Divergence and Diversity in the Euro Area

The Case of Germany, France and Italy

SWP Research Paper 2019/RP 06, 10.05.2019, 39 Pagesdoi:10.18449/2019RP06

Research AreasDr Paweł Tokarski is Senior Associate in the EU / Europe Division at SWP.

When the European Union introduced a common currency, this was based on the assumption that there would be increasing economic convergence of the participating states. These expectations were not met. Instead of gradually converging, the economic performance of euro area countries has noticeably diverged. The most considerable problem arising from this divergence is that it leads to social differences and to discrepancies in political interests regarding further direction of economic integration. Thus, in the long term, the current integration model within the euro area might be called into question.

Previous analyses of economic differences in the euro area have mostly focused on specific groups of countries, such as southern Europe versus northern Europe or central versus peripheral Europe. This study takes a different approach to the issue of convergence by looking at the three largest economies in the euro area: Germany, France and Italy.

Table of contents

Divergence and Diversity in the Euro Area

2 The Sheer Diversity of Economic Models Causing the Lack of Convergence

2.1 Convergence and Diversity in the Monetary Union

2.2 Fundamental Differences in Economic Models

2.4 The Role of the State and Social Dialogue

2.5 The Efficiency of Public Institutions

2.6 Economic Structures: Differences and Connections

3 Convergence or Divergence in the Monetary Union?

3.4 The Labour Market Situation

4 The Future of the Euro Area with Limited Convergence

4.1 Convergence through Disintegration or Fragmentation of the Monetary Union?

4.1.1 Withdrawal from Monetary Union

4.1.2 Splitting the Euro Area into Two Currency Areas

4.2 Stabilising Monetary Union with Limited Convergence

4.2.1 Transforming Economic Models

4.2.2 How Much Centralisation of Power Should There Be in Monetary Union?

4.2.3 Further Risk-Sharing with Stronger Conditionality

Issues and Recommendations

Divergence and Diversity in the Euro Area. The Case of Germany, France and Italy

When the European Union introduced a common currency, this was based on the assumption that there would be increasing economic convergence of the participating states. These expectations were not met. Instead of gradually converging, the economic performance of euro area countries has noticeably diverged. The most considerable problem arising from this divergence is that it leads to social differences and to discrepancies in political interests regarding economic and monetary integration. Thus, in the long term, the existing integration model within the euro area might be called into question.

Previous analyses of economic differences in the euro area have mostly focused on specific groups of countries, such as southern Europe versus northern Europe or central versus peripheral Europe. This study takes a different approach to the issue of convergence by looking at the three largest economies in the euro area: Germany, France and Italy. There are good reasons for focusing on these countries when analysing euro area stability. Together they account for almost 65 percent of the euro area’s Gross Domestic Product (GDP) and are home to around 210 million of the EU-19’s 341 million citizens. All three are among the most important economies in the world. They are also the only euro area countries that belong to the G7 and G20 formats. Furthermore, the stability of Germany, France and Italy is essential for the euro area. A massive financial assistance package for any one of these countries, even if unimaginable for Germany or France, would exceed the capacities of the European Stability Mechanism (ESM). Finally, the main challenge for the euro area is the sustainability of the economic models of the three largest economies. Italy’s economic and social problems (risks in the banking sector, excessive public debt, unemployment, regional differences) constitute a systemic risk for the currency area. Similarly, France has to implement comprehensive structural reforms. Meanwhile, the stability of the euro area depends heavily on the sustainability of the German economic model. Today, the Federal Republic of Germany functions as a stabiliser for the euro area, whereas in the late 1990s it was still referred to as the “sick man of Europe” and was regarded as a risk for monetary integration.

This study’s central focus is the unequal development of the three states. The intention is not to clarify whether or not sustained convergence within the monetary union could be promoted, and how, but rather how to deal with limited convergence. The research aims to answer key questions about the future of the euro area. How did the significant differences in economic performance between the three countries come about? Where do divergence processes show themselves most clearly? Could a return to national currencies support the necessary structural reforms and convergence? And what conclusions can be drawn from the economic performance of the three countries regarding current debates on euro area reform? This study will outline existing concepts of convergence before considering the economic systems of the three states in all their diversity. Thereafter, it will examine various options for consolidating euro area stability.

The reasons behind the divergence cannot be adequately assessed without analysing the structural problems of the euro area members, whose economic models are very heterogeneous. Differences include, for example, the role of the state, the quality of institutions and economic structures. They are responsible for the fact that membership of a common currency area has not brought about the hoped-for convergence. Instead, the financial and euro crises have further exacerbated the differences. This is evident in both nominal and real convergence indicators, which measure the economic and social divergence of the three largest euro area countries. The most significant differences are in competitiveness, current account balances, public debt and the labour market. A comparison of the real per-capita GDP growth rates of the twelve founding members of the euro area since 1999 shows that Italy’s deviation is greater than average. The economic models of Germany, France and Italy differ to such an extent that it is impossible to pursue a sustainable convergence path. Reforms in the euro area must therefore focus on how to stabilise the single currency under the conditions of limited convergence between its largest economies.

Everything suggests that there is no simple solution to further stabilising the euro area. Neither returning to national currencies nor federalising the euro area are a way out. Convergence and structural change will heavily depend on independent factors such as a positive economic environment, as well as a favourable political situation in the largest euro area members. In particular, stabilising the euro area requires continuing the structural changes at member state level. The efficiency of state institutions must be improved; as recent research shows, this has a major influence on real convergence. The largest euro states should be monitored more intensively and from the long-term perspective within the framework of the European Semester – their importance for the stability of monetary union and the difficulties associated with structural changes implies this. It is also essential to keep monetary policy clearly involved in the stabilisation process and to increasingly share risks, including the joint debt issuance. The ESM should be strengthened, especially in its role as backstop of the banking union. This also means increasing the ESM’s lending capacity. Ultimately, the euro cannot exist without the support of public opinion; social integration therefore needs to be further strengthened in the euro area.

The Sheer Diversity of Economic Models Causing the Lack of Convergence

Convergence and Diversity in the Monetary Union

Convergence in the EU context means the alignment of individual member states’ economic performances. Sustainable convergence means that economically weaker countries move towards the level of stronger economies.1 The term divergence describes the opposite: a drifting apart of states’ economic performances. There are different types of convergence that can be measured by specific indicators. Nominal convergence describes harmonisation by nominal variables such as inflation, interest rates, budget deficit or public debt. This has been a condition for entry into the euro area since the beginning of monetary union. Real convergence, on the other hand, is measured in terms of how much a country’s general standard of living, working conditions, economic institutions and structures change for the better in comparison with better positioned countries.2 This study analyses the main aspects of real and nominal convergence using concrete examples relating to competitiveness, public finances, income levels and the labour market. There is a special focus on the role, efficiency and particularities of national institutions.

The wish to promote convergence has always played a central role in the historical development of monetary integration. As long ago as 1974, the Council of the European Communities made it clear that the project of economic and monetary union could not be tackled as long as convergence in member states’ economic policies could not be achieved and maintained.3 The 1989 Delors Report, named after the then-President of the European Commission, argued that a monetary union without sufficient convergence of national economic policies would not survive in the long term and could harm the Community.4

The current EU Treaties contain references to real and nominal convergence. Article 3 TEU sets out the objective of promoting the well-being of member states and the “economic, social and territorial cohesion” between them. Article 121 para 3 TFEU provides that the Council shall monitor economic developments in each member state and in the Union in order to “ensure closer coordination of economic policies and sustained convergence of the economic performances of the Member States”. The only concrete definition of convergence provided by EU law is in Article 140 para 1 TFEU, which specifies the nominal convergence criteria for candidate countries for monetary union.5 However, exceptions have already been made in practice. Italy, for example, was accepted as a member of the monetary union even though it failed the sovereign debt criterion. It was generally assumed that membership of the single currency zone would give a strong impetus to national economic reforms because the countries concerned could no longer rely on the exchange rate adjustment instrument.6 However, this expectation has not been fulfilled. Instead, a substantial number of the monetary union members have neglected urgently needed structural reforms since the introduction of the euro.

