s authoritarian system is effectively under the control of the presidential centre of power. It was up to a small circle of technocrats to decide on the raising of new debt and the strategic approach to negotiations with creditors. Between 2015 and 2022, two people who had already shaped the country’s economic and financial policy in important functions under Mubarak (see Box 1, p. 11) had a decisive level of influence.

Banker Tarek Amer replaced the hapless Hisham Ramez as head of the CBE at the end of 2015. The latter had apparently lost favour with the president because he opposed a stronger devaluation of the Egyptian pound and criticised the regime’s costly infrastructure projects.27 In 2016, Amer was instrumental in negotiations with the IMF that led to the finalisation of a three-year loan agreement. He also steered Egypt’s return to the international bond market, which was made possible by the agreement.

The economist Mahmoud Mohieldin – until then Senior Vice President of the World Bank – was appointed Executive Director of the IMF in 2020 on Egypt’s recommendation and at the behest of a number of Arab states. He is thus significantly involved in the negotiations between Cairo and the IMF. However, Mohieldin was apparently already supporting Egypt’s political leadership with his economic expertise and international contacts in the years prior. This is indicated not only by his appearances at official events in the country, but also by the fact that younger economists associated with him reached strategically important government positions. In particular, Rania al-Mashat,28 who as Minister for International Cooperation is involved in negotiations with external donors, and Ahmed Kouchouk,29 who since the beginning of 2016 has been Deputy Minister of Finance for Fiscal Policy and Institutional Reforms and is thus responsible for the debt dossier.

Kouchouk in particular seems to play a central role in the political decision-making process and to enjoy Sisi’s trust. Not only is it formally his responsibility within the government to implement the debt policy operationally,30 he is also, among other things, a member of the board of trustees of the National Training Academy – an institution founded by Sisi that has become increasingly important in the process of consolidating power.31

The instruments: Carrots, sticks, and obfuscation

The institutional framework tailored to the executive and the replacement of key positions in the Ministry of Finance and the CBE in 2015/16 enabled the government under President Sisi to pursue a well-choreographed debt policy. A comprehensive approach was necessary not least because the government in Cairo needed several sources of financing at once. In order to cover the country’s enormous capital needs, loans from international financial institutions and multinational development banks – first and foremost the IMF – were necessary, secondly bilateral financial support from various donor countries, and thirdly money from international investors.

These three sources of funding were directly interrelated. The IMF tied its support to the willingness of other external donors to pay, which was particularly true of Egypt’s traditional sovereign creditors. And to restore and maintain its access to the international capital market, the country needed the IMF’s seal of approval. Without this, international portfolio investors were hardly willing to lend to Egypt on a significant scale. In order to be able to access the three sources and use the corresponding funds as independently as possible, those responsible in Cairo relied on a mixture of incentives, threats, and concealment of the actual debt situation during the following years.

Partial economic reforms

Immediately after the reshuffles within the Ministry of Finance in March 2016, the government and the CBE began to work out a coordinated plan as a basis for negotiations with the IMF.32 After 2011, the military leadership in particular had strictly opposed IMF programmes, apparently because they feared conditions that would impose economic reforms.33 But now Egypt’s foreign exchange reserves were dwindling, which made an agreement with the IMF inevitable. In the months that followed, Cairo finally agreed with the Fund on a series of macroeconomic stabilisation measures as a condition for three years of financing equivalent to 8,597 billion Special Drawing Rights (about US$12 billion).34 Egypt thus fully utilised its borrowing capacity under the Extended Fund Facility.

The concessions that were ultimately made to the IMF included above all the massive devaluation of the Egyptian currency, tax increases, and the reduction of subsidies.35 These were measures that were accompanied by considerable social costs for poorer sections of the population,36 but they contributed to the macroeconomic stabilisation of the country in a very short time. This was particularly evident in the development of foreign exchange reserves, which increased by more than 150 per cent between June 2016 and June 2019, from around US$17.6 billion to more than US$44.5 billion.37 The massive spending cuts also allowed the budget deficit to be slowly reduced, and Egypt achieved a primary surplus (budget surplus excluding debt servicing costs) in fiscal year 2018/19. Economic growth also improved. It reached a preliminary peak of 5.6 per cent in 2019.38

Cairo’s reforms systematically omitted structural problems – the regime nevertheless received excellent marks from the IMF.

The steps taken towards macroeconomic stabilisation, however, concealed the fact that the government systematically omitted important reforms in areas of relevance to power politics.39 For example, tax policy options for revenue generation were by no means exhausted. In particular, the regime made little effort to increase the contributions of wealthier segments of the population towards the financing of state expenditures. It renounced a stronger progressive income tax,40 and the introduction of a capital gains tax, already planned for 2014, was repeatedly postponed.41

Above all, however, the structural weaknesses related to the private sector were not addressed.42 State-owned enterprises continued to benefit from being massively favoured, for example in the awarding of public contracts or in tax law. Many business obstacles, especially for small and medium-sized enterprises, remained in place. And due to the lack of independence of the judiciary, legal certainty continued to be insufficient as well as the government’s willingness to seriously fight endemic corruption.43

Nevertheless, the policy of “stabilisation without reforms”44 paid off twice for Egypt’s leadership. On the one hand, the measures taken were enough for the IMF to give the government excellent marks. The tone of the periodic status reports was consistently positive. Executive Directors repeatedly praised the administration’s “strong ownership”. In a press statement at the conclusion of the programme, the then Executive Director, David Lipton, stressed that the reforms had been successful in “achieving macroeconomic stabilization and a recovery in growth and employment, and putting public debt on a clearly declining trajectory”.45 The final report itself said that “the authorities’ prudent policies” had helped strengthen “Egypt’s resilience to the elevated uncertainty in the external environment”.46 The IMF attributed the fact that the country was in no way able to ensure its solvency after 2019 without external assistance obviously solely to the economic disruptions resulting from the Corona pandemic. Accordingly, it was easy for the Egyptian government to secure new aid from the IMF in 2020. In May of that year, the country was granted loans of US$2.8 billion under the Rapid Financing Instrument and in June US$5.2 billion under a Stand-By Arrangement (SBA).47