The main challenge to the smooth functioning of monetary union is the diversity of its member states.

Convergence plays a key role in the functioning of monetary union. Sustainable convergence could bring the euro area closer to being an optimal currency area, which would strengthen its stability. This could be achieved, inter alia, by promoting worker mobility and fiscal transfers.7 The convergence of per capita incomes within the monetary union also plays a major role. It is not only an important objective of economic integration, but also contributes to the overall cohesion of the euro area.8

There are no studies that show what degree of convergence would be necessary for the monetary union system and how much divergence it can withstand. In general, however, it is clear that divergent economic performance by states can undermine the stability of the economic area in two ways. First, the excessive public debt of individual economies poses an increased risk to the entire monetary union. In such cases, the ECB or the ESM can assist by alleviating the pressure of financial markets on the countries concerned. However, this requires a convergence of political interests at the euro level, as other countries must agree to bear the costs and risks of financial assistance. Second, a lack of sufficient political integration and convergence of interests can pose a risk to the stability of the currency area. Different economic performances lead to different social situations; in turn, this results in differing political objectives for European integration.9 As a consequence, the social aspects of economic divergence have increasingly come to the fore since the beginning of the euro crisis. If the political objectives of the largest economies diverge significantly and become increasingly difficult to reconcile, this could lead to the disintegration of monetary union.

The EU-19 format brings together economies of different sizes, following different economic models and at different stages of economic development. The common monetary policy and strict fiscal policy therefore complicate overall economic policy. Some countries in the currency area found it easier to cope with the consequences of the global financial crisis and the euro crisis, while others are still struggling with the economic, financial, political and social consequences. The wide range and scale of these problems are particularly evident in the case of the three largest euro area economies.

The main challenge to the smooth functioning of monetary union is member state diversity. They differ in their traditions, institutions and patterns of economic thought and action. The fact that their economic institutions, such as the labour market, are not equally efficient and flexible contributed directly to the difference in individual countries’ economic performance during the crisis. Such particularities are difficult to bring together under a common umbrella of a single currency, uniform fiscal rules and uniform monetary policy. Another important factor is that while monetary policy is regulated centrally by the ECB, economic policy is still the responsibility of member states. There are certain fiscal rules to which all states must adhere, but it is still up to national institutions to shape economic policies. Differences in the quality of state and economic institutions as well as in economic and social models are therefore constitutive for the differences in member states’ economic development.

Fundamental Differences in Economic Models

The economic models of EU countries differ in the way their product and labour markets function, in their welfare and education systems, politics, culture and even underlying ideology.10 Large economies, which are often complex, cannot always be assigned a universal classification. The three economic models are indeed classified differently. Germany and France are often referred to as belonging to the continental model, Italy to the Mediterranean model.11 Sometimes Germany and France are also categorised as “northwestern continental”.12

Within the monetary union, there are further categories. One group consists of Germany, the Netherlands, Austria, Belgium and Finland. They pursue an export-orientated growth model and are referred to as Coordinated Market Economies (CME). Such market economies prefer to coordinate their relations with other economic actors rather than rely on pure market forces. The southern European countries are Mediterranean Market Economies (MME): Spain, Portugal, Greece and Italy.13 These countries have a limited institutional capacity to coordinate wages and implement long-term growth strategies. Before joining the Monetary Union, they used periodic devaluations of their respective currencies as an instrument to increase their competitiveness.14

In this typology, the French model is situated in between CME and MME, although it has more similarities with the Southern European variant.15 Italy’s economic model also has some specific features, in particular the importance of correlations between central and regional institutions (regional capitalism).16 The economic models of the CME euro states are said to be more adaptable to changing external conditions because their growth strategies are “externally” orientated, and because they have pronounced cultures of internal cooperation. This is particularly important in the face of strong external shocks such as the global financial crisis. The type of economic model therefore plays a crucial role in a country’s economic development. With monetary integration, the Euro area member states lost a constitutive component of their options for steering economic policy. This particularly affected those economies whose competitive strategy was based on periodically devaluing their own currency within the framework of an autonomous monetary policy.

The overview of the three major economies in Table 1 (p. 10) shows their considerable differences: in territorial design, the role of the state and its relationship to the economy, but also in economic philosophy and the objectives of economic policy. The characteristics of the Italian model are difficult to capture in some categories, but in most cases it can be located between the German and French systems. Moreover, the Italian South represents a different model than the North, where industrial production and services play a much more important role.

The three countries also differ in the dominant schools of economic thought. Germany’s Ordoliberalism and France’s neo-Keynesian orientation, in particular, are often in opposition. German and French economic thinking differs, among other things, in terms of the prevailing rules, the government’s freedom to borrow, the role of monetary policy and inflation, and freedom of trade and competition.17 The most important factors in German economic thinking are personal responsibility, the disciplinary function of the financial markets, low inflation, stable finances and the independence of the central bank.18 Italian economic thinking, in turn, has been strongly influenced by both Germany and France. The Italian and French economies are similar in their demand-led, Keynes-inspired economic policies.19 Such deviations in interests and theoretical approaches make it difficult for euro area members to agree on a common direction in economic policy. This increases the divergence of economic policies, which are mainly the responsibility of member states.

The Role of the State and Social Dialogue

|

|

Germany |

France |

Italy |

|

Type of state |

federalism |

centralised unitary state |

regional unitary state |

|

Model of capitalism |

“managed capitalism” |

state capitalism |

dysfunctional state capitalism, |

|

State/economy relations |

state as guarantor of free competition, state as regulator |

state as driver, government control |

state oriented towards patronage and subsidies |

|

Dominant economic philosophy |

Ordoliberalism |

(Neo-)Keynesianism |

elements of both, dominated by (Neo‑)Keynesianism |

|

Growth model |

export-based |

based on domestic demand |

mixed |

|

Orientation of economic policy |

supply policy |

demand policy |

demand policy |

|

Priorities of economic policy |

price stability, economic growth, employment, balance |

economic growth, employment |

economic growth, employment |

|

Author’s presentation based on: Sinah Schnells, Deutschland und Frankreich im Krisenmanagement der Eurozone. Kompromisse trotz unterschiedlicher Präferenzen? (Freie Universität Berlin, 2016), 45; Markus K. Brunnermeier, Harold James and Jean-Pierre Landau, The Euro and the Battle of Ideas (Princeton, NJ: Princeton University Press, 2016); Vincent Della Sala, “The Italian Model of Capitalism: On the Road between Globalization and Europeanization?”, Journal of European Public Policy 11, no. 6 (2004): 1041–57; Carlo Trigilia and Luigi Burroni, “Italy: Rise, Decline and Restructuring of a Regionalized Capitalism”, Economy and Society 38, no. 4 (2009): 630–53. |

|||

An important feature in which the three major economies differ is the role of the state. The inequalities in this area are relevant to both the emergence of divergences and the necessary adjustment mechanisms.

In France, the state plays an especially important role. Compared to Germany and Italy, the country has a very long tradition of state centralisation, which originated with King Louis XIV (1638–1715). The Italian experience with statehood, on the other hand, is less continuous. Until the foundation of the Kingdom in 1861, Italy was really only a geographical concept. Despite the country’s regional diversity, the unitary-state model was chosen to build a compact nation state. This marked the beginning of the conflict between the central government and the regions, which manifests itself particularly strongly in southern Italy. An important feature that distinguishes Italy from Germany and France is the North-South divide in economic development.

The differences in the role of the state are evident, for example, in public expenditure as a share of GDP. A historically evolved feature of the French economic model is the high level of government spending in relation to general economic output. According to the OECD, in 2017 France’s government expenditure ratio was 56.4 percent of GDP and was the highest of all OECD countries. In Italy, this indicator is lower than for France, at 48.7 percent, but the strong intervention of the state clearly distinguishes both from the German model, where the level of government spending relative to GDP is only 43.9 percent.20 France is an active shareholder of the largest companies. This is problematic in so far as the government shares responsibility for the companies’ financial situation, as well as their protection against foreign takeover.21

As the example of the Nordic countries shows, a stronger role of the state in the economy and high tax burdens do not necessarily lead to lower economic performance. However, the Nordic economic models have specific characteristics such as efficient state institutions, a business-friendly environment, high competitiveness through innovation, low product market regulation, efficient social protection, a high degree of media freedom, low corruption, effective collective bargaining and high-quality education with broad access. In the absence of these characteristics, however, a high level of government spending has considerable negative consequences. First, the risk of misallocation of resources increases as the state intervenes in the allocation process and the latter is no longer guided by market mechanisms. Second, it multiplies the social groups that engage in “rent-seeking”, leading to the politicisation of transfers. Where the state exercises a stronger redistributive role, there are, as a rule, large numbers of domestic actors who are not interested in the status quo changing.

Political institutions should above all preserve the stability of a country and at the same time be able to initiate reforms. In Italy, political instability – reflected in frequent changes of government – is a major obstacle to coherent economic policies. Constant changes of government stand in the way of long-term strategies, such as those required to develop southern Italy. Italy has a tradition of technocratic government (governo tecnico) to compensate for the inability of political parties to form stable coalitions. Such governments usually take on the difficult task of implementing reforms that are unpopular in society.22 Although political cycles in France are much more stable than in Italy, internal party conflicts often block reforms. To surmount such situations, the Paris Government can use the legal instrument of the decree or Article 49.3 of the French Constitution. The latter allows the government to force a bill through parliament unless parliament votes a no confidence measure in the government. This procedure was used several times between 2015 and 2017 to implement labour market reforms. The German political system is currently in a state of flux because the country’s political scene is becoming increasingly fragmented; this makes it more difficult to form government coalitions.

Another important factor is the ability of the most important actors in the economy, including trade unions, to influence economic policy. France has one of the lowest rates of union membership in the OECD (7.9 percent in 2015) and yet the highest percentage of workers covered by collective agreements (98.5 percent in 2014). This means that French unions negotiate not only for their own members, but for the sector as a whole, making them much more powerful than unions in Germany. There the proportion of trade union members is significantly higher than in France – in 2015 it stood at 17,6 percent – without this being reflected in greater influence. As can be observed in negotiations, French trade unions are more politicised than German ones. In Italy, the role of trade unions is yet more complex. At 35.7 percent (2015), the proportion of members is considerably higher again than in Germany. However, the influence of Italian trade unions varies from sector to sector and region to region. In addition, Italy has a large number of small enterprises with few workers and a high level of irregular employment.

The Efficiency of Public Institutions

There is a positive correlation between the economic institutions of a state and its economic performance. The quality of institutions is sometimes presented as decisive for the success or failure of entire nations.23 More recent analyses have also shown that institutions are an important factor in explaining the economic divergence between members of the monetary union.24 There is evidence of a direct link between institutions and public debt on the one hand and economic growth on the other.25 Moreover, the research in institutional economics demonstrates that the fundamental prerequisite for better economic policy is to reform the social and political institutions that shape it.

The institutional perspective must therefore be taken into account in explaining the euro crisis. The “northern” economies of Europe, including Germany, had more institutional capacity than the “southern” ones to pursue export-orientated growth strategies. Such strategies require coordination between producers, coordinated wage bargaining and cooperation in vocational training with a focus on skills and innovation promotion.26

The efficiency of state institutions and state regulation has a direct impact on a country’s economic activity. It is a prerequisite for innovation and productivity. The World Bank’s “Doing Business” analyses show this correlation.27 They identify legal obstacles in Italy, for example, which are reflected in a low recovery rate and high insolvency costs. In addition, these hurdles have a negative impact on current efforts to restructure the country’s banking sector, which is suffering from non-performing loans. Regional data, on the other hand, show that there are significant differences in the efficiency of public institutions between the north and the south of Italy.28

Economic Structures: Differences and Connections

One of the main characteristics of the euro area is a high level of economic-structures differentiation at the national level: some are demand-led, others supply-led.29 At present, the three largest economies in the euro area show marked differences.30

An open economy has some advantages for a country’s competitiveness and convergence towards more efficient economies. It expands the markets for domestic companies and exposes them to international competition. An economy’s success in international competition depends directly on the quality of government institutions and regulatory practices, on productivity, infrastructure and human capital.31 The German economy has a higher degree of openness than the Italian or French economies. It is strongly geared to exports, which accounted for 46 percent of German GDP in 2016.32 That year, Germany generated the largest trade surplus worldwide. There are now also many competitive companies in Italy that are successfully expanding in foreign markets. However, the level of Italian exports to GDP is significantly lower (30 percent).

The economies of the three countries being examined here are closely connected. There are more interdependencies between the French and German economies than between each of the two and the Italian economy. How mutual economic relations have developed also has to do with the extent to which the three countries cooperated politically after the Second World War. France and Germany worked closely together, which led to a strong economic exchange and mutual dependencies between the two economies. For both France and Italy, the German economy carries enormous weight,33 achieving a significant surplus in bilateral trade.34 All three countries are also important sources and targets of reciprocal direct investment. Although their financial sectors are dominated by domestic institutions, they are still strongly interconnected.35 In December 2017, German banks held financial claims against France amounting to approximately €180 billion and the liabilities of Italian banks to German ones totalled €67 billion.36 This is an important link between the three economies; it is also a potential channel of risk transmission.

Convergence or Divergence in the Monetary Union?

The respective economic models and the efficiency of the national economic institutions have a direct influence on the economic performance of the three largest euro states. At the start of monetary union, the economic and political situation in Europe was quite different from what it is today. Following the implementation of Stage Three of Economic and Monetary Union in 1999, Italy and France experienced stronger GDP growth dynamics than Germany. The Federal Republic was regarded as the “sick man of the euro”, and there were fears that its economic problems might have a negative impact on the stability of the single currency.

Until 2005, economic cycles in Germany, France and Italy were relatively similar; thereafter growth slowed significantly in Italy. In the years of the global financial crisis starting in 2007 and during the euro area crisis, all three economies experienced a deep recession. That the decline in France was comparatively weaker is due to distinct features of the French economic model and the lower importance of foreign trade for the country. The Italian economy, on the other hand, was severely affected by the crisis, which was exacerbated by its subsequent budget consolidation. That Italy’s GDP has risen noticeably since 2015 is mainly due to the growth of the global economy and the ECB’s accommodative monetary policy.

The next part of this study will examine the varied economic performance of the three countries with a special focus on the functioning of economic institutions. Nominal convergence will be mainly analysed in the context of competitiveness and public finances. The aim is to clarify why the three economies have developed so differently. Real convergence will be measured on the basis of income development and the labour market situation.

Competitiveness

The Real Effective Exchange Rate (REER) is one of the most important indicators of the competitiveness of an economy. It provides information on the price trends of goods produced in that country in relation to its main trading partners.37 The loss of competitiveness vis-à-vis trading partners caused by inflation differentials is generally considered one of the main reasons for the weak economic performance of certain euro area countries. Higher inflation in one of the member states can make exports from that country more expensive than exports from the others, while imported products simultaneously become cheaper than domestic products. This mechanism is known as the appreciation of the real effective exchange rate. If, on the other hand, the development of the REER is negative, the domestic economy will become more competitive compared to that of its trading partners.