On the other hand, Cairo was able to regain the confidence of international investors. For them, the IMF programme had an important signalling effect.48 The close coordination with the IMF created the impression that the Sisi administration was operating fundamentally differently from previous governments. In addition, the rating agencies agreed with the IMF’s positive judgement and upgraded Egypt in their ratings.49 In particular, the massive expansion of foreign exchange reserves was seen as advantageous. The country was consequently able to regain its capital market capability. Between 2016 and 2022, numerous Eurobonds were issued, and the share of government bonds in foreign debt rose accordingly from under 3 per cent to more than 20 per cent.

Investment incentives and government contracts

Approaching the IMF was by no means sufficient to meet Egypt’s financing needs. To finance the three-year IMF programme negotiated in 2016 under the Extended Fund Facilities alone, the country needed US$35 billion, with only US$12 billion being provided by the IMF. The government therefore sought intensive assistance from various donor countries.

President Sisi hoped for further financial aid from the three Gulf monarchies in particular.50 After Saudi Arabia, the UAE and Kuwait had provided significant support for the military coup in summer 2013, they had become the country’s most important creditors. Since then, however, their willingness to provide new loans had noticeably decreased.51 This applied especially for the leadership in Riyadh. After the Saudi change of throne at the beginning of 2015, relations between the two countries had become rather reserved. President Sisi therefore saw himself forced to take a drastic step in April 2016. In order to secure a new support package worth US$22 billion, he agreed to cede two strategically important islands in the Red Sea to Saudi Arabia that had been under Egyptian control since the 1950s.52 Domestic protests against this “island return” were suppressed by massive police-state repression.53

In the following years, the Egyptian government also made it easier for Gulf investors to acquire land and take control of Egyptian companies.54 This became particularly clear at the beginning of 2022, when the Gulf states combined renewed aid with extensive investment commitments. However, these were by no means greenfield investments and also not “privatization in a conventional sense”,55 but rather the acquisition of lucrative state holdings in selected companies, which the Sisi administration apparently had to cede in return for the new loans.56

The UAE, through Abu Dhabi Development Holding, took state holdings in five listed companies, including Egypt’s largest private bank, worth a total of US$2 billion.57 Saudi Arabia agreed with the Cairo government to invest more than US$10 billion through its sovereign wealth fund – the Public Investment Fund – and Qatar – whose relations with Egypt were extremely strained between 2013 and 2021 because of the emirate’s support for the Muslim Brotherhood – also announced US$5 billion in investments.58 These investment announcements were accompanied by fresh loans. In March 2022 all three states together deposited US$13 billion into the CBE,59 increasing the share of Egypt’s total external debt owed to the Gulf monarchies to more than 20 per cent (see Figure 2, p. 15).

Economic incentives also helped to revive relations with the country’s traditional creditors – the Paris Club countries, especially the European ones – whose importance as lenders had declined since 2013 (see Figure 2, p. 15). While the Gulf monarchies received preferential access to the Egyptian corporate sector, Cairo relied on credit-financed government contracts with the European creditor states. In this regard, large European companies received public contracts for infrastructure or defence projects, which were financed by loans from international banking consortia.

Due to their economic importance in their home countries, the companies concerned found it comparatively easy to have these transactions secured by the respective export credit agencies, which in turn made financing through favourable bank loans possible in the first place. This was the case, for example, with the purchase of power plants and railways from the German Siemens Group (see Box 2, p. 11), trains from the British company Bombardier, warships from the Italian manufacturer Fincantieri, and Rafale fighter planes from the French arms manufacturer Dassault Aviation.60

|

In June 2015, Siemens succeeded in concluding the largest business deal in its history. Egypt awarded the German company the contract to build three gas-fired power plants with a total capacity of more than 14 gigawatts to meet the electricity needs of up to 40 million people.a The biggest challenge in the €6 billion deal was its financing. With reference to safeguarding German jobs, the then Siemens CEO, Joe Kaeser, asked for support from the German government as early as February 2015,b which was then granted. A consortium of banks arranged a loan that was secured with export credit guarantees from the federal government (so-called Hermes cover). In 2015 and 2016 alone, Berlin granted Hermes guarantees totalling €4.1 billion.c Accordingly, the Federal Government’s compensation risk in the export business with Egypt rose sharply.d While it was less than €1 billion in 2014, it had risen to €6.7 billion by the end of 2016. By the end of 2021, the value had fallen to €5.2 billion, but Egypt was still among the five countries with the highest compensation risk in an international comparison. In May 2022, Siemens once again announced the largest business deal in the Group’s history. This time, the company, |

as consortium leader, was awarded the contract for the construction of a 2,000-kilometre high-speed rail network in Egypt – contract value €8.1 billion. In addition to the construction of the railway line, the contract includes the delivery of more than 170 trains as well as the construction of depots and stations.e Celebrated by the German government as a “milestone for German-Egyptian economic relations”,f the project has also met with criticism in Egypt in view of empty state coffers.g In any case, the financing of the gigantic infrastructure project became the central challenge. Once again, the majority of the construction costs had to be covered by a long-term bank loan. The prerequisite for this was once again export credit guarantees from the federal government, which Siemens had apparently already been promised in principle in the summer of 2021. In the following years, a new Hermes guarantee of more than €5.6 billion is likely to be issued.h Accordingly, the indemnification risk of the federal government would once again rise sharply, possibly to as much as €10 billion.i Egypt could thus occupy one of the first three places in a country comparison – with the United States and Russia.j |