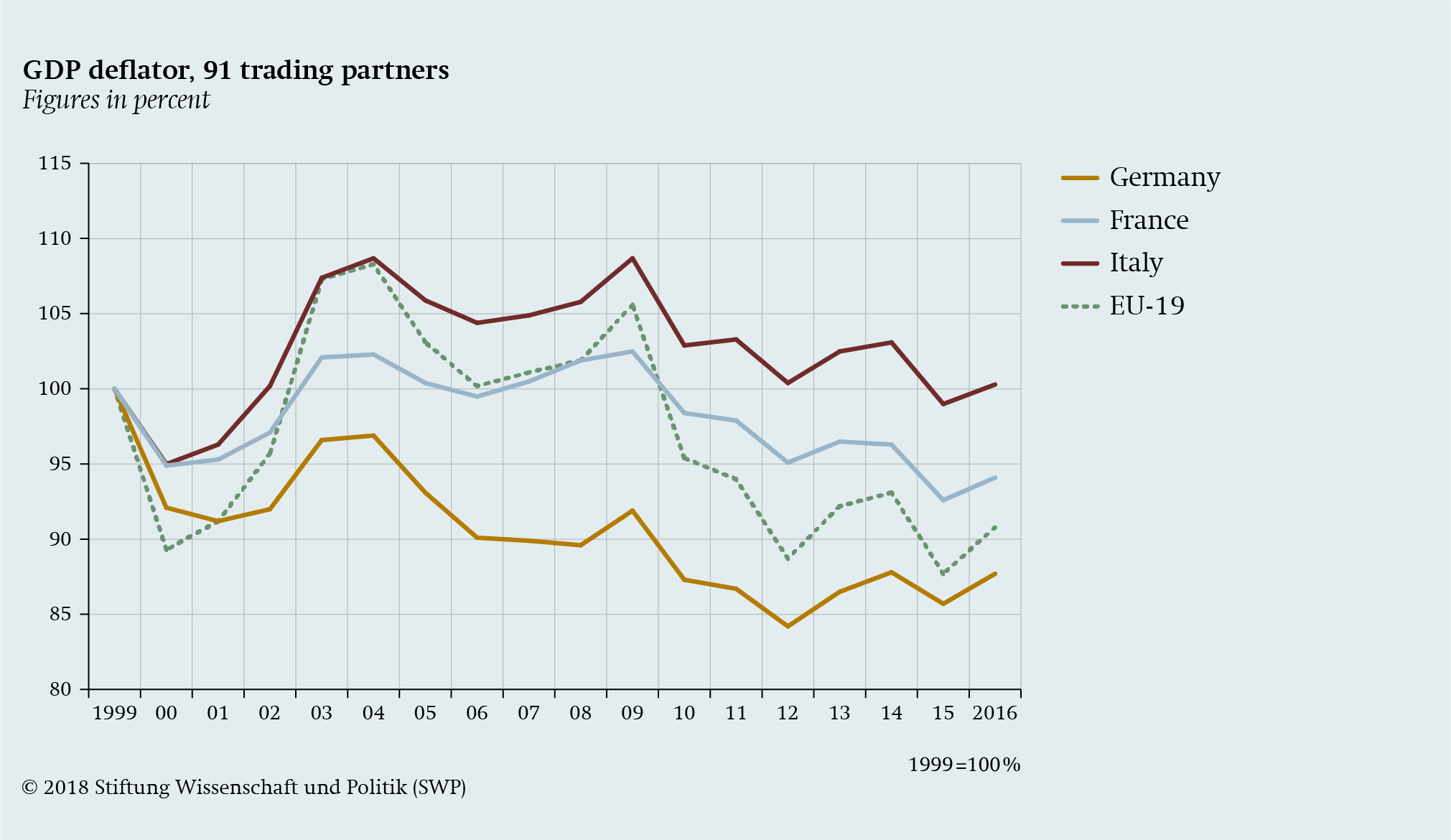

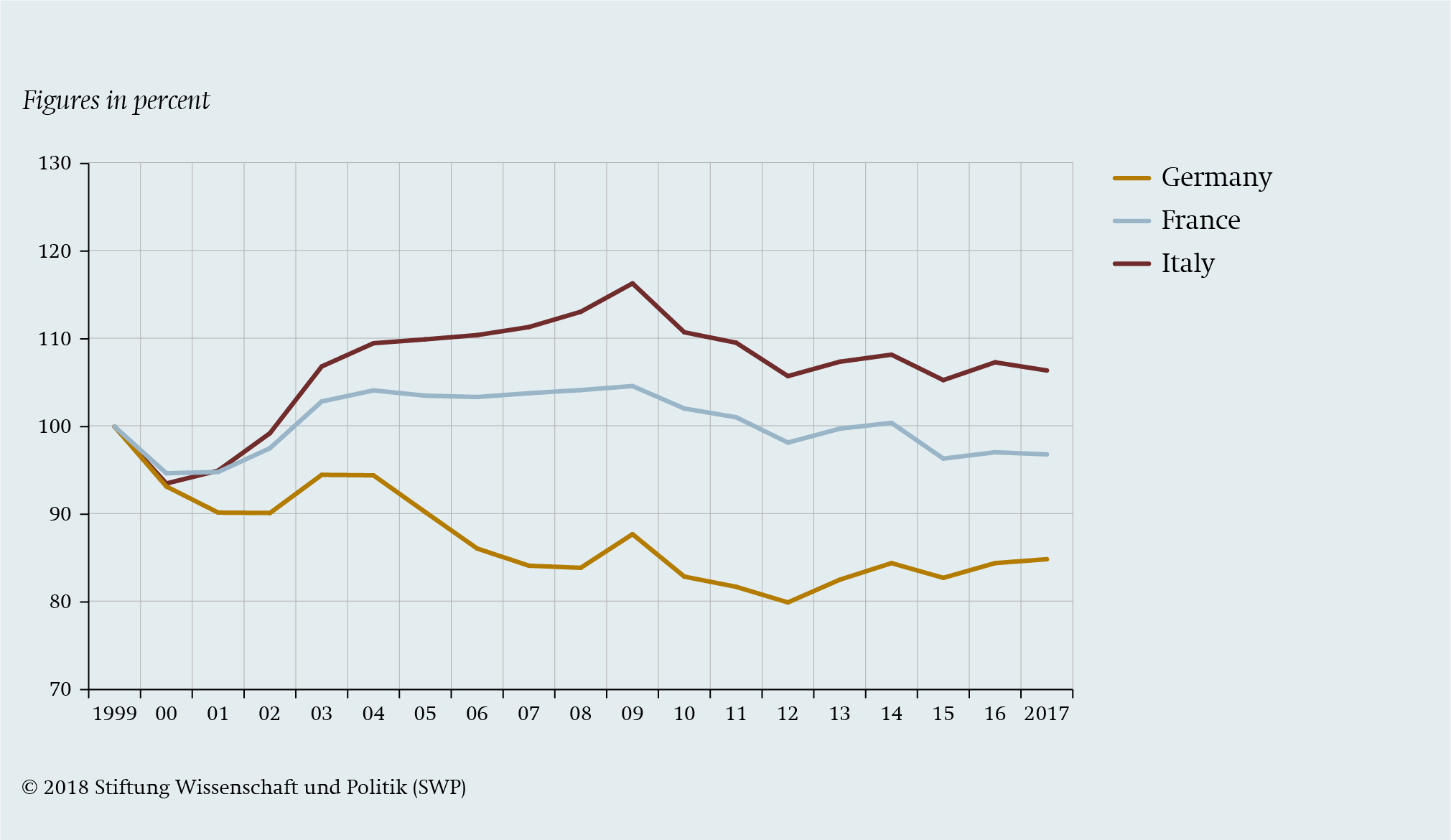

Graph 1 (p. 15) shows how the REER developed between 1999 and 2016 in the three major euro area countries and in the euro area as a whole. It is evident that Italy’s membership of the monetary union has had a negative impact on its exports because the high REER has reduced the external competitiveness of its economy. Even though the price competitiveness of France and Italy improved after 2010, Germany’s real effective exchange rate remains well below that of the other two countries. The German economy has remained much more competitive because it has been able to keep its labour costs low. Graph 2 shows the development of this factor in Germany, France and Italy from 1999 to 2017. Clearly the trend differs between the three countries. After 2001, labour costs developed very differently in France and Italy compared to Germany. The euro crisis did not bring about any significant convergence; although labour costs have now also fallen in France and Italy, the same trend has applied to Germany. The most important explanation for Germany’s differing values is the way the German labour market institutions function. Its labour market is based on flexible contracts and reciprocal agreements between trade unions and employers’ organisations. These instruments have made it possible to decentralise wage bargaining and shift it to the enterprise and industry level.38

Graph 1 Real Effective Exchange Rate (REER) of Germany, France and Italy, 1999–2016

As a “northern” economy with strong institutions, Germany thus enjoys a considerable competitive advantage, which leads to the accumulation of current account surpluses. This is mainly due to wage restraint, but also to other factors that ensure an optimal product range for imports from the BRICS countries (Brazil, Russia, India, China, and South Africa) or ensure cost efficiency by using supply chains towards economies with low labour costs. The dynamics of relative prices reflect not only changes in labour costs and other production factors, but also growth in productivity and quality improvements. Qualitative improvements were similar in the three large euro states. Low productivity, however, was a significant challenge of the Italian economy.

The current account balances of France, Germany and Italy have also increasingly diverged since the beginning of the monetary union. The current account balance reveals the specific features of the French economy. It is mainly based on domestic consumption, is strongly driven by government expenditure and its external competitiveness is low. The core of the current account is the trade balance. One of the most controversial topics in debates on imbalances in the euro area is Germany’s massive trade surplus. Although most of this is achieved with countries outside the monetary union,39 in 2017 Germany also generated significant surpluses in trade with France (€41.4 billion) and Italy (€10 billion).40 In France, it is often argued that the German surplus is at the expense of the other euro countries.41 Germany’s trade balance surplus is interpreted in different ways, but in any case results from several internal and external factors. One explanation lies in the basic determinants of import and export, such as the productivity of the German economy and the quality of its products. Another interpretation is that in the event of a surplus of national savings over national investments – as in Germany – the savings flow abroad as capital exports and promote the import of German products there.42 According to yet another interpretation, Germany’s low REER and low domestic demand are responsible for the surplus. The latter, it is argued, poses a threat to the euro area, as other countries will not be able to keep up due to the German price advantage.

Graph 2 Relative labour costs in Germany, France and Italy, 1999–2017 (1999 = 100%)

There is also a risk for Germany itself. As mentioned above, Germany exports a great deal of capital, making it an important creditor state. Moreover, an export-driven current account balance containing massive surpluses should be considered as a warning signal because it often reflects economic problems. These may be structural weaknesses requiring changes in economic and social policies, such as low domestic demand, demographic ageing, high labour taxation, insufficient investment or low wages. In general, the German trade surplus is due to both structural and economic policy factors – and it should be tackled. Possible solutions on the German side include strengthening domestic demand through wage increases and a more expansionary fiscal policy.43 However, these methods would not necessarily increase internal consumption or imports from other euro area countries, including France or Italy. Higher wages can also lead to higher savings. To achieve more convergence, structural adjustments in the other euro area countries will also have to be pursued.

Public Finances

One of the most important factors exposing the divergence between the large euro area countries is the state of public finances. There is a close link between the problems of persistent negative current account balances discussed above and excessive public sector debt. The latter leads to a negative net foreign asset position and increases a country’s dependence on foreign capital to finance its domestic economy. The budget deficit and the ratio of sovereign debt to GDP are among the most important criteria for nominal convergence when a country wants to join the euro area.

As Graph 3 shows, France, Germany and Italy recorded similar debt financing costs almost throughout the entire first decade of monetary union. This came to an end with the outbreak of the global financial crisis and the Euro area crisis. The German and French yield curves on one side and the Italian on the other side started to diverge significantly. German and French government bonds were also priced differently by the investors. The interest rates of the German government bonds served as a benchmark to assess the trends in financing costs of the other EU‑19 countries.

Graph 3 Evolution of yields on ten-year government bonds in Germany, France and Italy

Italian public finances are a special case. After the onset of the global financial crisis, the country was particularly hard hit by the increase of interest rates of its government bonds. Its present level of public debt is alarmingly high. However, the problem of growing public debt predates the crisis in the monetary union. In Italy, government debt began to rise gradually as early as the mid-1960s. This was justified by the fight against inflation and the attempt to stabilise the lira within the framework of the European Monetary System. However, the origins of Italy’s debt problem are much more complex. They can also be explained by the economic differences between the north and south of the country and by the behaviour of its national institutions. In southern Italy, large and persistent deficits arose, which were not counteracted for political reasons. Regional governments there caused massive overspending without internalising the costs of growing national debt.44 Neither the centre-right nor the centre-left governments in Rome during the 2000s were able to push through the reforms needed to reduce debt and improve the country’s competitiveness and cohesion. Since the escalation of the euro area crisis in 2010, the problem has become even more acute. In the summer of 2011, Italy was on the verge of insolvency. The reason was not only the high public debt, but also the distrust of international investors, which was fuelled by a conflict between then Prime Minister Silvio Berlusconi and Finance Minister Giulio Tremonti. The Securities Markets Programme, a bond purchasing programme of the European Central Bank for the secondary market, probably saved the country from insolvency. The ECB is currently the only institution able to stabilise the country’s debt market. In mid-2018, the announcement of additional public spending by the Conte government led to a substantial rise in interest rates on Italian government bonds, raising questions about the sustainability of the country’s public finances. In 2018 the public debt was close to 133 percent of GDP and the Italian debt market was far from stable.

Graph 4 Public debt of Germany, France and Italy, 1960–2018

France also has significant problems in stabilising its public finances, but the difficulties are somewhat different. The high level of government spending – with France topping all other OECD countries – remains at the heart of national budget problems. According to the IMF, what caused the country’s large budget deficits were the rapid growth in social, wage and municipal spending during the global financial crisis.45 France also has the highest private sector debt within the euro area (households and non-financial corporations). Private debt accounts for almost 130 percent of GDP, and is rising. Potentially, this is a significant risk transmission channel for the country’s entire economy as well as its public finances.46

In Germany, the trend in public finances is completely different from France and Italy. During the euro crisis, the country benefited from significantly lower borrowing costs. This factor has helped to balance the federal budget since 2014. The level of government gross debt fell from 81 percent of GDP in 2010 to 60.9 percent in 2018. According to some calculations, the total savings that Germany achieved between 2010 and 2015 through the low interest rates on government bonds add up to almost €100 billion.47

Another problem with public finances is that they are linked to the banking sector. There is a link between taxpayers and banks for as long as the banks are restructured and capitalised with public money. Contrary to media coverage, state aids to the banking sector in Germany during the crisis years were much greater than in France or Italy. During the period 2010–2017, government debt resulting from support to financial institutions was between 5 and 10 percent of GDP, while Italy and France had almost no such debt at all.48 Due to the increasing spreads on government bonds, the governments of the southern euro countries were unable to provide any significant assistance to the banking sector. Germany, on the other hand, was able to help its banks thanks to low spreads on government bonds, which ensured low financing costs for industry and helped finance foreign demand.49 In Italy, the sustainability of public finances is further undermined by the difficult situation within the banking sector. The third largest economy in the euro area has still a very high proportion of non-performing loans (NPLs). In the second quarter of 2018, NPLs in Italy accounted for 9.9 percent of total loans. In Germany, on the other hand, this share is only 1.5 percent, and in France 3.1 percent.50 Non-performing loans are loans whose repayment is either heavily in arrears or very unlikely. In such cases, the bank must make a value adjustment to the loan with additional capital, thereby either reducing its profit or increasing its loss. A high number of non-performing loans can therefore cause considerable difficulties for banks.

Excessive public debt is a major burden on Italy’s budget. In times of unfavourable economic conditions, there is no room for manoeuvre in fiscal policy to stimulate the economy. The cost of servicing the debt also increases the pressure on other expenditures in the budget. According to OECD figures, debt service costs in Italy amounted to 4.8 percent of nominal GDP in 2014.51 They thus exceeded the country’s public spending on education, which, according to UNESCO, amounted to only 4.1 percent of GDP in the same year.52

The fiscal policy framework of the monetary union is a central theme for Paris, Rome and Berlin. Because the three countries differ in their economic performance, they also pursue different political priorities with regard to the EU. The European Commission is calling for budget deficits to be reduced at a predetermined pace. This prompts France and Italy to focus their efforts on making financial supervision in the euro area more flexible. For example, Paris has proposed excluding investment or defence expenditure from the deficit calculation, which would loosen the EU framework.