|

|

a Siemens, “Completion of World’s Largest Combined Cycle Power Plants in Record Time”, press release, 27 July 2018, https://press.siemens.com/global/en/pressrelease/completion-worlds-largest-combined-cycle-power-plants-record-time. b See for the letter from Joe Kaeser to the then Minister of Economics Sigmar Gabriel the Twitter thread by Frederik Richter of 23 November 2017, https://twitter.com/frederik richter/status/933693962384281601. c Author’s calculations, data sources: Export Credit Guarantees of the Federal Republic of Germany. Annual Report 2016 (Euler Hermes Aktiengesellschaft), https://bit.ly/3VOxx0J; Export Credit Guarantees of the Federal Republic of Germany. Annual Report 2015 (Euler Hermes Aktiengesellschaft), https://bit.ly/3VSmio0. d The indemnification risk results “from the future maturities of commitments under cover granted plus interest, less the percentage to be retained by the exporters and banks for their own account”. See Federal Ministry for Economic Affairs and Climate Action (BMWK), Export Credit Guarantees. Annual Report 2021 (Berlin, April 2022), 70, https://bit.ly/3VRPxY3. |

e Siemens, “Siemens Mobility Finalizes Contract for 2,000 km High-speed Rail System in Egypt”, press release, 28 May 2022, https://bit.ly/3PnhJzW. f “Rede von Bundeskanzler Olaf Scholz zum Vertragsabschluss zwischen Ägypten und Siemens Mobility am 26. Mai 2022”, Bulletin der Bundesregierung, no. 68–3 (27 May 2022), https:// bit.ly/3Plv77F. g Marina Zapf, “Siemens fordert in Ägypten Chinas Bahn-Vormachtstellung in Afrika heraus”, Capital, 4 June 2022, https://bit.ly/3HthYqY. h Apparently, the request was issued only to secure Siemens’ shares and not those of the consortium partners. i This sum results from the compensation risk to date and the requested loan guarantees for the railway business amounting to probably €5.6 billion. j In 2021, the United States was in first place with an indemnification risk of €13.2 billion, Russia took second place with €11 billion. See Federal Ministry for Economic Affairs and Climate Action (BMWK), Export Credit Guarantees. Annual Report 2021 (see note d), 70. |

|

Although there were occasional concerns in the relevant ministries,61 the indemnity risk of business dealings with China in the books of the export credit agencies or the relevant government agencies in Germany, France, the United Kingdom, and Italy rose steadily. And the significance of these state-backed credit transactions with international banks for Egypt’s foreign debt has also increased significantly since 2016. In 2018, the CBE even introduced a separate category in the debt statistics through which such loans were recorded.62

For the regime in Cairo, these transactions had an extremely positive side effect. The European governments found themselves in an additional, indirect creditor position, because they had assumed an indemnification risk vis-à-vis the respective national companies or intermediary commercial banks. Accordingly, their interest in keeping Egypt solvent may have increased. In decisions on bilateral budget support and lending by multinational or international financial institutions, in which the Europeans have a considerable say, this circumstance was probably quite relevant.

In addition to European companies, Chinese state-owned firms also increasingly benefited from public contracts and investment opportunities in Egypt. The value of China’s investment and construction was US$12.8 billion in the period from 2014 to 2019, almost 80 per cent higher than in the period from 2008 to 2013.63 In particular in the Suez Economic and Trade Cooperation Zone – a special economic zone on the Suez Canal already established in 2008 – China’s state-owned enterprises were able to expand their investments.64 From Beijing’s point of view, investments in logistics and port infrastructure were of strategic importance for its own trade policy. The Suez Canal is of great importance within the framework of the Maritime Silk Road, which is to connect China’s south-eastern coast with the Mediterranean.65 According to Chinese data, 60 per cent of Chinese exports to Europe are transported through the Suez Canal, and 10 per cent of the annual traffic volume in the waterway is accounted for by ships from the People’s Republic.66

Contrary to official statements by Cairo, which portrayed Chinese involvement as a great success, the Sisi administration may rather have seen it as a means to an end.67 Chinese products not only accounted for the largest share of Egyptian imports, but the country also became the largest source of Egypt’s trade deficit. The fear of flooding the market with cheap Chinese products at the expense of its own industry was therefore widespread in Egypt’s business community.68 And the long-term socio-economic benefits of Chinese involvement remained uncertain in the opinion of some observers.69 In addition, companies from the People’s Republic were extremely self-confident with their demands, which could well lead to conflicts in large infrastructure projects such as the construction of the new capital.70 Closer economic relations, however, were unavoidable for the Egyptian leadership if it wanted to have access to financial aid from Beijing. In fact, China’s importance as a creditor increased dramatically. Whereas the country played only a very minor role as a lender until 2016, it was Egypt’s largest creditor country after the Gulf monarchies in March 2022 (see Figure 2, p. 15).71

Linkage with other policy areas

Of central importance for the success of the debt policy was its linkage with other policy fields. The fact that such measures were embedded in Egypt’s foreign and regional policy was by no means new. President Mubarak had already known to use the country’s regional status to attract financial support from Western partners. President Sisi acted even more aggressively in this regard. In 2016, he gave the argumentative thrust in a speech to the United Nations (UN) General Assembly:

“While the Middle East continues to suffer from bloody conflicts, Egypt has managed to preserve its stability in the midst of a highly unstable region [...]. The international community must acknowledge and support this fact, to the benefit of the region and the world at large, so that Egypt may continue to act as an anchor of stability in the Middle East, sparing no efforts in carrying out its natural role by working with regional and international parties to restore security and stability in the region.”72