Of the three countries, Germany has the largest fiscal room for manoeuvre, but its fiscal policy remains extremely rigid as it aims at balanced budgets. Opportunities to secure sustainable economic growth in Germany are therefore not being properly utilised. Its growth potential could be increased through investment in infrastructure, digital networks, better childcare, and increased integration of refugees and lower taxation of labour.53 On the other hand, the high indebtedness of some countries severely exacerbates the divergence problem in the euro area. Excessive public debt slows down the economy in several ways, for example by crowding out private and public investment, or triggering speculation about a country’s possible insolvency. All this leads to macroeconomic uncertainty, which is particularly strong in Italy.

Income Development

Real convergence, measured by per capita income, reflects how the population’s prosperity develops and is therefore closely linked to changes in social conditions. Analyses of the situation prior to the creation of Economic and Monetary Union show that real convergence between the current euro area countries has gradually declined since the early 1980s.54 It was expected that monetary union would strengthen convergence between members. This has not been achieved, however. In fact, there has been a strong process of divergence between the first members of the euro area since the introduction of the single currency. As the data show, the three major economies have developed differently in this respect. Graph 5 (p. 21) shows that Italy’s GDP level per capita in 2018 was on a similar level as in1999. The country’s performance is worse than that of Greece and other euro area members who received financial assistance during the crisis. In 2019, Italy is expected to reach a symbolic GDP growth rate of around 0.2 percent. This will complicate the process of returning GDP per capita to the pre-crisis levels of 2007. According to IMF forecasts, this should be achieved by 2027. Furthermore, there are also large differences in per capita income in Italy along the north-south axis.

France has had a much better growth momentum since 1999. However, it must be remembered that the French population has grown faster than other countries’, so that its GDP per capita is proportionally lower. France has not been able to translate the additional labour supply into growth. Real GDP per capita has risen less in France than in some euro area countries that have experienced economic difficulties, such as Finland and Spain.

The Labour Market Situation

The economic performance and GDP per capita of individual countries often depend heavily on the quality of their public institutions.55 This is particularly evident in Italy: the inefficiency of its public sector has a negative impact on the country’s competitiveness. One of the most important areas of divergence between the three economies is the labour market, especially its flexibility. There are major problems in the way the Italian labour market institutions function. Italy ranks 116th on the Global Competitiveness Index in terms of labour market efficiency.56 This measures the ease with which workers are hired and dismissed, and collective bargaining takes place. Germany and France ranked significantly higher: 14th and 56th, respectively. There is general agreement that countries whose labour and product markets have more rigid structures have been more affected by the crisis than those with more flexible markets. Existing divergences were thus encouraged.57

Both France and Italy face the problem of structural unemployment. The situation in both countries has deteriorated as a result of the euro crisis. From 2011 to 2014, unemployment in Italy rose from around 8 percent to over 12 percent. As of 2015, the situation gradually began to improve again, due to a change in economic conditions and some reforms of the Italian labour market (Jobs Act). However, the labour market is still a cause for concern. This is particularly true with respect to certain statistical values. For instance, the female employment rate in Italy is the third lowest of all OECD countries (ahead of Turkey and Mexico).58 It is also striking that the costs of the crisis on the labour market are disproportionately borne by the younger population.59 Youth unemployment level in Italy is at almost 33 percent, one of the highest rates in Europe. In most cases, younger workers only have temporary contracts. However, the division of the labour market into temporary and permanent jobs is also a problem for the other large euro area countries. In 2017, almost 17 percent of employees in France were employed in temporary work – significantly more than in Italy (15.4 percent) and Germany (12.8 percent). In all three countries the share is thus above the OECD average of 11.2 percent.60 Among OECD members, France has not only the lowest rate of change from temporary to permanent contracts, but also the highest rate of under- and over-qualified workers in the workforce.61 This indicates institutional problems in the labour market linked to deficits in the education system and in vocational qualifications.

Graph 5 GDP per capita in selected countries

In Italy, the north-south divide must be taken into account for the labour market as well. In 2018, unemployment in Sicily was 21.5 percent, more than three times as high as in Lombardy (6 percent).62 For Italy as a whole, in 2017 the proportion of 15–29 year olds who were Not in Education, Employment, or Training (NEET) was 25.11 percent.63 This is not only the highest rate within the monetary union, but also one of the highest among OECD economies. In Italy, youth unemployment closely correlates with the rate of early school leavers, which is particularly high in the south. The euro crisis has made young people’s lack of prospects even worse; some scholars consider it a “lost generation”.64

Graph 6 Unemployment rates in Germany, France and Italy, 2005–2017 (%)

In Germany differences persist between east and west, which are reflected in unemployment statistics, real GDP per capita and the location of the largest companies. But neither Germany nor France has such serious regional differences as Italy. In France, the most vulnerable groups on the labour market are young low-skilled workers and immigrants from outside the EU.65 The situation in Germany is quite different from that of France and Italy. In the initial phase of monetary union, Germany had to contend with even greater problems on the labour market than the other two countries. From 2004 to 2007, unemployment was higher in the largest EU economy than in Italy or France (see Graph 6). Not until 2009 did Germany’s rate fall below Italy’s (7.7 percent), to 7.6 percent.66 The labour-market and social reforms implemented by Germany between 2003 and 2005 are one of the main reasons for its rising labour force participation and falling unemployment.67 Unemployment has remained at its lowest level since reunification. In the coming years, however, Germany will face several challenges, such as integration of immigrants into the labour market.

In summary, comparing the three largest euro economies reveals a growing divergence in competitiveness, public finances and their social conditions. These differences in economic performance have various causes. Some can be attributed to monetary integration, which has eliminated the instrument of flexible exchange rates at the national level. However, the main reasons lie in the structural characteristics of the three economies. Persistent differences in inflation and labour market performance have contributed to the existing chasm in competitiveness, which is reflected in the respective current account balances. A closer look reveals complex structural problems in labour markets and wide regional disparities, particularly in Italy. In theory, internal deflation is necessary to improve the country’s competitiveness. However, deflation would hamper growth. It is difficult to imagine that such a process would be socially and politically acceptable for Italy. Despite all this, the extent of economic divergence between the three economies is so significant that a sustainable convergence path for the monetary union cannot be achieved in the foreseeable future.

The Future of the Euro Area with Limited Convergence

The need for convergence continues to play an important role in discussions at various levels on the future of monetary union. The ECB’s expansive monetary policy largely contributed to the last phase of positive economic climate. In October 2018, net purchases of government bonds were reduced to €15 billion per month and discontinued at the end of the year. If the expected slowdown in economic growth occurs, France, Germany and Italy could again drift further apart in their economic performance. The structural differences between the economic models of the three countries are unlikely to narrow significantly in the foreseeable future. Therefore, economic divergence is likely to persist for a long time and remain one of the major challenges for European economic integration.68

Two questions are particularly important in this context. First, might withdrawing from the monetary union or splitting it into two currency areas be a better alternative to retaining the current composition of the euro area? Would convergence between Europe’s largest economies be strengthened if national currencies were reintroduced? Second, in which direction should the entire economic and monetary integration process move? In the medium term, monetary union is not expected to transform into a federal or quasi-federal system. What path should be taken to better prepare a euro area with limited convergence for the next crisis, taking into account the different interests of the three largest countries?

Convergence through Disintegration or Fragmentation of the Monetary Union?

Withdrawal from Monetary Union

Since the outbreak of the euro area crisis, there have been regular discussions as to whether a return to the national currency in some states could help improve their economic situation and increase convergence.69 Of the three countries discussed here, speculation about Italy’s withdrawal from the euro is particularly frequent.70 There are several factors that could speak in favour of such a step. A national currency with a flexible exchange rate can help to mitigate external shocks and increase the price competitiveness of a state’s economy. In addition, national monetary policy can be better coordinated with national fiscal policy, allowing a country to respond to macroeconomic imbalances with a consistent policy mix.

However, there are many arguments that contradict the assumption that the reintroduction of national currencies would improve convergence between countries. Three overriding aspects speak against an optimistic interpretation of a euro withdrawal: the behaviour of the population, the likely depreciation of the new currency, and the lack of a regulated withdrawal procedure.

First, while a return to the national currency would restore national control over monetary policy, the first reports of the country in question leaving the euro should be expected to lead to a “bank run”, i.e. inhabitants would try en masse to withdraw their deposits as quickly as possible. This would paralyse the financial sector. Such a scenario is particularly likely in Italy, where there is little confidence in the banking system. To prevent a run on the banks, capital controls would have to be introduced to prevent capital from flowing abroad. This in turn would prevent the country from fully participating in the EU internal market, which would be extremely damaging to the economy and fatal to many businesses.

The depreciation of a new currency would mean bankruptcy for many private companies in Italy.

The second set of counterarguments is related to the depreciation of the new currency. Such depreciation would be initiated almost automatically if investors lacked confidence in the new currency. On the one hand, the depreciation would mean bankruptcy for a large number of private companies in the country, because the companies’ assets would be converted into the new currency, whereas liabilities to foreign companies would still have to be paid in euros. On the other hand, investors who have invested in public debt would be severely damaged by the withdrawal of the country from the euro. A special feature of Italy’s public debt is that only a relatively small proportion of public debt is held by non-residents: 33.3 percent in August 2018.71 Italy thus has the lowest share of government bonds held by non-residents among all euro countries.72 Domestic investors would be paid back their debts in the new currency, which would have a much lower value against the euro. Even more serious would be state insolvency, in which case the debts would not be repaid at all. The country would therefore be confronted with serious financial problems as a result of its withdrawal from the euro. Another argument in the context of currency devaluation is the related price increase for imported goods. This would increase inflation, and government bond yields would rise. Debt repayment in euros would therefore be a major problem for the budget of the country concerned. For example, the French central bank estimates additional debt servicing costs of €30 billion if a new French currency depreciated.73

An unresolved issue is how the depreciation of the new currency would affect exchange rates. In the case of France, the new national currency would lose its value only against a few countries, including Germany, Ireland, the Netherlands and Luxembourg, following a withdrawal from the euro. Because these countries account for only about 45 percent of France’s exports, more than half of its exports would be less competitive than before.74 Additionally, countries such as Italy could go into severe recession or even insolvency after leaving the currency area or after its disintegration. This, in turn, would have a very negative effect on exports, such as France’s, due to reduced demand. An additional factor is the political will of the government. Currency depreciation might well appear to be a more attractive measure for increasing the competitiveness of a country’s economy, rather than painful and protracted structural reforms. The latter are usually associated with enormous political costs. As long as there is no strong external pressure and the instrument of devaluation is available, the government concerned would probably avoid reform efforts. A “temporary” exit from monetary union is therefore not a viable way to restore convergence. Moreover, it is unlikely that either the country’s population or the rest of the euro area would accept the country adopting the single currency again at a later date.

Another problem in the event of withdrawal from the single currency is the country’s financial liabilities to the Eurosystem. For Italy, these total about €482.8 billion, as shown by the latest TARGET 2 data. For France, the problem would be considerably smaller, since TARGET 2 liabilities of the French central bank “only” amount to €19.8 billion. The most exposed central bank in the Eurosystem is the Bundesbank. Its TARGET 2 claims amounted to €872.7 billion at the end of February 2019.75 Should Italy decide to withdraw from monetary union, it would never be able to pay its liabilities. This is again due to the fact that a withdrawal would devalue its new currency whereas its debt would continue to be payable in euro.

A disintegration of the euro area or the withdrawal of individual states would also signal the beginning of serious legal disputes, as there is currently no orderly legal procedure for this. Legal chaos and economic uncertainty would result. The creation of a new currency for a euro member state would be a gigantic logistical operation that would require at least three years of intensive preparations. In addition, the withdrawal of a large euro economy would probably trigger a domino effect that could lead to the disintegration of the monetary union. The belief in the irreversibility of the euro area would be destroyed, and confidence in the euro currency would also suffer.

It can be concluded that withdrawals from the euro area would have a negative impact on convergence. The disintegration of the monetary area would have negative consequences for political integration in Europe. None of the countries examined would benefit from withdrawing from the monetary union either. Although the national government in question would have regained monetary control, this advantage would be outweighed by the negative economic, social and institutional consequences of a return to its own currency.

Splitting the Euro Area into Two Currency Areas

An alternative idea for strengthening the competitiveness of the southern states is to divide the euro area into two currency areas. This is based on the frequently voiced assessment that the euro area consists of “North” and “South” blocks, and argues that the EU‑19 should be split into these two sections.76 Historical experience also shows that it is possible to break up a currency area into two or more zones. One example is the division of Czechoslovakia in 1993. However, it is debatable whether such an option could work as intended for the euro. There are too many economic, political and legal obstacles that need to be surmounted in too short a time. As already mentioned, a split in the euro would destroy the most important foundation of monetary union, namely the principle of the irreversibility of the single currency. This could intensify speculation about the sustainability of sovereign debt of some euro members. Moreover, the EU Treaties would have to be amended to lay down the new rules, which in some countries would require referendums. Another problem is the aforementioned liabilities in the Eurosystem.

It has often been suggested that members of the southern euro area should leave the monetary union.77 From an economic point of view, however, an exit would be much easier for the strong economies of the North.78 This is due to their competitiveness, the extremely low probability that their currencies would depreciate, the stability of their banking systems, and their institutional strength. All these factors would make it possible to smoothly organise such a complex operation as the creation of a new currency. However, this currency would tend to appreciate in the stronger economies, which would be detrimental to their international competitiveness and thus to exports. For countries that base their economic model on exports, such as Germany, this is not an attractive option.

There is no question that Germany and Italy would find themselves in different currency systems if the split were to occur. However, it is unclear which camp France would be in. Membership in the southern euro would mean that the country would have to assume greater responsibility for Italy’s and Greece’s public debt and banking problems. However, participating in the northern euro would also be difficult for the French economy, since deficit rules could be interpreted more strictly and other members could better control labour costs. If three separate monetary areas were created, this would also have negative consequences for the integrity of the EU internal market.

Stabilising Monetary Union with Limited Convergence

A dismantling of the monetary union – whether controlled or uncontrolled – would pose major economic and political problems. Therefore the key question remains how the different national economies, with their different institutions and economic performances, can coexist under the umbrella of the single currency. Consideration should be given to how the stability of the monetary union could be improved when convergence processes are limited. Moreover, the debate on possible solutions to the euro crisis is strongly focused on the euro area rules. The search for new convergence criteria or a reform of the Stability and Growth Pact is the wrong way to go about this. Sufficient economic benchmarks have already been defined in the economic policy management system of the currency area. Examples are the “EU 2020 Strategy” and the macroeconomic imbalance procedure. However, implementation poses many problems in both cases, relating to the way some economies function within the rigid framework of monetary union. In this context, crucial questions arise regarding the capacity for reform of the largest economies, including fiscal transfers, sanctions mechanisms and financial markets, as well as further risk-sharing, power centralisation in the monetary union, and societal support for the euro project. All these issues are interconnected.

Transforming Economic Models

The analysis in the previous sections has shown that most of the economic problems in the euro area are structural in nature. Italy and France in particular need to adapt their economic models to changing global and regional competition. Italy faces the greatest challenges in this transformation. Because the country lacks the possibility of increasing its competitiveness via the exchange rate, it has only one option: permanent strict budgetary discipline and structural reforms. Both paths seem to be difficult to follow for political reasons. Italy’s structural problems are not easily solved due to institutional weaknesses and the political elite’s disinterest.79 A certain level of financial resources is also needed to implement structural reforms and reduce institutional shortcomings. But, due to strict budgetary discipline and substantial debt servicing costs, Rome lacks the money.

The literature on the diversity of capitalism concludes that existing economic models are subject to constant change. This transformation is demonstrably market-oriented – a development that can be observed in France and Italy in fields such as the labour market, social protection and product market regulation since the late 1980s.80 The question remains as to how to steer this change in the desired direction and to increase the chances of success for reforms.