Egypt’s official representatives repeated this narrative of the “regional anchor of stability”73 almost like a mantra, and despite massive criticism from civil society actors, it was hardly questioned by Western governments.74 Decision-makers in Europe and the United States ignored obvious indications of destructive regional political behaviour – such as Cairo’s support for general Khalifa Haftar in the Libyan civil war, which undermined UN mediation efforts for the neighbouring country,75 Egypt’s backing for the Assad regime in Syria and Russia’s military intervention there,76 or its obvious siding with the hardly democratic-oriented military leadership in neighbouring Sudan.77 Instead, the narrative served as a basic justification for any cooperation with Egypt,78 even though Western governments simultaneously condemned the extremely problematic human rights situation in the country.79

But the Sisi administration cleverly linked the debt course not only with foreign and regional policy issues, but also with migration and climate policy. This became particularly clear when the refugee crisis in Europe came to a head. In 2015 at the latest, the Egyptian government identified the policy issue as a lever to receive the largest possible amount of financial aid from the Europeans.80 Migration policy thereby became a “dramaturgical act”,81 in which diplomats and politicians deliberately stoked fears of a “flood of refugees” that could emanate from Egypt. Moreover, control of the Egyptian maritime border to the Mediterranean Sea was apparently relaxed to such an extent that between 2014 and 2016 there was significantly more irregular migration to Europe compared to previous years.82

The fact that Egypt received new loans appears to be linked to the closure of its sea border to migrants.

During the negotiations on the IMF loan in 2016, the issue of irregular migration did not officially play a role. Behind closed doors, however, there were apparently tough negotiations on this very issue. This is indicated at least by the fact that immediately after the successful conclusion of the negotiations with the IMF, Egyptian security forces hermetically sealed off the country’s sea border, which caused the number of refugees to drop drastically. And statements by top German and European politicians also suggest that the granting of loans and the closure of the sea border to irregular migration had been directly linked.83

When the refugee crisis in Europe subsided, climate and sustainability issues offered the Egyptian government a new opportunity to link its debt policy to an issue that is highly relevant for international financial institutions and Western donor countries. In 2016, the Sisi administration presented its national strategy for sustainable development, the “Egypt Vision 2030”, which is closely aligned with the United Nations’ 2030 Agenda for Sustainable Development and the African Union’s Agenda 2063. Civil society actors criticised the lack of a detailed roadmap for achieving the goals set out in the strategy and the fact that independent non-governmental organisations (NGOs) could hardly participate due to police-state repression.84 Government representatives, on the other hand, did not tire of emphasising Egypt’s regional pioneering role, especially in climate policy. Above all, the topic of climate financing was promoted. After President Sisi mandated the government to significantly expand green and sustainable financing,85 Egypt became the first North African country to issue “green bonds” to the tune of US$750 million in 2020 (see Box 3).

|

In September 2020, Egypt became the first North African country to issue so-called “Green Bonds”. The five-year bond was seven times oversubscribed and, due to high demand, US$750 million was issued instead of the initially planned US$500 million. The declared goal of the issuance was to “integrate sustainability considerations into its public budget financing plans”.a As announced in the “Vision 2030” development plan published by the government in 2016, the share of sustainable projects in public investments is to be significantly increased, not least in order to achieve the country’s self-set climate goals. The World Bank celebrated the issuance, which it had supported through its Government Debt and Risk Management Program, as a great success, stressing that Egypt’s example will inspire other emerging economies to consider “green bonds” as a financial solution.b Behind the latter is the financing of a monorail to connect Egypt’s new capital under construction with the metropolis of Cairo. |

Even if the railway project should meet certain sustainability standards on its own,c it is part of an infrastructure project that is extremely dubious, especially from the perspective of sustainable development. Initial independent studies criticise that the construction of the new capital could aggravate Egypt’s water issues and destroy large parts of the fragile desert landscape east of Cairo.d Critics also accuse the Sisi administration of repeating the mistakes of past governments and ignoring the needs of the population. Instead of investing in this prestigious project, it would make more sense to invest in existing cities and improve the living conditions of the poor. From that perspective, the new capital is at best geared to the needs of the Egyptian upper class and will further isolate the political leadership from the people.e |

|

|

a Ministry of Finance, Egypt Sovereign Green Bond Allocation & Impact Report 2021 (Cairo, 2021) 11, https://assets.mof.gov. eg/files/a3362b50-574c-11ec-9145-6f33c8bd6a26.pdf. b World Bank, “Supporting Egypt’s Inaugural Green Bond Issuance”, 15 March 2022, https://www.worldbank.org/en/ news/feature/2022/03/02/supporting-egypt-s-inaugural-green-bond-issuance. c There are also doubts about this. For example, civil society actors complain that the project will destroy residential neighbourhoods and functioning neighbourhood spaces and uproot street trees that are important for the city’s climate; see Menna A. Farouk, “Egypt’s Street Trees Fall Foul of Urban Development Drive”, Thomson Reuters Foundation News, 20 May 2022, https:// news.trust.org/item/20220520085932-xmd3g; Beesan Kassab, “Move to Demolish Nasr City Neighborhoods Based on Profit, |

Not Public Interest, Experts Say”, Mada, 26 January 2022, https://bit.ly/3Hxc3Bb. d Julian Bolleter and Robert Cameron, “A Critical Landscape and Urban Design Analysis of Egypt’s New Administrative Capital City”, Journal of Landscape Architecture 16, no. 1 (2021): e Rod Sweet, “Dreamland: A Critical Assessment of Egypt’s Plan for a Brand New Capital”, Construction Research and Innovation 10, no. 1 (2019): 18–26, https://www.tandfonline.com/doi/ full/10.1080/20450249.2019.1583946; “Egypt’s Sisi Looks to New Desert Capital to Cement Legacy”, rfi, 14 November 2021, https://www.rfi.fr/en/middle-east/20211114-egypt-s-sisi-looks-to-new-desert-capital-to-cement-legacy. |

|

Climate finance also became the central theme at the 27th UN Climate Change Conference (COP27), which took place in Egypt’s Sharm el-Sheikh in November 2022. While the logistical preparation for the conference was apparently largely controlled by Egypt’s General Intelligence Service GIS,86 one of the architects of Cairo’s debt policy is largely responsible for its content. Mahmoud Mohieldin was appointed Climate Action Champion of the country by the government in February 2022 – a position he has since held in personal union with his mandate as IMF Executive Director.87 Mohieldin himself, as well as members of the Egyptian government, repeatedly stressed the need to put financing issues at the heart of the conference.88 In June 2022, right in time for the COP27, the government presented a national climate strategy for the period up to 2050. The strategy estimates Egypt’s financing gap for implementing the required mitigation and adaptation programmes at a total of US$248 billion.89

Concealment of the actual debt situation

In order to be able to enter into new loan obligations, the Egyptian government had to provide its creditors with information about the country’s debt situation. Accordingly, it was necessary for the CBE to publish debt statistics on a regular basis. These served as an important benchmark for debt sustainability, both in the IMF status reports, which have been published regularly since 2016 as part of the respective programmes, and in the obligatory prospectuses for the issuance of government bonds and notes. In addition, the statistics were also used in the government decision-making of individual creditor countries, not least to adequately assess the risk involved in issuing export credit guarantees. However, it was questionable for several reasons as to whether the Egyptian government’s statistics actually adequately reflected the country’s debt situation or whether they may have underreported the amount of foreign debt.

The government was able to massively expand its borrowing without it becoming visible in the official statistics.

Fundamentally, it is unclear how credible government statistics are in Egypt. According to the World Bank, the country has a high capacity for data collection, but data transparency is limited.90 Data provided by the government about economic and social development therefore always raises questions.91 As far as the CBE’s debt data is concerned, civil society actors such as the Egyptian Initiative for Personal Rights criticise that these were published only with several months delay.92 In addition, the NGO complained that the statistics on foreign debt did not include loans in local currency owned by foreigners.93 In fact, such foreign investments in high yield domestic Egyptian treasuries (carry trades) had successively increased after 201794 before they reached their temporary peak in September 2021 with a volume of US$34 billion.95 Particularly helpful in this context was the CBE’s monetary policy, steered by Tarek Amer, which set disincentives for foreign capital investors. After the sharp devaluation of the Egyptian pound in 2016, the CBE had kept the exchange rate largely stable within a narrow range – contrary to the IMF’s demand for its complete unpegging – and minimised the currency risk for carry trades.96 The government was thus able to massively expand its borrowing without reporting this in the official foreign debt statistics. How dangerous such a form of borrowing is for the short-term availability of foreign currency, and thus the solvency of the country, became apparent after the Russian invasion of Ukraine: Within a few days, Egypt saw an exodus of up to US$3 billion by concerned foreign investors, which put the country’s currency reserves under massive pressure.97

While the handling of carry trades within the official statistics could still be considered as balance sheet cosmetics (since they did not appear as external debt, but their issuance was documented as part of domestic debt), the statistical recording of other loans is fundamentally in question. This concerns, for example, a loan agreement for US$25 billion that had apparently already been entered into with Russia in 2016 as part of the planned construction of Egypt’s first nuclear power plant. Although construction of the power plant is now apparently in full swing, despite Western sanctions against Russia,98 details of this agreement are hardly known.99 Until 2022, only a small part, if any, of the liability was listed in the CBE’s statistics.100 In the coming years, the country’s foreign debt could increase significantly as a result of this agreement alone. Similarly problematic was the non-transparent handling of contingent liabilities incurred by the state through the borrowing of public companies or state authorities (“economic authorities”).101 Since 2015, the Egyptian state appears to have provided guarantees for the borrowing of public institutions and enterprises to a greater extent than before.102 For March 2021, the government estimated that total government-guaranteed debt amounted to 19.9 per cent of GDP.103 According to older government statistics, more than half of this amount is accounted for by public external guarantees, which secure loans signed between public or private enterprises and foreign creditors.104 As no verifiable breakdowns have been provided, such figures can at best be considered a vague estimate. It also remains unclear which of these liabilities were included in the CBE’s external debt statistics. It is worth noting that the IMF warned in 2021 that in a “shock scenario”, contingent liabilities could become actual liabilities, which would cause Egypt’s public debt to soar.105

The profiteer: The military and its economic empire

The successful external debt policy opened up some fiscal space for the government under President Sisi. Of the US$115 billion in new external debt that Egypt took on between June 2013 and March 2022, the smaller part went into padding the CBE’s reserves. The larger part, more than US$96 billion,106 was used by the political leadership to finance government spending that was not matched by corresponding revenues. The government justified the expansive debt policy primarily by saying that it would contribute towards improving the economic framework conditions, creating incentives for private – and especially foreign – direct investment, which would in turn positively impact long-term growth.107

However, this effect has not materialised so far. Private-sector investment fell to an average of 6.3 per cent of GDP between 2016/17 and 2020/21 (it had been on average more than 10 per cent between 2006 and 2010).108 This was below the level of Gamal Abdel Nasser’s presidency (1954–1970), which had pursued a socialist-style economic policy.109