The first and most important prerequisite for structural reforms and thus for encouraging convergence is macroeconomic stability and a positive macroeconomic environment. The more favourable the economic outlook, the lower the political cost of national reform. However, favourable economic conditions are independent of the political cycle. Furthermore, even when favourable, economic conditions often discourage political decision makers from making unpopular decisions. In times of economic slowdown, the fiscal space is often limited. Structural rigidities, especially in the labour and product markets, then deepen the recession and make recovery more difficult.

Experience shows that successful reform programmes are based on several preconditions that are difficult to reconcile. An extensive analysis of the main elements necessary for successful structural reform was presented by the OECD in 2009. They are a strong electoral mandate; effective communication between the political sphere and society; solid research behind the reform targets; sufficient time; strong government cohesion; effective political leadership; good conditions for the policy area to be reformed; and perseverance.81 It is very hard to achieve several of these factors simultaneously.

Economic reforms are much easier to implement in small euro area member states as opposed to large ones. This is due to the territorial and economic complexity of the respective economies. It is therefore not especially helpful to use the example of successful reforms in Ireland or Latvia for large countries. Moreover, the reforms in these two cases have had serious social consequences, which are still felt today. In contrast, the German Hartz reforms are often cited as a possible model in the debates on economic reforms in France and Italy. Both countries compiled legislative packages to liberalise their labour markets. In Italy, the Jobs Act was adopted in 2015, in France the Loi Macron (2015), Loi El Khomri (2016) and Loi Pénicaud (2017) were adopted. However, the desired results of these reforms are unlikely to materialise unless the labour market institutions are renewed, and lessons are drawn from the negative side effects of the German labour market reforms (such as a division of the labour market into two; and increase in precarious employment). Recent IMF research suggests that a special fiscal package should be implemented to mitigate the negative social impact of reforms.82 However, this is problematic in countries struggling with excessive public debt, as is the case in Italy and France.

The European Semester has turned into a kind of bureaucratic routine.

How, then, can national reforms be accelerated using the instruments available within the economic governance of the monetary area? First of all, it should be acknowledged that these resources only have a limited impact on the economic policies of the largest member states.

The “European Semester”, the most important instrument of economic policy coordination, has turned into a kind of bureaucratic routine. The European Commission presents each member state with country-specific recommendations (CSRs), which are then endorsed by the European Councils and then adopted by the EU finance ministers. However, the CSRs do not trigger much public debate about the macroeconomic situation or the state of national reforms. Since 2013, most of the country-specific recommendations related to Macroeconomic Imbalance Procedure have not been sufficiently implemented.83 To strengthen ownership, member states have set up various bodies to monitor economic reforms (National Fiscal Councils and National Productivity Boards). The decentralisation of this assessment is a positive catalyst for reform. However, it remains a challenge to limit tasks appropriately at each level, and to carry out checks and balances without unduly complicating economic governance.84 Besides, the largest EU economies should be subject to stricter surveillance, given their systemic importance for the euro area. The reality is rather different. There have been several instances where the Commission has put more pressure on smaller member states than on the larger ones. The experience of the European Semester also shows that the institutions of large member states are inward-looking and have little interest in accepting external advice concerning structural reforms.85

Reform capability of the largest euro countries remains uncertain – especially in Italy.

However, it is questionable whether transfers of funds to implement reforms would be a sufficient incentive for the largest euro states. Germany, France and Italy are the largest net contributors to the EU budget. Cash transfers would only adjust their net position; they would not be significant for the macroeconomic situation. Moreover, Italy’s institutional weakness makes it difficult for it to draw on EU funds. At end of 2016 the country had the largest proportion of unabsorbed EU funds from the 2007–2013 multiannual financial framework.86 If a member state is unable to pursue a proper economic policy, this usually has to do with a lack of ownership – and this cannot be “bought” with EU funds or imposed from Brussels.

Sanctions are another economic policy instrument. This instrument was strengthened during the euro area crisis for use against individual member states in the event of inadmissible national policies. However, it is difficult to envisage the largest euro area countries being subject to financial sanctions. Such punitive measures could also have counterproductive effects and strengthen Euro-sceptic movements. Both the European Commission and the ministers in the EU Economic and Financial Affairs Council (ECOFIN) are aware of the negative political consequences of sanctions against the largest over indebted countries.

Another way to create incentives for reform is through pressure from the financial markets. During the crisis, interest rates on government bonds from France, Italy and other countries rose. This was an important warning signal from the financial markets; it showed that investors were increasingly distrustful of the economic prospects of these countries. However, this kind of pressure should not be overestimated. The negative reactions of rating agencies and investors came too late to avert the crisis. In addition, at some stages of the crisis, the agencies over-reacted, thus contributing – along with some chaotic investor behaviour – to the escalation of the situation. To date, during the euro crisis, the financial markets have been characterised by irrational and short-term thinking. Their actions service the need for quick profits. Furthermore, the ECB’s expansionary monetary policy helped to lower government bond yields, which limited the “corrective” role of the financial markets. However, the pressure on Italian government bonds in 2018 and 2019 played an important role in limiting the deficit plans of the Conte Government.

Whether the largest euro countries can indeed reform therefore remains unclear. There are pessimistic predictions, especially for Italy. Institutional blockades, interest groups orientated towards the status quo and the fiscal policy of Giuseppe Conte’s government, in office since June 2018 (tax cuts and higher government spending) give little cause for optimism. The two coalition partners, the Lega and the Five-Star Movement, have announced some reforms to the justice system and the fight against corruption. In the first months of its term, however, the government focused on fulfilling populist election promises, including special benefits for the poorest sections of the population and the cancellation of earlier pension reforms. The projections of general government deficit in April 2019 raised the public deficit to 2.4 percent of GDP, significantly higher than agreed with the European Commission in December 2018 (2.04 percent). The ensuing conflict between Rome and Brussels revealed the ineffectiveness of the EU and euro area institutions and their dependence on the disciplining effects of financial markets.87 If the Conte government continues to relax fiscal policy, Italy’s financial stability will deteriorate and the country will experience further political shocks.

France’s economy continues to face significant challenges, and Macron’s reforms should be assessed cautiously.

The case of France is different. President Emmanuel Macron has been more successful with reforms than his predecessors, benefiting from favourable economic conditions. But two years after his election, there was growing resistance from various social groups, while support for the president is declining. Union protests against planned labour market reforms contributed to the sluggish growth of the French economy in mid-2018. In the autumn of that year, there were violent protests by the “yellow vests”, including blockades of motorways and petrol stations. These events will also have a negative impact on economic activity. France’s economy continues to face significant challenges, and Macron’s reforms should be assessed cautiously. Despite their clear objective of curbing expenditure, and favourable economic conditions, France’s public debt rose to almost 100 percent of GDP at the end of 2018.88 Even further-reaching reforms of public finances are therefore not to be expected. In the coming years, Germany will also be confronted with the need to review the sustainability of its economic model. An attempt to partially revise the Hartz reforms could worsen the country’s competitiveness. This would probably lead to a convergence of economic performance vis-à-vis France and Italy, but could at the same time call into question euro area sustainability.

According to current forecasts, economic growth will develop differently in the three countries, and will be heavily influenced by their demographic situations. The current trends show strong divergences in demographic outlook between the countries. In Germany the long term scenario is not very optimistic. According to the latest assessment by the Global Aging Report, between 2018 and 2070 Germany will have to face one of the highest increases of pension contributions of all EU countries (measured in terms of GDP).89 In France, the long-term demographic situation is expected to be significantly better than in Germany and Italy, according to projections of its working-age population between 2018 and 2070.90

How Much Centralisation of Power Should There Be in Monetary Union?

For some time now, there has been discussion as to whether economic policy in the currency area should be further centralised to promote convergence between member states. This issue particularly concerns the largest euro area countries. They tend to prefer intergovernmental contacts, whereas EU institutions tend to use them mainly when they see an opportunity for self-advancement. A key area of conflict has long been the implementation of the Stability and Growth Pact. The largest member states of the EU, France and Germany, diluted the rules of the Pact in 2005. Often, it is the larger euro area countries facing problems complying with budgetary rules that openly criticise the European Commission. This especially applies to France, where high-ranking politicians like to protest loudly against Brussels’ reprimands.91 Similar dissent can frequently be heard from politicians in Rome.92