Even before the onset of the two external shocks – the Corona pandemic in 2020 and the Russia-Ukraine war in 2022 – the business climate in the Egyptian private sector was extremely poor. For example, even before 2020, the majority of S&P Global’s monthly Purchasing Managers’ Index (PMI) pointed to a contraction in private economic activity outside the oil and gas sector.110 Also the annual inflow of foreign direct investment, which was concentrated mainly in the low labour-intensive oil and gas sector, remained at a minimal level compared to the late 2000s.111 The country’s economic growth, which at times was above the regional average, was mainly explained by government construction projects and was thus only temporary. In general, there was a lack of growth drivers,112 resulting in unfavourable prospects for further economic development.113

At the same time, however, the repayment and interest costs that the Egyptian state had to bear for external and domestic debt continued to rise (see Figure 3, p. 25). In fiscal year 2020/21, more than 50 per cent of government revenues had to be spent on interest payments – in 2012/13 it was still less than 42 per cent.114 Due to the high interest and repayment burden, an increasingly smaller share of budget expenditure was available for public investment.115 Interest payments on external loans have so far only accounted for a small part of this, which can be explained by the sometimes generous repayment periods. However, a clear increase can be seen here as well. In 2013/14, external loans accounted for less than 3 per cent of interest payments; in 2021/22, it is expected to be more than 10 per cent.

In light of this, the question of what the government actually did with the financial leeway created by borrowing is all the more important. There are several indications that the military in particular – and thus the actor on which President Sisi was directly dependent to consolidate his power – benefited from the debt policy. Under President Sisi, the armed forces were able to significantly expand their position in the Egyptian economy. Sisi himself assigned the military the role of the “motor of national development”.116 The Ministry of Interior, and particularly the GIS, were also able to advance their own economic agendas, but compared to the military to a much lesser extent.117 In this context, external borrowing may have been important in three ways. It protected the revenues and assets of the armed forces, contributed to the financing of major projects in which they could earn significant money, and enabled an expansive military build-up that benefited the officer corps in particular.

Protection of revenues and assets of the armed forces

The Ministry of Defence and its subordinated Ministry of Military Production control four state agencies or organisations through which the military had been operating in the civilian economy for decades – the National Service Projects Organization (NSPO), the Arab Organization for Industrialization, the National Authority for Military Production, and the Armed Forces Engineering Authority.118 Since 2013, these actors have been increasingly active, for example in food production, the energy industry, and in construction and infrastructure projects.119 Due to a lack of data, the speed and scope of this expansion can only be guessed at on the basis of intermittent reports. The Ministry of Military Production, for instance, predicted that revenues from the operations of its 20 companies would be 15 billion Egyptian pounds (LE) in the 2018/19 fiscal year – around five times higher than in the 2013/14 fiscal year.120

The borrowing helped to ensure that these revenues remained in the military’s own operating system. Consequently, the government was able to prevent the repeat of an extremely unpleasant situation for the armed forces that occurred in 2011. At that time, the military leadership had to shore up the CBE’s foreign exchange reserves with a US$1 billion cash injection to avert national bankruptcy.121 Between 2013 and 2021, the military apparently did not have to contribute towards financing budget deficits. On the contrary, its business empire benefited from extensive tax exemptions. The NSPO, for example, under whose umbrella no fewer than 35 companies with a combined annual turnover of well over US$1 billion were managed in 2019,122 was exempt from income tax under Egyptian tax law, as were other military companies.123 The armed forces were generally exempt from property taxes, and while the government decided to increase VAT as part of the reform programme agreed with the IMF to increase government revenues, it simultaneously introduced generous exemptions for military companies. Accordingly, goods and services that served national defence were exempted from VAT, with the Ministry of Defence being given the right to define them.124

Where the revenues of the military economic empire flowed to cannot be answered satisfactorily due to a lack of transparency.125 In this context, there is repeated speculation about the existence of “special funds” to which the armed forces have access.126 While civilian government agencies are only allowed to maintain accounts at the CBE, the armed forces can invest money and foreign currency in private banks outside Egypt through their companies.127 At least some of these funds may be managed through intermediaries. For example, numerous offshore companies in tax havens such as the British Virgin Islands and the Bahamas have ownership links to Egyptian entrepreneurs, some of whom apparently have excellent contacts to the military or the secret service.128

The successful borrowing also meant that there was no particular financial pressure to privatise military assets. Although President Sisi first publicly mentioned the possibility of privatising military companies in 2019,129 no concrete steps were taken until 2022. In fact, the IMF and the World Bank have not called for such privatisation for years. It was not until 2021 that the IMF started to criticise the competition-distorting role of military companies publicly and called for reforms.130 Since then, there has been some movement, at least on a declaratory level. In early 2022, the head of Egypt’s capital market regulator raised the prospect of initial public offerings in the near future.131 President Sisi also publicly repeated similar announcements.132 In the absence of concrete steps, however, it remained unclear whether this was merely rhetoric in the context of negotiations for new IMF loans. Moreover, the government remained silent on the question of whether possible proceeds from the sales would in the end actually be used to finance the budget deficit, and thus be taken away from the armed forces.

Loan-financed infrastructure projects

External borrowing enabled the Sisi administration to realise a series of infrastructure projects from which the military benefitted in particular. Although the expansion of transport routes and energy supply could certainly have positive effects on the economic development of the country,133 in the cases of individual mega-projects and the enormous expenses associated with them, the benefit for society as a whole is more than questionable.

An example of this was the hasty expansion of the Suez Canal in 2015. A new lane was dug in record time – an undertaking that served as a stage for President Sisi to present himself as a national leader,134 but which is unlikely to be profitable for the state budget in the foreseeable future. The speed with which the expansion was completed – due to political demands – led to massive cost increases of ultimately more than US$8 billion, which in turn contributed to further borrowing, including from external sources.135

Even at the beginning of the construction, the forecast that the income from the canal business would increase by up to 150 per cent within eight years was not very reliable.136 And the Suez Canal Authority, which was supposed to finance the project by issuing bonds, even had to ask the Ministry of Finance to pay off US$600 million in overdue loan repayments in 2019.137 These were bank loans obviously used to pay foreign companies involved in the expansion. Meanwhile, the military’s construction arm and a few selected private companies benefitted from the non-transparent awarding of contracts. The military was evidently able to make profits simply by subcontracting.138

The construction of a new capital – the New Administrative Capital – to the east of the metropolis of Cairo was just as economically questionable as the canal expansion. Here, too, no transparent feasibility studies were presented in advance. President Sisi himself put the cost in 2020 at LE 380 billion (about US$24 billion at that time), spread over seven years.139 Other estimates were as high as US$58 billion.140 The government’s assurances that the public budget would not be affected because the project would be largely financed by private investment were patently false.141 Especially in the initial phase, private companies withdrew from the project because they were afraid that later returns would not cover the initial investments. In the end, the state had to step in with financial injections, also at the expense of rising foreign debt.

Whether these investments will pay off for the regular state budget is doubtful, to say the least. However, the Egyptian military is likely to profit economically in this case as well. It became publicly known that the armed forces have a majority stake in the Administrative Capital Urban Development Company (ACUD)142 – the state-owned operating company to which the government transferred the lucrative building land for the new city. Whether the military also contributed own financial resources to the implementation of the mega-project, however, remains unclear. The budget of the ACUD is kept secret due to the involvement of the armed forces.143 However, President Sisi announced in July 2022 that the company would charge the state LE 4 billion (about US$212 million in that time) annually for office rents.144

Loan-financed arms expenditure

At the same time that Egypt’s foreign debt rose sharply, Cairo made significant purchases of armaments. According to data from the Stockholm International Peace Research Institute (SIPRI), the country even became the world’s third-largest arms importer between 2017 and 2021. The country’s share of global arms imports thus increased by 73 per cent compared to the period 2012–2016, when Egypt ranked 11th.145 In 2019 and 2020 alone, the government made purchases worth an estimated US$16 billion.146 These purchases covered almost all types of weapons. Even assuming that purchases of this magnitude are based on generous payment terms, Egypt is spending significant amounts of money on arms acquisitions. It seems that the military has been able to buy new weapons systems on the international market largely without financial restrictions.

The military utility of the arms purchases is questionable – but they open up avenues for personal enrichment.

It is remarkable that the excessive arms purchases could hardly be reconciled with Egypt’s official defence budget. Adjusted for inflation, it had even shrunk between 2011 and 2020.147 And even in a regional comparison, the reported defence spending seemed rather below average.148 Arms purchases were thus apparently not financed through official military spending, but through other means. Direct financing by the Gulf monarchies could have played a role, especially in the case of arms deals with Russia.149 However, at least some of the purchases may also have been financed through external borrowing. An example of this was the aforementioned purchase of French fighter jets in 2015 and 2021, for which Cairo entered into loan agreements with French banks amounting to at least €7.2 billion.150

How many purchases were actually financed by loans cannot be conclusively answered due to a lack of data transparency, nor can the question of where such loans are found in the CBE’s statistics. Egyptian analysts suspect that in the CBE’s monthly reports, at least some of the borrowing by the military fell under the debtor category “other sectors”. Debt under this heading had increased by about US$11.3 billion between June 2013 and March 2022, far more than tripling (from US$4.08 billion to US$15.34 billion).151

It is also possible that the military was able to finance part of the arms procurement with its own funds. However, the question then arises as to whether this money could not have been used in a better way for the benefit of society as a whole, for example to improve the extremely precarious socio-economic situation of the population. Even from a military point of view, the excessive arms procurement did not seem very plausible. On the one hand, military analysts questioned whether the purchase of large weapons systems could really be justified by the country’s need for security. Asymmetric threats, such as those posed by armed militant groups, can hardly be countered in this way.152 And the massive investments into the military infrastructure in the east of the country need to be explained against the background that there is a peace treaty with Israel.153 On the other hand, there are likely to be significant consequential expenses due to the fact that Egypt has diversified its arms procurement. Individual systems are not compatible with each other, which increases maintenance and personnel training costs accordingly.154

Although the military utility from the arms acquisitions is by no means clear, the economic benefit they bring to members of the officer corps could be significant. Due to the secrecy and the lack of legal regulations, the Ministry of Defence was able to make arms purchases through direct contracting, without a transparent bidding process.155 In addition, Law No. 147 ensured that arms purchases were exempt from taxes and not subject to control by Egypt’s Central Auditing Organization. This framework prepared the ground for widespread corruption. Not only decision-makers in the Ministry of Defence were able to enrich themselves personally, but also former officers who brokered arms deals as local agents.156 For the officer corps’ support for the president, these side incomes were not insignificant.

Conclusions and recommendations

Egypt’s excessive borrowing in recent years has been interpreted as a weakness of the country in numerous analyses. Even the term “beggar state” was used.157 Yet, Egypt’s debt policy has so far proven very successful for President Sisi. The government in Cairo has been able to master the two challenges outlined at the beginning. First, loans from international financial institutions, donor countries, and foreign portfolio investors enabled the country to refinance itself. Second, the political leadership did not make any substantial concessions that would have contradicted the goal of consolidating its own rule. The prerequisite for this success was that the Sisi administration used a well-coordinated mix of instruments and that practical action was in the hands of experienced, internationally well-connected technocrats who were closely linked to the presidential power centre.

The military in particular benefited from this debt policy and was able to significantly expand its position in the Egyptian economy during the period under review. This was a decisive factor in President Sisi's consolidation of power. For him, the loyalty of the armed forces has been the most important prerequisite for enforcing wide-ranging police-state repression. The president was thus able to effectively stifle any political opposition.

Nevertheless, the question arises as to how long this instrumentalisation of debt policy for power-political purposes can be continued. For Egypt, it is becoming increasingly difficult to finance itself through external borrowing due to the increased debt burden. The war in Ukraine is acting here as an accelerant. Economic uncertainty and rising interest rates in major industrialised countries are affecting the willingness of international portfolio investors to invest their money in an emerging market such as Egypt. At the same time, the government will need fresh external financing in the future to close the budget deficit, which will remain high, not least due to the rising interest burden. Projections indicate an average annual external financing requirement of US$26 billion for the next three budget years alone.158 This leaves borrowing through financial institutions and donor countries as the only option. In fact, in March 2022, Egypt was forced to ask the IMF for help again. Although government circles initially voiced optimism and held out the prospect of a quick agreement with the IMF, the negotiations turned out to be much more difficult than in 2016.159 As a result, the state’s financial situation came to a dramatic head. In the following months, the cost of hedging Egyptian government bonds rose to record levels and almost tripled between January and October 2022.160 At the same time, the CBE’s currency reserves dwindled faster and faster, the Egyptian currency depreciated, and inflation rose.161 The CBE’s strategy of keeping the exchange rate as stable as possible, and thus creating attractive conditions for foreign capital investors, had failed.

A growing unease had also become noticeable within the political leadership under President Sisi. In August 2022, the head of the CBE, Tarek Amer, was replaced. Sisi had evidently lost confidence in one of the main people responsible for Egypt’s debt policy.162 The banker Hassan Abdalla was put in charge as acting governor of the CBE. His task was apparently to initiate a change of course in the exchange rate policy, and thus create the conditions for new financial support from the IMF. The latter had apparently made the floating of the exchange rate an ultimate condition for new support. In fact, on 27 October 2022 – in the wake of a massive devaluation of the Egyptian pound by around 15 per cent against the US dollar – the IMF announced the long-awaited conclusion of a staff-level agreement on a new Extended Fund Facility Arrangement. According to this agreement, the IMF will support an Egyptian reform programme with a new credit line of US$3 billion over 46 months,163 which should unlock billions of US dollars in additional financing from other donor countries and international financial institutions.

Despite the change in exchange-rate policy, the appointment of Hassan Abdalla as head of the CBE in fact indicates that the political leadership will fundamentally try to continue to instrumentalise debt policy for power-political purposes. Like Mahmoud Mohieldin and Tarek Amer, the banker belonged to the close circle of economic technocrats loyal to the regime in the last years of the Mubarak era and was considered a confidant of the president’s son Gamal Mubarak in that time.164 Before his appointment as head of the CBE, Abdalla headed the United Media Service holding company, a media conglomerate apparently controlled by the GIS.165 It can be assumed that, like his predecessor, he will coordinate closely with the presidential power centre and give top priority to the interests of the military.

The decisive factor for the further course of Egypt’s debt policy will therefore be how the country’s creditors position themselves. Three considerations should guide German and European policy in this regard.

1. A “business as usual” lending policy would be the worst of all options. As long as the Egyptian leadership uses loans to consolidate its rule, it can only succeed in the short term in averting the country’s insolvency through new debt. The misallocation of financial resources for the benefit of the armed forces opposes the development of a competition-based, free-market economy, reinforces the social imbalance in the country, and enables police-state repression. New loans without conditions or with conditions along the lines of the 2016 IMF programme would thus further increase the debt burden and, accordingly, the interest burden, without providing the decisive impetus for Egypt’s economic, social, and political development. Germany and its European partners should therefore have no interest in maintaining the same lending policy as in the past for two reasons.

On the one hand, the financial risk would further increase because Cairo might soon no longer be in a position to meet its payment promises on time. For Germany, for example, Egypt has become the largest debtor among developing countries in terms of receivables from development aid loans, with almost €1.8 billion (as of the end of 2020).166 In addition, there is extensive budget support amounting to €450 million and the drastically increased indemnification risk through export credit guarantees. Egypt’s insolvency would thus also have direct financial consequences for Germany – in addition to indirect consequences. Germany is an important donor country to a number of development banks – first and foremost the IMF – and would therefore also have to shoulder their loan defaults.

On the other hand, it would exacerbate rather than mitigate Egypt’s destabilisation if the current practice of lending were to continue. The combination of social decline and police-state repression increases the risk of future unrest. The popular uprising of 2011 should be viewed as a warning here and not as a singular historic episode. Europe is threatened with unforeseeable negative consequences if the most populous neighbouring country, with more than 100 million people, is destabilised. In this case, increasing migration pressure and an export of terrorist violence can be expected.

2. It is questionable whether the IMF will push for a change of policy in Cairo. The IMF has not been sufficiently critical of the debt policy of the Sisi administration. On the contrary – both through the conditions for lending and through appreciation of Cairo’s insufficient reform policy – it has further favoured its instrumentalisation for power politics. In particular, it was a big mistake in this context to ignore the economic expansion of the Egyptian armed forces. Despite the fact that there are enough analyses pointing out the military’s problematic economic activities and presenting various options for its gradual withdrawal from the economy,167 the IMF did not address this issue publicly before 2021. And even then, the Fund addressed the issue in rather general terms, pointing out that the “large state footprint should be gradually reduced”.168 Such formulations fail to deal with the dimension of the problem in an adequate way. Instead, a traceable and verifiable roadmap for the privatisation of army companies as well as more transparency with regard to the income and assets of the armed forces should be conditional to any new loans. In principle, Egypt should only receive new financial assistance if the political leadership can credibly demonstrate that its needs cannot be met with its own resources.